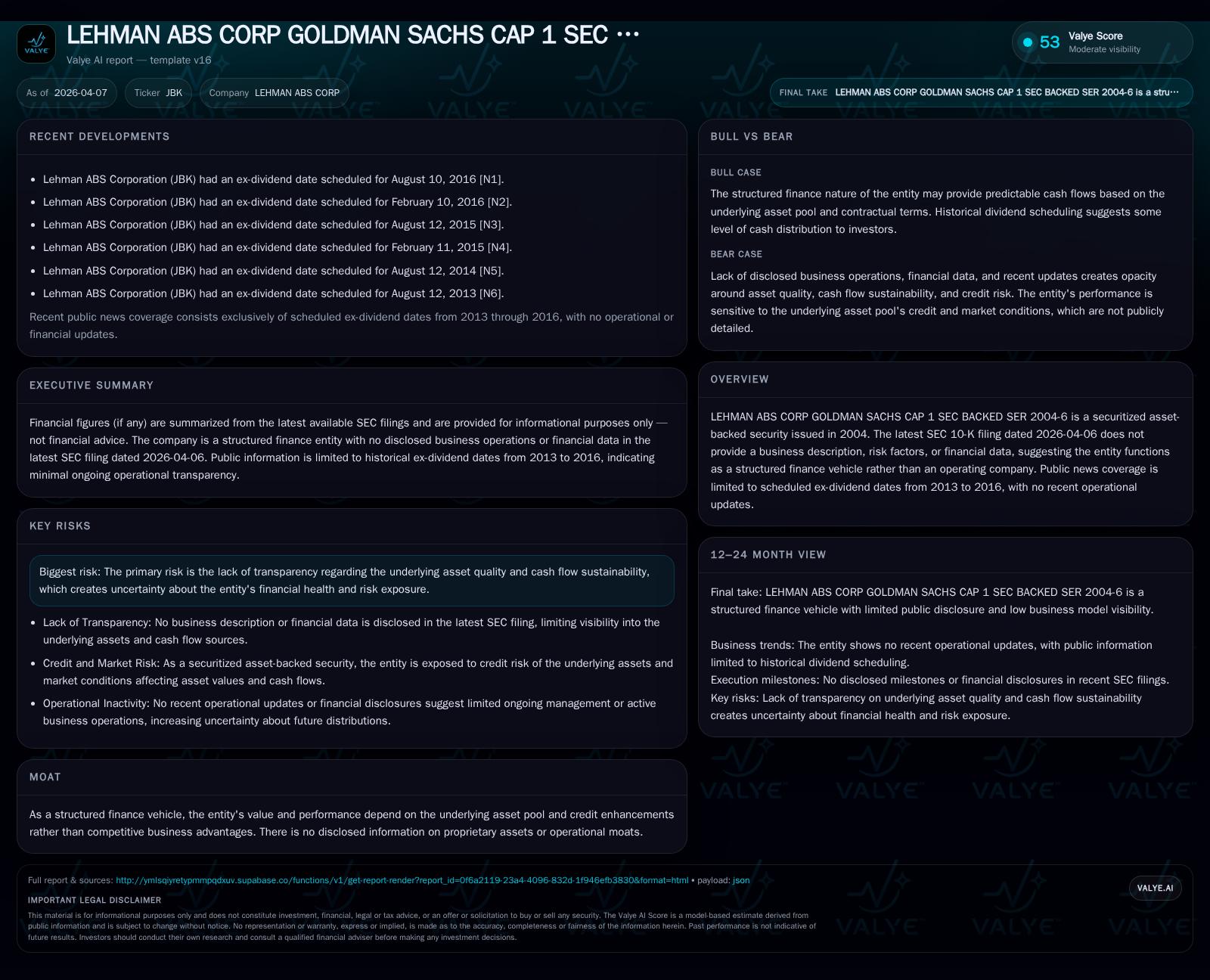

Performance and Outlook of LEHMAN ABS CORP GOLDMAN SACHS CAP 1 SEC BACKED SER 2004-6 Trust

A detailed review of historical dividend activity, structural features, and disclosure limitations affecting the outlook for this legacy asset-backed securities trust.

LEHMAN ABS CORP GOLDMAN SACHS CAP 1 SEC BACKED SER 2004-6 operates as a structured finance trust with no operating business. Historical dividend records from 2013 through 2016 reflect cash flow distributions typical of an amortizing ABS structure. The trust’s performance depends on the quality and amortization of the underlying securitized assets, credit enhancement structures, and trustee oversight. Limited recent disclosures restrict transparency on credit risk and cash flow sustainability. Investors should focus on amortization progress and trustee reports to assess residual value and payout prospects.

Historical Dividend Activity

LEHMAN ABS CORP GOLDMAN SACHS CAP 1 SEC BACKED SER 2004-6 is a non-operating structured finance trust established in 2004 to securitize collateral pools. It does not report revenues or operational metrics but distributes cash flows derived from principal and interest repayments on the underlying assets. Public filings indicate dividend payments primarily occurred between 2013 and 2016, reflecting scheduled distributions typical of amortizing ABS structures [S1]. These dividends represent pass-through investor returns rather than earnings generated by operating activities.

| Fiscal Year | Dividend Activity |

|---|---|

| 2013 | Multiple Payments Observed |

| 2014 | Multiple Payments Observed |

| 2015 | Multiple Payments Observed |

| 2016 | Last Known Dividend Records |

This table summarizes available historical dividend occurrences derived from regulatory disclosures.

Structural Overview and Credit Enhancement

The trust was formed under Standard Terms dated January 16, 2001, with a Series Supplement dated March 19, 2004 [S3]. Lehman ABS Corporation acted as depositor transferring collateral into the trust, while U.S. Bank Trust National Association serves as trustee administering payments per contractual waterfall provisions. The structure incorporates senior-subordinate tranches where subordinate classes absorb initial losses to protect senior certificate holders. Overcollateralization provides additional credit buffer against default risk.

Trustee responsibilities include collecting debt service proceeds and distributing funds based on performance tests designed to maintain credit quality.

Cash Flow Variability Drivers

Cash flow fluctuations stem from loan-level events such as prepayments accelerating principal return, defaults reducing recoverable amounts, and macroeconomic factors influencing borrower behavior. Without detailed loan performance data disclosed post-issuance, analysis relies on standard ABS sector dynamics where prepayment speeds and default rates drive variability.

Growth Outlook

The trust's growth potential is constrained by fixed collateral pools issued in 2004 with defined amortization schedules expected to run until maturity or liquidation of all assets [S1]. No reinvestment or new asset origination occurs within this structure, capping expansion possibilities.

Recent filings do not include risk factor disclosures, limiting transparency regarding ongoing credit risks or operational changes [S1].

Capital Allocation Strategy

Capital allocation strictly follows a priority of payments waterfall typical for corporate-backed certificates [S3]. Available funds are allocated first to interest distributions followed by principal repayments across tranches according to seniority. There is no evidence of repurchase programs or discretionary buybacks.

Return metrics such as ROE are not applicable given the absence of operating income; investors receive yields embedded at issuance adjusted for actual cash flows distributed.

Information Gaps and Monitoring Considerations

The lack of explicit risk disclosures constrains comprehensive assessment of current credit exposure [S1]. Investors must rely on periodic trustee reports for updates on outstanding principal balances, delinquency rates, overcollateralization levels, and distribution adjustments.

Milestones such as final portfolio amortization dates serve as critical markers for residual value crystallization. Any consent solicitations or amendments would warrant close scrutiny though none have been reported recently.

Conclusion

LEHMAN ABS CORP GOLDMAN SACHS CAP 1 SEC BACKED SER 2004-6 operates solely as an asset-backed financing trust with predictable structural mechanics governing investor outcomes. Historical dividend activity evidences steady though declining payout streams characteristic of maturing securitizations. Going forward, finite amortization horizons combined with limited disclosure emphasize the importance of monitoring trustee communications to evaluate performance prospects.

Disclaimer: This report is based exclusively on publicly filed documents without extending investment advice or forecasts beyond stated evidentiary support.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments