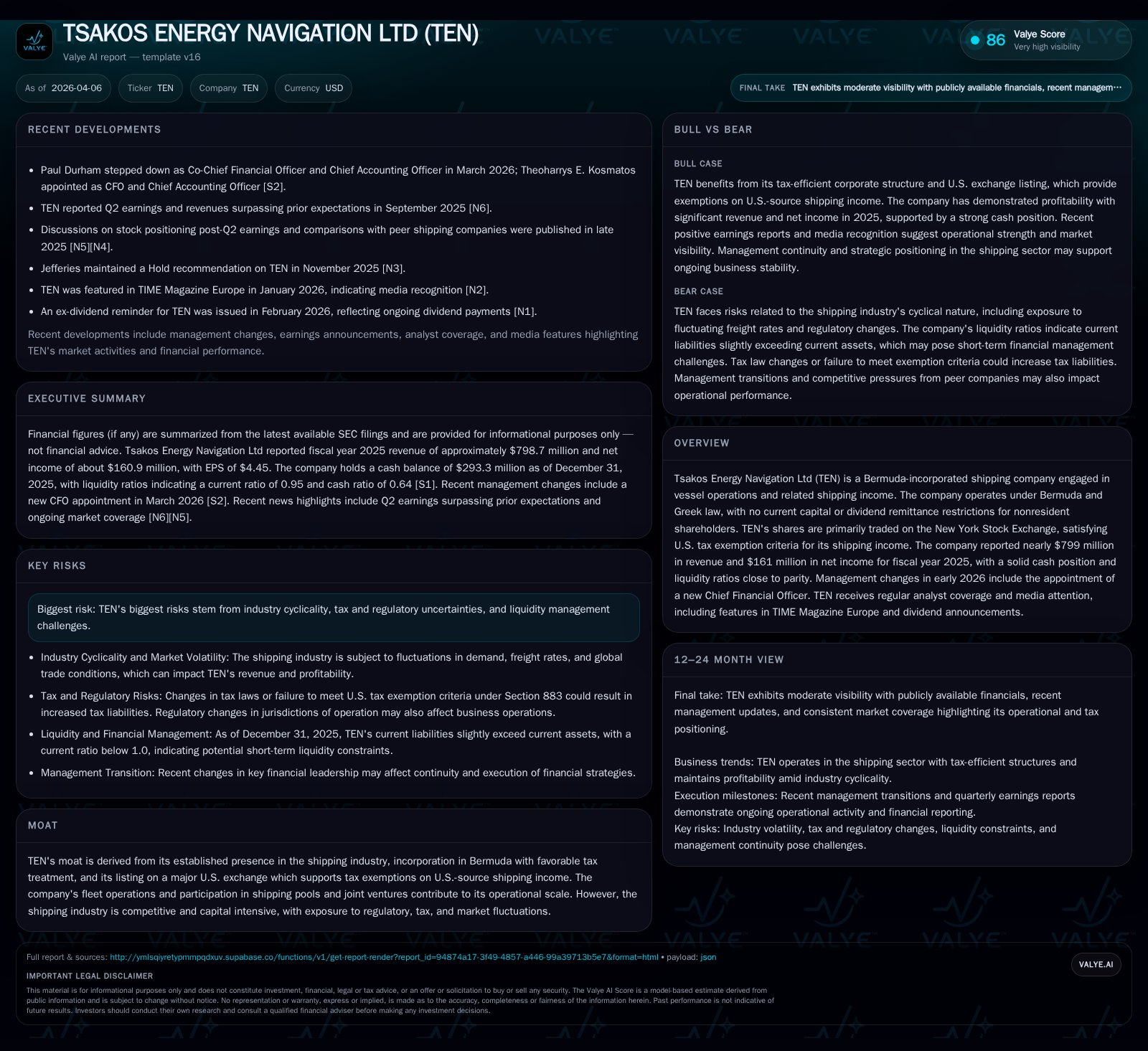

Tsakos Energy Navigation's Financial Currents and Strategic Horizons

An analysis of how TEN’s operational scale, capital allocation, and leadership changes interact amid cyclical market dynamics to influence its financial trajectory.

Tsakos Energy Navigation Ltd (TEN), a Bermuda-incorporated shipping company, reported a slight revenue decline in FY2025 but sustained strong operating cash flow amid softer freight markets and reduced dry-docking expenses. The company faces near-term liquidity pressures from maturing short-term debt and significant capital expenditure commitments. A recent CFO leadership change may influence future financial strategy. TEN's dividend continuity and tax-efficient structure support its competitive position, while tanker market cyclicality and regulatory developments remain key risks.

Historical Financial Performance and Fleet Utilization Trends

Tsakos Energy Navigation Ltd (TEN) reported fiscal year 2025 revenue of $798.7 million, representing a slight 0.7% decrease from $804.1 million in FY2024 [F1]. Operating income declined by 9.4% to $252.3 million, while net income fell 8.7% to $160.9 million [F1]. These results reflect a softening in tanker freight rates compared to prior elevated market conditions described in management commentary [S1].

Operating cash flow decreased modestly by 3.3% to $297.6 million, supported by cost efficiencies including reduced dry-docking expenses—ten vessels were dry-docked in 2025 versus fifteen in the prior year [S1][F1]. This contributed to approximately $10 million lower repair yard payments [S1]. The fleet's charter mix shifted with an increase in time-chartered vessels from forty-nine to fifty-three impacting revenue stability.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 799 | 161 | 298 | 252 | -0.7% | -8.7% |

| 2024 | 804 | 176 | 308 | 279 | -9.6% | -41.3% |

| 2023 | 890 | 300 | 395 | 391 | +3.4% | +47.0% |

| 2022 | 860 | 204 | 289 | 256 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 60 | 8.8 |

| 2024 | 72 | 10.2 |

| 2023 | 62 | 18.5 |

| 2022 | 44 | 13.9 |

Source: SEC companyfacts cache [F1].

All figures rounded; percentages based on SEC XBRL data [F1].

Revenue and Profit Drivers

The decline in operating income is linked to softer tanker market rates as the balance shifted toward more time-chartered vessels offering stable but potentially lower daily hire rates compared to spot market earnings [S1].

Additionally, accrued liabilities related to European Union Allowances (EUAs) nearly doubled from $12.9 million to $28.5 million, increasing voyage expense burdens while receivables associated with recoverable allowances also rose [S1].

Voyage expenses fell by about $39 million (7.6%), primarily due to lower bunker fuel prices and operational adjustments reducing spot market exposure [S1]. This lowered expense volatility but constrained upside earnings during favorable market spikes.

Liquidity and Working Capital Position

TEN’s current liabilities increased from $408.5 million in FY2024 to $458.0 million in FY2025 mainly due to reclassification of maturing debt into short-term obligations totaling approximately $114.6 million [S1][F1]. Concurrently, current assets decreased modestly by $17.2 million driven by a reduction in cash balances—from $343 million to $293 million—and declines in receivables and inventories partially offset by investments linked to EUAs [S1][F1].

This resulted in a current ratio of approximately 0.95, indicating tighter working capital conditions that may necessitate refinancing or asset sales should market conditions worsen [S1]. Management highlighted readiness to access capital markets or asset disposals if liquidity pressures intensify.

Capital Expenditure Commitments

Annual capital expenditures remain substantial—exceeding $530 million—with commitments focused on newbuild deliveries, vessel acquisitions, scheduled dry-dockings, and technical upgrades required for regulatory compliance [S1]. These significant outlays limit free cash flow despite strong operating cash inflows.

Leadership Change at CFO Level

In March 2026, TEN appointed Theoharrys E. Kosmatos as sole Chief Financial Officer following the departure of co-CFO Paul Durham who moved into an advisory role [S2]. Kosmatos had served as co-CFO since mid-2024.

While no specific guidance was provided on strategic changes, such transitions often precede reassessments of capital allocation priorities and liquidity management approaches.

Outlook Considerations

TEN does not provide formal forward-looking guidance but ongoing factors influencing performance include:

- Tanker demand volatility affecting charter rates,

- Evolving IMO and EU environmental regulations impacting operating costs,

- Fleet renewal timing balancing capacity growth against aging tonnage economics,

- Bermuda’s Corporate Income Tax Act effective January 2025 currently expected to have minimal material impact due to dividend exemptions [S1].

Dividend Policy and Shareholder Returns

TEN has steadily increased dividend payments from approximately $43.7 million in FY2022 to around $60.1 million in FY2025 [F1], maintaining a payout ratio near one-third of net income.

No share repurchases have been conducted since at least FY2018, reflecting a conservative approach prioritizing reinvestment and balance sheet strength over buybacks given industry cyclicality and capital demands [F1].

Operational Moat: Tax Efficiency and Contract Mix

Bermuda incorporation affords TEN exemptions from corporate income taxes and withholding on dividends internationally except for Bermuda-resident shareholders [S1], enhancing after-tax cash flow efficiency particularly on U.S.-source shipping income.

Operational stability derives from a diversified mix of time-charter contracts providing predictable revenues alongside spot market exposure capturing upside potential [S1]. Participation in pools and joint ventures further mitigates volatility through shared operational risk.

Risks: Market Cyclicality and Regulatory Developments

Key risks include tanker freight rate volatility driven by global economic shifts affecting crude oil transportation demand [S1], rising EU emissions allowance costs impacting voyage expenses unpredictably, and the implications of Bermuda’s Corporate Income Tax Act for multinational groups exceeding EUR750 million revenue thresholds—though currently assessed as limited impact for TEN due to dividend exclusions [S1]. Liquidity management remains critical given maturing debt obligations.

This report is based on publicly available filings as of April 6th, 2026 without investment advice or recommendations. Readers should conduct independent analysis before forming conclusions regarding Tsakos Energy Navigation Ltd's prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments