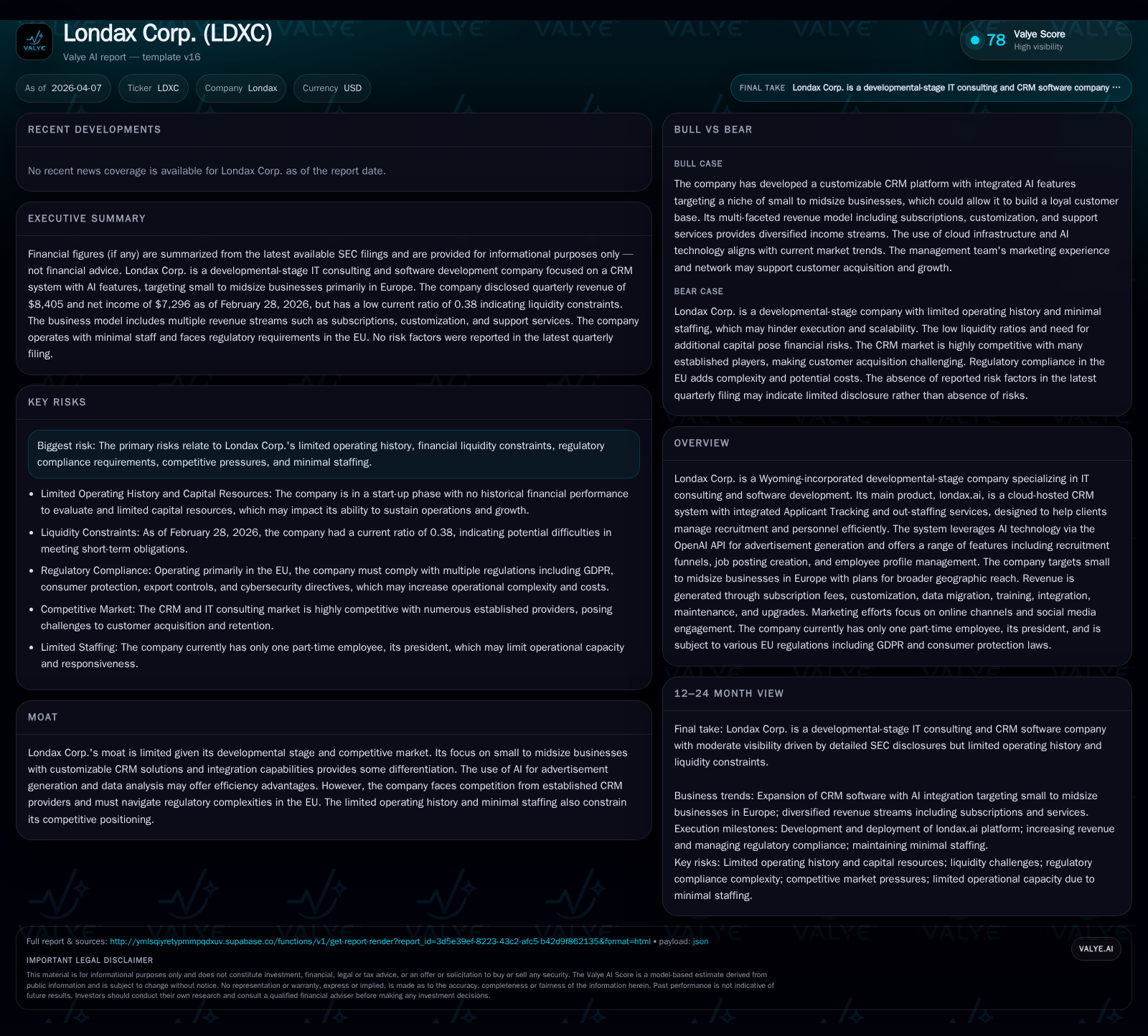

Londax Corp's Early Revenue Growth and Technological Positioning in AI-Driven CRM

Londax Corp demonstrates significant revenue improvement alongside ongoing developmental challenges as it builds an AI-enhanced CRM platform tailored for European SMBs.

Londax Corp, a fledgling IT consulting and software developer, posted a 162.5% revenue increase from FY2024 to FY2025 driven by customer expansion and higher service delivery volumes. Its flagship product, londax.ai, integrates AI-powered recruitment tools targeting small and midsize enterprises in Europe. Despite improved operating losses and stronger cash flow from operations, the company’s minimal staffing and constrained liquidity pose risks to scalability. Regulatory compliance in the EU and competition from established CRM vendors compound challenges as Londax transitions from development toward market penetration.

Trajectory of Early Revenue Growth and Underlying Drivers

Londax Corp.'s financial results for the fiscal years ended May 31, 2025 and 2024 show substantial growth in revenue alongside continued net losses typical of a startup in its early stages [F1][S1]. Revenue increased by approximately 162.5%, reaching $66,410 in FY2025 compared with $25,297 in FY2024. This rise was primarily due to a larger customer base and higher volume of services delivered.

Cost of sales appeared for the first time in FY2025 at $12,000 compared to none in the prior year, indicating initial monetization expenses associated with service delivery [S1][S4]. Operating expenses nearly doubled to $55,608 driven by increases in general and administrative expenses related to intangible asset development and higher amortization reflecting capitalization of software development costs [S1][S4]. Professional fees declined moderately but remained significant.

Despite these cost pressures, operating loss improved from -$1,882 to -$1,198 (a 36.3% reduction), signaling progress toward operating leverage as revenue scales [F1]. Net losses followed this trend accordingly.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 66410 | -1198 | 94461 | -1198 | +162.5% | +36.3% |

| 2024 | 25297 | -1882 | -53782 | -1882 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -3.2 |

| 2024 | -4.8 |

Source: SEC companyfacts cache [F1].

AI-Powered Product Suite and Market Targeting Strategy

Londax.ai is a cloud-hosted web application on AWS comprising frontend and backend components designed for recruitment management [S7][S8]. Its core functionalities include:

- Customer Relationship Management (CRM)

- Applicant Tracking System (ATS)

- Out-staffing services enabling flexible workforce engagement

- Recruitment funnel tracking KPIs across hiring stages

- Job posting creation via manual input or AI-generated advertisements using the OpenAI API

- Employee profile management features

This platform targets small to midsize enterprises primarily in Europe with plans for broader global reach [S7][S10]. The company’s revenue model combines subscription fees with project-based charges for customization, data migration partnerships, training/consulting services, integration support, maintenance contracts, and upgrades [S7][S10].

Marketing efforts leverage digital channels such as SEO optimization and social media platforms (Facebook, Twitter, Instagram) combined with online advertising via Google AdWords and Facebook tools alongside participation in industry events to reach prospective clients effectively [S8].

EU Regulatory Environment and Competitive Dynamics

Operating within the EU necessitates compliance with multiple regulatory frameworks impacting Londax’s SaaS business model [S9]:

- GDPR mandates rigorous data protection standards around personal data processing.

- Consumer Protection Laws regulate online service contracts including cancellation rights.

- Copyright laws protect proprietary software while preventing infringement.

- Export Controls may apply if encryption technologies are involved.

- E-Commerce Directive governs electronic contracts.

- Competition laws affect pricing strategies.

- VAT rules vary across member states complicating invoicing.

- Network Information Security Directive requires cybersecurity measures.

These regulations add complexity and cost burdens that Londax must manage amid competition from established CRM providers benefiting from scale economies [S9].

Liquidity, Capital Structure, and Funding Imperatives

As of February 28, 2026 Londax reported current assets of approximately $24,631 against current liabilities of about $63,995 yielding a current ratio near 0.38—a liquidity constraint highlighting reliance on creditor financing [F1]. Accounts payable rose sharply to $51,372 by May 31, 2025 compared with $14,512 the previous year [S1][S15], emphasizing working capital dependency.

Related-party liabilities owed to the president totaled about $4,281 at fiscal year-end indicating insider financing arrangements supporting operations [S3]. Capital structure changes included voluntary cancellation of restricted shares reducing outstanding shares significantly mid-2025 which impacted equity distribution but did not affect cash resources directly [S16].

Future financing availability remains uncertain given limited operating history; equity raises could dilute shareholders further as external institutional investment has not been prominently disclosed [S16][S22].

Profitability Metrics and Cash Flow Analysis

While net income remained negative at -$1.2K in FY2025 (an improvement over FY2024), operating cash flow turned positive at approximately $94.5K compared with a negative cash flow of -$53.8K the prior year [F1][S1]. This improvement was driven largely by non-cash amortization expenses ($11.3K) and working capital management including increased accounts payable balances providing temporary liquidity relief.

Return on equity is estimated around -3.2% reflecting ongoing investment losses relative to equity capital invested [F1]. Capital expenditures focused on intangible asset development consistent with R&D priorities rather than physical asset acquisition [S4]. No dividends or share repurchases were reported aligning with typical startup capital conservation strategies.

Operational Risks Amid Limited History and Minimal Staffing

Londax operates with minimal staffing—only its president dedicates part-time hours—raising concerns about capacity to scale operations or meet governance demands particularly under complex EU regulatory regimes [S6][S9]. The company’s short operating history limits visibility into sustainable business execution or competitive positioning.

Competition is intense with global CRM incumbents offering broad ecosystems augmented by AI-driven analytics; Londax’s advantages rest on customization flexibility tailored for SMBs but face pressure from entrenched players [S6][S9]. Compliance risks are material given potential penalties under GDPR or consumer protection laws if data or contractual practices fall short.

Capital scarcity presents further risk by constraining investments needed for product enhancement or marketing critical to customer acquisition and retention.

Outlook Considerations: Milestones to Monitor

No explicit forward guidance or milestones were disclosed beyond FY2025 results. Key indicators to watch include:

- User adoption growth rates indicating market acceptance;

- Churn metrics reflecting customer retention effectiveness;

- Customer acquisition cost trends signaling marketing efficiency;

- Progress expanding staff addressing operational scale bottlenecks;

- Technological enhancements elevating platform functionality;

- Regulatory compliance audits or certifications;

- Financing developments ensuring capital adequacy for growth.

These factors will be critical determinants of whether Londax can transform early momentum into sustainable competitive positioning within the European SMB CRM sector increasingly influenced by AI capabilities.

Disclaimer: This analysis is based solely on publicly available SEC filings as of April 7th, 2026 without projections beyond stated facts or news reports. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments