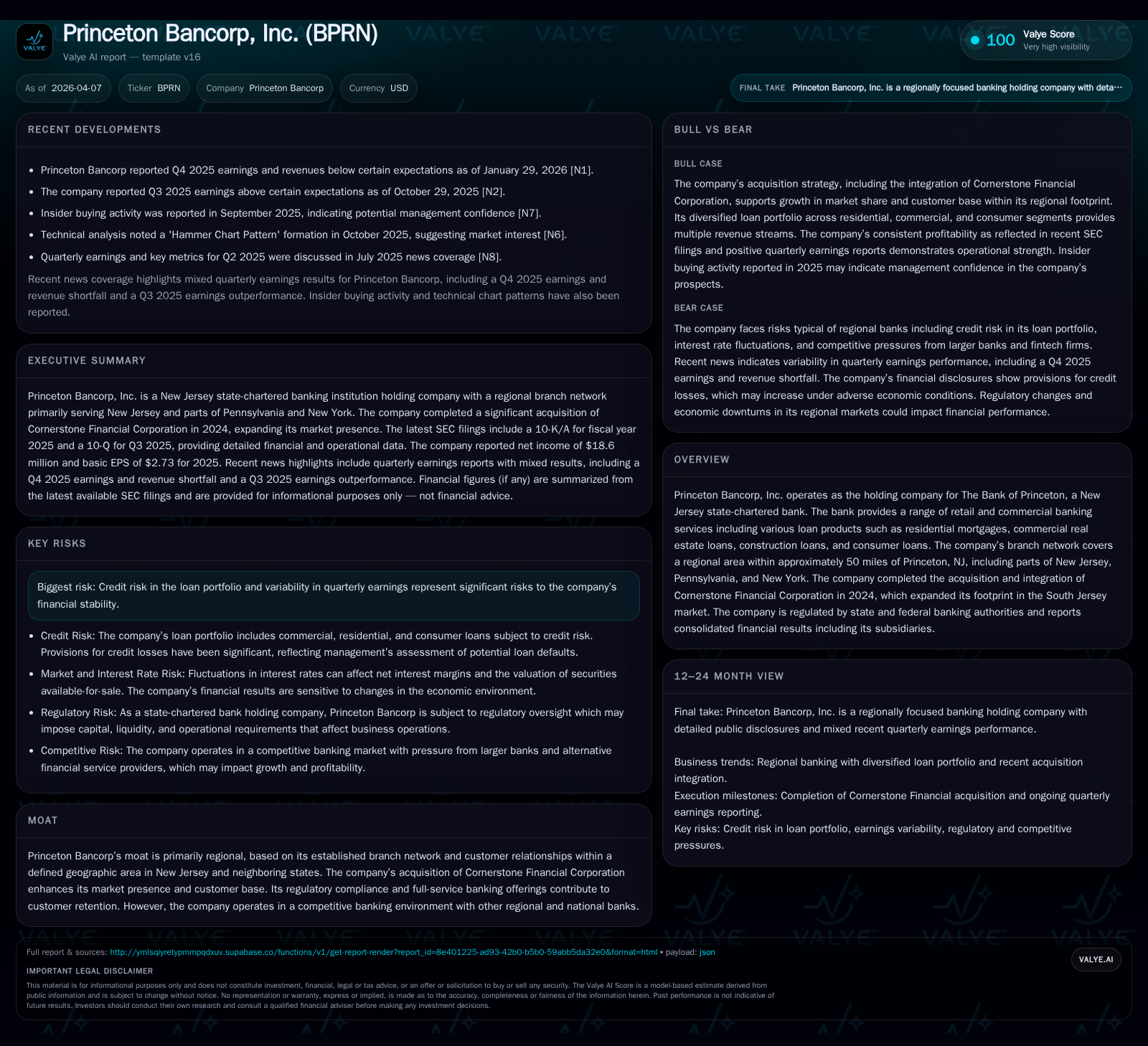

Princeton Bancorp Capitalizes on Regional Expansion and Loan Diversification

A detailed review of Princeton Bancorp’s strategic acquisition and balanced loan portfolio driving renewed financial performance.

Princeton Bancorp demonstrated a robust net income rebound of 81.7% in FY2025, supported by a nearly 46% surge in operating cash flows despite reduced capital expenditures. The strategic acquisition of Cornerstone Financial Corporation in 2024 expanded its South Jersey presence, bolstering the branch network and deposit base. The company maintains a diversified loan portfolio spanning residential mortgages, commercial real estate, and construction loans, with credit risk management remaining critical amid competitive pressures. Capital allocation reflects measured shareholder returns through dividends and increased buybacks, supporting an approximate ROE of 6.9%. Forward growth could hinge on efficient integration and credit loss trajectory monitoring.

Historical Financial Performance: A Tale of Recovery and Volatility

Princeton Bancorp’s financial trajectory from FY2022 through FY2025 illustrates significant swings particularly evident in net income results. After posting $26.5 million in net income for FY2022, the company experienced a downturn through FY2024 when net income declined to approximately $10.2 million — a substantial drop of over 60%. This contraction was largely driven by credit provisioning sensitivity amid evolving loan portfolio risk [F1]. However, FY2025 reversed this trend with an impressive rebound of 81.7%, culminating in $18.6 million net income.

Operating cash flow (CFO) similarly mirrors this pattern of volatility but demonstrates resiliency: CFO fell sharply in FY2024 but surged nearly 46% in FY2025 to $21.5 million despite capital expenditures (Capex) shrinking by 41.7%. Such dynamics suggest improved operational cash conversion possibly due to enhanced credit management and expense controls [F1]. Notably, Capex decreased after peaking in previous years, indicative of controlled investment likely due to branch network consolidation or efficiency initiatives.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 19 | 21 | 889000 | +81.7% |

| 2024 | 10 | 15 | 1525000 | -60.2% |

| 2023 | 26 | 23 | 1712000 | -2.8% |

| 2022 | 26 | 24 | 607000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 9 | 8 | 21 |

| 2024 | 8 | 1 | 13 |

| 2023 | 8 | 0 | 21 |

| 2022 | 6 | 9 | 23 |

Source: SEC companyfacts cache [F1].

In sum, Princeton Bancorp’s historical performance reveals a bank navigating earnings volatility primarily modulated by credit loss provisioning adjustments while maintaining a sturdy equity base that grew consistently albeit at a slower pace by the end of the period [F1].

Loan Portfolio Dynamics: Balancing Residential, Commercial, and Construction Lending

Core to Princeton Bancorp’s revenue generation is its diversified loan portfolio encompassing residential mortgages; commercial real estate loans; construction financing; and consumer loans including home equity lines [S14][S2]. Segmentation impacts risk profile since differing asset classes carry varying credit loss allowances tailored through underwriting rigor focused on financing receivables aging.

Residential first lien mortgages remain foundational with significant exposure emphasized through conservative underwriting standards to mitigate default risk [S25]. Commercial real estate loans reflect weighted average maturity considerations extending loan tenors tied to underlying collateral values within stable geographic markets surrounding Princeton.

Construction loans act as an extension avenue for commercial real estate lending but are inherently more sensitive to economic cycles hence higher scrutiny is applied via loan loss provisioning frameworks evidenced from management commentary [S10][S25]. Consumer loan segments provide yield diversification though are monitored closely for delinquencies beyond standard seasoning periods.

Allowance for credit losses is regularly evaluated against regulatory benchmarks driven by internal risk metrics including special mention/non-performing financing receivable ratios—metrics shared with banking examiners during routine evaluations ensuring adequacy aligned with observed asset quality trends [S4][S5].

This balanced approach serves to optimize net interest margin while managing downside risks within an intensely competitive regional banking environment marked by overlapping footprints from national scale banks.

Cornerstone Acquisition: Catalyzing South Jersey Market Penetration

The August 23, 2024 acquisition of Cornerstone Financial Corporation stands as a pivotal strategic event expanding Princeton Bancorp’s footprint notably within South Jersey markets [S14][S2]. This transaction involved integration of five additional branches anchored in Mt. Laurel—a key node extending reach into Burlington County and nearby suburban corridors.

Through stock consideration exchanges merging Cornerstone Bank into the company’s existing operations, Princeton Bancorp enhanced its deposit franchise density facilitating cross-selling opportunities across retail and commercial customer segments under a unified regulatory compliance regime [S14].

The transaction supports moat enlargement based on entrenched customer relationships augmented by full-service retail and business banking capabilities standardized across the enlarged network [S14]. Operational synergies include streamlined back-office functions alongside combined marketing efforts designed to drive deposit growth and loan origination strength.

Moreover, this geographic extension is coherent with the company's regional strategy focusing on contiguous markets within an approximately fifty-mile radius around Princeton—a well-defined service area allowing efficient management oversight by the chief operating decision maker (CODM) [S4].

Credit Risk Management in a Competitive Regional Banking Context

Credit risk remains one of Princeton Bancorp's primary financial stability challenges given the inherent variability across its loan portfolios [S4][S5]. The allowance for credit losses periodically adjusted upward throughout recent periods signals proactive management addressing pockets of non-performing assets concentrated within certain segments like construction or commercial real estate loans.

Detailed disclosures reveal that regulatory agencies engage regularly through examinations assessing both quantitative adequacy and qualitative underwriting policies ensuring alignment with evolving local market conditions [S4]. While no extraordinary reserve build has been mandated beyond normal course provisions recently, management underscores vigilance given economic cyclicality risks impacting borrower repayment capacity.

Metrics such as performing vs special mention classifications along with delinquency buckets (30-59 days through greater than ninety days past due) form integral elements guiding credit loss provisioning models [S25]. The bank also contends with pressure from larger regional banks competing for similar credits while managing profitability retention.

By sustaining disciplined underwriting standards complemented by active portfolio monitoring facilitated by integrated risk information systems post-Cornerstone merger, Princeton Bancorp aims to maintain credit quality thresholds consistent with stakeholder expectations yet flexible enough to capitalize on attractive lending opportunities locally.

Capital Structure and Allocation: Evaluating ROE, Dividends, and Buybacks

During FY2025 Princeton Bancorp exhibited prudent capital stewardship balancing reinvestment with shareholder returns [F1][S5]. Equity grew modestly by about 3.3% year-over-year to near $271 million driven primarily by retained earnings accumulation post net income improvement.

Dividends paid increased approximately 14%, totaling nearly $8.7 million reflecting consistent cash returns policy taking into account earnings recovery while maintaining capital buffers [F1]. Simultaneously share repurchases accelerated substantially from prior year levels reaching $7.9 million—a ninefold increase indicating management confidence in capital flexibility supporting stock price enhancement.

Derived return on equity approximates around 6.9%, which albeit moderate points to reasonable efficiency considering recent earnings volatility and elevated credit cost environment [F1]. Operating cash flow generosity relative to capex underpins free cash flow approximating $20.6 million allowing for continued capital allocation toward both organic growth investments and shareholder remuneration decisions.

Overall, capital strategy appears calibrated to sustain regulatory requirements while offering attractive features to investors without compromising balance sheet strength crucial for future strategic initiatives including potential acquisitions or technology upgrades.

Forward-Looking Growth Opportunities and Performance Indicators to Watch

While explicit future guidance is absent from available disclosures, key performance indicators warrant vigilant tracking given their influence on Princeton Bancorp's ongoing growth prospects:

- Loan loss allowance evolution: Post-acquisition integration period will reveal how synergistic effects stabilize or stress portfolio risk metrics affecting quarterly earnings runway.

- Net interest margin trajectory: The interplay between asset yields and funding costs amidst regional rate fluctuations will impact core profitability measures requiring close analysis.

- Branch network performance: Full operational integration success of Cornerstone branches alongside local market penetration gains may unlock incremental fee income sources.

- Liquidity adequacy: Monitoring core deposit growth rates vis-à-vis overall funding mix will signal franchise health amidst competitive deposit pricing dynamics.

- Regulatory capital ratios: Maintaining cushion compliant with state and federal mandates provides operating flexibility vital for navigating macroeconomic uncertainties.

These metrics collectively inform how Princeton Bancorp can leverage its regional competitive moat strengthened via acquisitions while balancing inherent credit risk exposures intrinsic to its diversified lending footprint.

This report has been prepared solely for informational purposes based upon publicly available data and received filings as of the stated dates without intention or recommendation regarding investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments