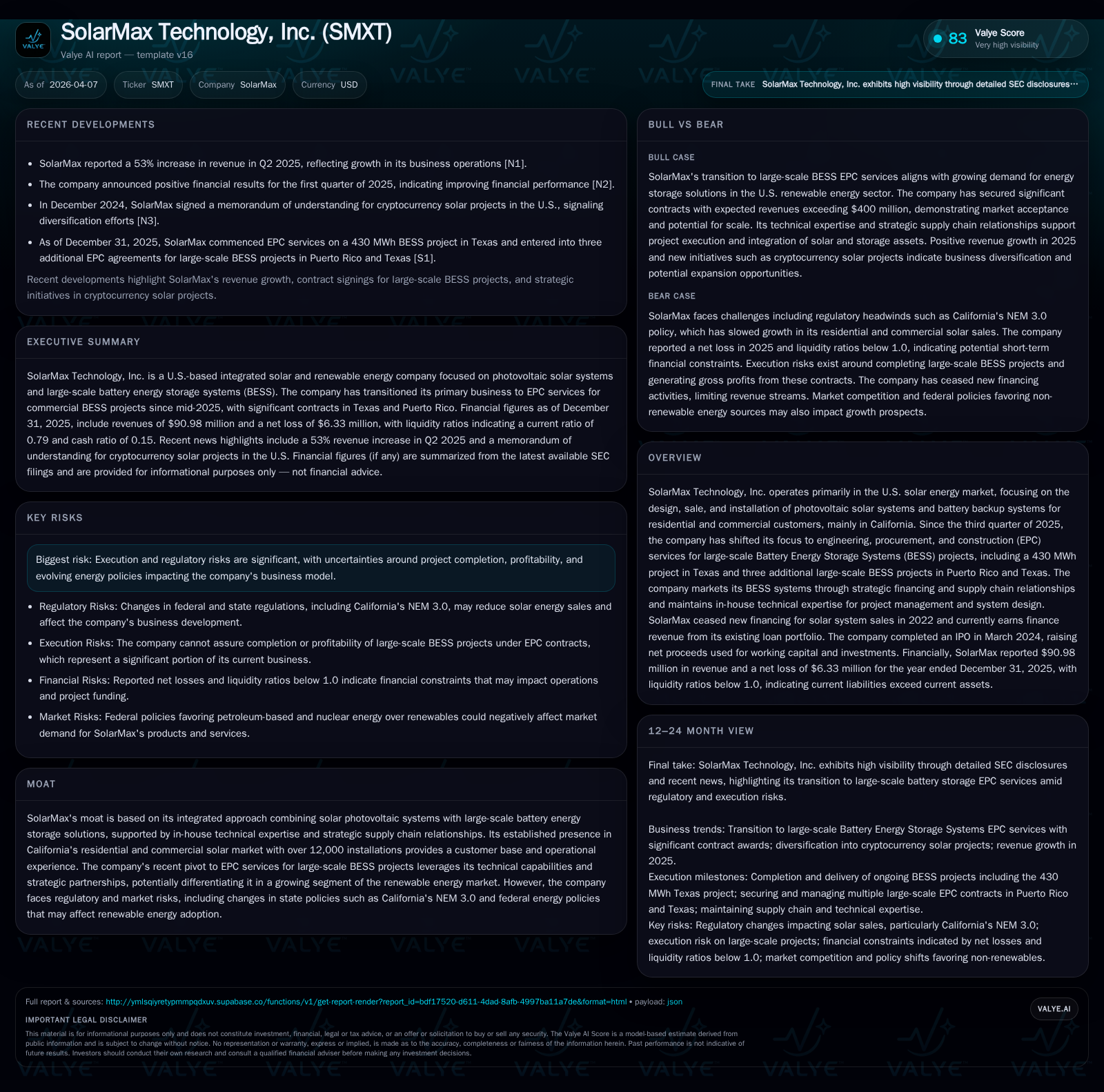

SolarMax Technology’s Transition from Residential Solar Sales to Large-Scale BESS EPC

SolarMax Technology has shifted its core operations from residential solar system sales to engineering, procurement, and construction (EPC) services for large-scale Battery Energy Storage Systems (BESS), reflecting both a strategic repositioning and response to mounting financial and regulatory pressures.

After years operating primarily in the U.S. residential and commercial solar market with integrated photovoltaic systems and financing, SolarMax pivoted sharply in late 2025 to pursue EPC contracts in the sizable battery energy storage segment. This transition drove an almost threefold revenue increase in 2025 but failed to stem net losses or improve liquidity meaningfully, as fixed-price contract risks, supply chain inflation, and regulatory headwinds persist. Capital structure challenges including defaults on convertible notes and a working capital deficit complicate the path forward. The company’s ability to profitably complete its initial large-scale BESS projects will be critical to validate its new business model amid evolving trade policies and diminishing residential solar incentives.

From Residential Installation to Industrial-Scale Battery EPC: The Growth Evolution

Prior to the third quarter of 2025, SolarMax Technology’s business model centered on the sale and installation of photovoltaic solar systems complemented by battery backup solutions targeted at residential and commercial customers primarily in California. Historically, the company also financed these installations internally but ceased offering new loans after 2022 due to capital limitations. This legacy approach capitalized on California’s vibrant solar market supported by state-level incentives.

However, evolving state regulations such as California’s NEM 3.0 policy introduced in 2024 undermined demand for residential solar systems by reducing net metering benefits, slowing growth rates significantly.[S1] In response, SolarMax pivoted strategically starting in Q3 2025 towards engineering, procurement, and construction (EPC) services focused on large-scale Battery Energy Storage Systems (BESS), shifting from smaller-scale system sales to complex industrial projects.[S1] This shift leverages SolarMax’s in-house technical expertise, project management skills, and strategic supply chain partnerships acquired through prior operations.

By year-end 2025, the company had commenced construction on a major 430 MWh BESS project in Texas under a fixed-price contract valued at approximately $60 million recognized during H2 alone.[S1][F1] Additionally, SolarMax contracted three further large-scale BESS projects—two in Puerto Rico and one more in Corpus Christi, Texas—to expand this emerging segment.[S1] While these victories underscore confidence in their technical capabilities, none of these latter projects had commenced physical construction by the reporting date.

2025 Financial Turnaround: Revenue Leap Amid Persistent Operating Losses

The strategic pivot yielded a pronounced increase in top-line performance. Annual revenue surged to approximately $91 million for FY2025—a near threefold jump of +295.8% year-over-year—primarily driven by new BESS EPC revenues comprising over two-thirds of total sales.[F1][S1] This contrasts starkly with earlier years dominated by residential/commercial system sales that slowed as financing activities ceased.

Despite sharp revenue gains, profitability remains elusive. Operating losses decreased substantially from -$33 million in FY2024 to -$6.3 million in FY2025 (-81% improvement).[F1] Net losses followed a parallel trajectory ending near -$6.3 million.[F1]

Operating cash flow improved dramatically as well: flipping from negative $9.1 million in FY2024 to positive $0.5 million in FY2025—a jump exceeding +105% YoY—signaling initial operational cash generation aligned with project execution.[F1]

Capital expenditures scaled back entirely following minor investments previously reported.[F1] Although margin pressure persists due to fixed-price contract risks coupled with input cost inflation (discussed below), the narrowing loss profile suggests early easing of financial strain linked with high fixed costs under the prior business model.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 91 | -6 | 0 | -6 | +295.8% | +81.9% |

| 2024 | 23 | -35 | -9 | -33 | -57.5% | -8141.3% |

| 2023 | 54 | 0 | 4 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 51.8 | |

| 2024 | -9 | 231.9 |

| 2023 | 4 | -2.7 |

Source: SEC companyfacts cache [F1].

Table: SolarMax Historical Financial Summary (FY2023-FY2025)

The Emerging Battery Energy Storage Systems (BESS) Opportunity and Execution Risks

The large-scale BESS sector represents an attractive growth avenue aligning with increasing grid decarbonization efforts across the U.S., especially given the accelerated deployment of intermittent renewables like solar and wind necessitating robust energy storage solutions.[S1]

SolarMax's EPC engagements are under fixed-price contracts—including the flagship Longfellow project—which expose it acutely to cost overruns stemming from volatile input prices such as polysilicon wafers critical for solar modules integrated into these systems.[S1] Polysilicon prices have rebounded recently after earlier declines globally owing to supply-demand imbalances compounded by inflationary pressures.[S1]

Compounding this are tariffs imposed or threatened on Chinese imports affecting raw materials/components costs adversely despite mitigation efforts via alternate sourcing strategies.[S1] The company discloses that while tariffs did not materially impact costs in FY2025, ongoing trade policy uncertainties cloud future margin sustainability.[S1]

Further concerns include lack of completed projects thus far leaving no operating track record for delivering large-capacity battery storage within budget or schedule constraints; delays or inefficiencies may impair profitability severely given fixed pricing structures.[S1]

Maintaining strong supplier relationships alongside deep embedded technical knowledge is therefore key competitive leverage enabling project design optimization and risk management but remains unproven at scale beyond the current flagship contract.[S1]

Navigating Regulatory and Supply Chain Pressures

The external environment poses mixed challenges:

- California's NEM 3.0 scheme reduced net metering payments effective since early 2024 curtailing residential solar demand drastically relative to prior generous compensation models.

- The federal Residential Clean Energy Credit fully expired December 31, 2025 instead of gradual phaseout planned under Inflation Reduction Act provisions altering homeowner incentive calculus markedly post-2025.[S1]

- Ongoing inflationary trends elevate labor/material costs further compounding project economics.

- Trade tariffs targeting Chinese manufactured inputs impose price uncertainty despite some mitigation steps.

These regulatory shifts materially diminish traditional revenue drivers tied to residential installations while amplifying cost pressure across all product lines including those embedded within battery storage systems reliant on silicon-based components.[S1]

Capital Structure Woes: Debt Defaults, Working Capital Deficits, and Financing Needs

As December 31, 2025 closed,[F1][S1] SolarMax carried a concerning working capital deficit approximating $20.4 million against current assets of roughly $75 million offset by current liabilities near $95 million yielding a current ratio below unity (0.79). Such imbalance constrains liquidity flexibility critically amid ongoing expansion efforts.

Convertible notes obligations totaling approximately $14.3 million were in default status impacting creditor relationships along with related party debts amounting close to $8 million combined ($5.5M secured party plus $2.5M CEO loan).[S1][S5] These burdens restrict access to affordable capital markets potentially forcing dilutive equity issuance further compressing shareholder value.[S1][S5]

The stock trading below Nasdaq’s required minimum bid price ($1/share) risks delisting events which would erode investor confidence further complicating fundraising prospects absent operational turnaround producing positive EBITDA soon.

Additionally, an outstanding receivable from SPIC (~$1M), associated with historic China projects prior to discontinuation post-2021 operations there,[S1] remains uncertain regarding collectability timing although management anticipates eventual recovery.

Dividend Policy, Buybacks, and Shareholder Returns Under Strain

SolarMax has not declared dividends nor engaged in share repurchase programs in recent periods consistent with conservation priorities amid persistent net losses,[S4] reflecting cash deployment focus towards sustaining core operations rather than direct shareholder returns.

Despite negative equity positions nearing -$12 million as of FY2025 end,[F1] a rough computed return on equity stands near +52%, propelled solely by improving net income loss contraction from prior years rather than positive earnings achievement directly—a customary anomaly during distressed turnarounds.[F1]

Absent sustained profitability restoring net income into positive territory will remain prerequisite before meaningful capital returns can be contemplated without jeopardizing corporate finances further.

Foresight: What to Watch in SolarMax’s Path Toward Profitability

Key milestones include:

- Successful on-budget completion and commissioning of the inaugural Longfellow Texas BESS facility,

- Initiation of construction activities on the three signed late-2025 EPC contracts,

- Demonstrable gross profit generation on these projects validating fixed-price contractual model viability amidst volatile inputs,

- Resolution or restructuring of convertible note defaults and working capital deficits restoring balance sheet stability,

- Management’s progress halting operating loss run rate declines toward break-even levels.

While formal guidance remains absent,[S3] market observers should monitor quarterly disclosures rigorously for progress updates given that establishing a credible delivery track record will be pivotal for contract pipeline expansion beyond initial success.

Conclusions: Assessing Risks versus Potential in SolarMax’s Strategic Reorientation

SolarMax’s transformation reflects an adaptive response seeking opportunity within rapidly evolving U.S renewable energy markets transitioning away from residential-centric solar sales toward utility-scale battery storage integration where growth prospects remain robust.

Its moat lies principally in combining legacy solar expertise with emerging battery storage engineering capabilities enabling entry into higher complexity EPC projects supported by strategic supplier alliances delivering competitive advantages.

Nevertheless, material execution risks remain around managing fixed-price contract exposures amidst pricing volatility triggered by tariffs & polysilicon price swings coupled with historically unproven delivery scale creating earnings unpredictability ahead.

Financial structural fragilities related to working capital shortfalls paired with convertible note defaults underscore immediate liquidity challenges curbing operational runway extensions absent successful project realizations or supplemental recapitalizations likely dilutive for existing shareholders.

Overall investor confidence will hinge on visible progress evidencing first profitable large-scale BESS completions aligned with prudent financial restructuring efforts navigating regulatory headwinds from diminished traditional residential incentives imposing fundamental business model recalibrations going forward.

Disclaimer: This analysis is based solely on publicly available company filings as of April 7, 2026 , SEC XBRL data [F1], and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments