Cal Redwood Acquisition Corp.'s Value Creation Prospects within the Technology, Media & Telecommunications Sphere

CRAQ, a TMT-focused SPAC with substantial IPO capital, aims to leverage its management expertise for a strategic business combination.

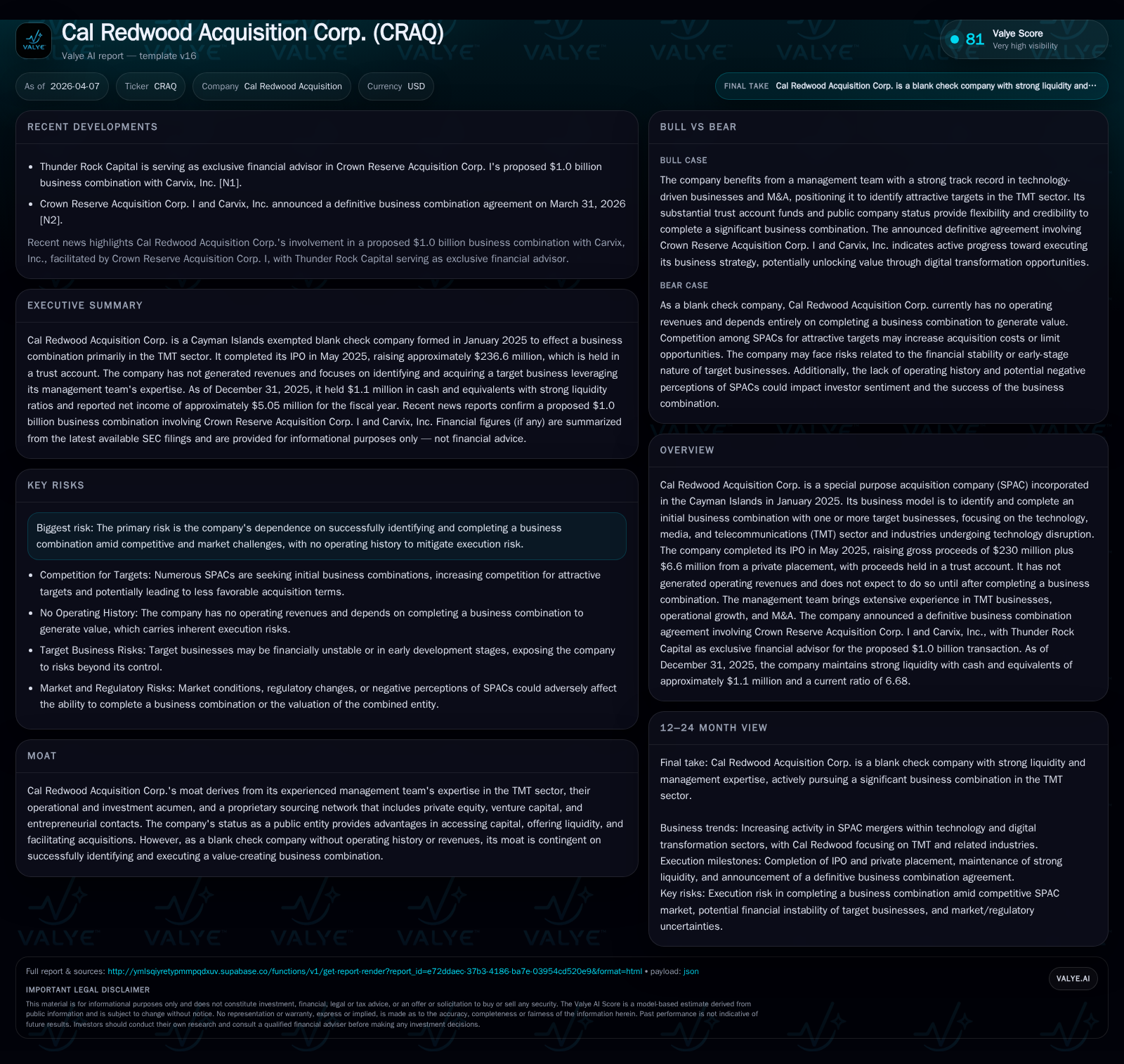

Cal Redwood Acquisition Corp. (CRAQ) launched its SPAC with an oversubscribed IPO raising $230 million plus a $6.6 million private placement, targeting tech-driven sectors within technology, media, and telecommunications. With no current operating revenues and activities limited to SPAC formation and target identification, CRAQ’s value hinges on successful execution of its business combination strategy. A recently announced definitive agreement involving affiliated entities and Carvix, Inc. highlights the management's active pipeline in the TMT sector. Key risks remain related to deal execution timing amid competitive acquisition landscapes; shareholders should monitor combination milestones closely.

IPO Inception and Initial Capitalization Details

Cal Redwood Acquisition Corp., incorporated in the Cayman Islands in January 2025, conducted its IPO on May 27, 2025. The Offering consisted of 23 million units priced at $10 each, fully exercising the underwriters' over-allotment option and generating gross proceeds of $230 million [S1][S3][S7]. Simultaneously, a private placement raised an additional $6.6 million from sponsor-related investors including Cohen & Company Capital Markets and Seaport Global Securities [S3][S8].

The gross proceeds were deposited into a trust account managed by Efficiency acting as trustee [S8][S13]. This trust holds funds primarily in U.S. Treasury Bills with maturities of 185 days or less or equivalent money market funds, safeguarding capital until use for an initial business combination or potential shareholder redemptions [S1][S13]. The company incurred underwriting fees totaling over $14 million including both cash and deferred components [S1]. The trust account structure aligns with standard SPAC mechanics providing investor protections with limited access to principal prior to deal closing.

Historical Financial Activity and Operating Metrics Since Inception

CRAQ has not commenced operations or generated revenues as it remains pre-combination [S1]. Its income for FY2025 totaled roughly $5.05 million stemming entirely from investment earnings on securities held within the trust account ($5.63 million) plus bank interest ($26 thousand), offset by operating expenses including compensation ($132k) and administrative costs ($468k) [F1][S1].

Cash outside the trust amounted to approximately $1.1 million at year-end 2025, covering due diligence and corporate expenditures [F1]. The company reported current assets of about $1.2 million against current liabilities near $180 thousand yielding a strong current ratio of 6.68x, reflecting robust short-term liquidity [F1]. Return metrics such as ROE are negative (-62.1%) given absence of operating profit coupled with equity accounting methods [F1]. These figures underline that financial performance remains driven solely by capital management before consummation of a target merger.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Net income stems largely from trust earnings netted against public company operating costs [F1].

Management Expertise and Strategic Sourcing in Technology, Media, and Telecommunications

CRAQ's moat fundamentally derives from its executive team's established expertise across TMT sectors known for rapid technological shifts [S1][N1][N2]. Board composition includes leaders with operational backgrounds in venture capital and private equity spaces emphasizing tech-enabled growth businesses [S3]. The company maintains an extensive sourcing network combining relationships within PE firms, VC investors, and entrepreneurial ecosystems that enable access to proprietary deal flow often unavailable to competitors.

This strategic positioning is crucial given heightened competition among SPACs vying for quality technology targets undergoing digital transformation across disparate subsectors — ranging from software services to telecom infrastructure upgrades [N2]. Management's ability to efficiently filter opportunities while leveraging cross-sector knowledge aims to enhance post-combination value creation through multi-vector growth rather than piecemeal acquisitions alone.

The Definitive Business Combination Agreement: Key Terms and Strategic Rationale

While CRAQ has yet to close its own initial business combination transaction as per filings [S1], it announced a definitive agreement tied closely with Crown Reserve Acquisition Corp. I involving Carvix, Inc., a transaction backed financially by Thunder Rock Capital serving as exclusive advisor [N1][N2]. This deal exemplifies CRAQ-connected parties executing large-scale TMT integrations reflecting complementary strategic fits focusing on tech disruption-based growth initiatives.

Though technically external to CRAQ’s balance sheet at this time, this partnership signals the management’s active engagement within their pipeline sourcing framework targeting high-value deals exceeding $1 billion valuations in digital mobility sector niches primarily serviced by Carvix’s offerings. Thunder Rock Capital’s advisory role adds credibility around structuring optimal financing solutions blending cash and equity considerations during such mergers.

Evaluating Growth Enablers and Sector Focus Post-Combination

Post-closing growth vectors anticipated revolve around technology sectors experiencing transformative disruption through digital innovation — a domain where CRAQ's management holds particular proficiency [S1][N2]. Potential target businesses may span sub-industries such as next-gen telecommunications infrastructure enhancements (e.g., 5G related services), cloud-native media platforms reshaping content distribution models, or SaaS providers innovating workflows for traditional industries undergoing IT modernization [S1].

Given the emphasis on multi-vector value creation post-transaction involving synergies from operational scaling combined with expanded product adjacencies within TMT segments, CRAQ’s prospects hinge on aligning market-leading technology platforms benefiting from secular trends like IoT expansion, AI adoption curves in communications systems,and evolving consumer media consumption habits.

Capital Allocation Priorities and Shareholder Return Potential

CRAQ’s capital allocation currently prioritizes preservation rather than return distributions typical pre-combination for SPAC structures [S3][S7][S9]. Gross proceeds nets after underwriting expenses primarily reside in the trust account dedicated solely towards funding the consummation of its eventual business combination or fulfilling redemption obligations if no suitable deal materializes within designated deadlines [S13].

Outside fund availability (~$1.1 million) allows financing of administrative overheads including due diligence expenses but does not support dividends or stock buyback programs at this stage — standard practice given unproven operational cash flow generation capacities thus far [F1][S3][S7]. Post-business combination capital returns will be contingent upon profitability trajectories established by combined entity fundamentals rather than baseline SPAC activity.

Risks Shaping Execution of the Initial Business Combination

The principal risk lies in successfully completing an attractive transaction amidst intense competition across TMT targets given abundant buyer activity within disrupted technology markets [S4][S5][S6][S1]. As a blank check company lacking any operating history or independent revenue generation capabilities prior to merger completion, CRAQ exposes shareholders to uncertainties related to target valuation accuracy, deal structure complexity, and integration risks inherent when forming new combined enterprises. Additional risks involve timing constraints since the company faces mandatory redemption deadlines approximately two years after IPO closing subject to extension approvals which amplify pressure on execution pace.[S4] No material litigation or governmental proceedings currently affect CRAQ according to recent disclosures,[S1] mitigating legal downside beyond inherent transaction risks.

Key Milestones Ahead: What Investors Should Monitor

Investors ought to follow progress on CRAQ’s completion timetable of its initial business combination closely alongside shareholder votes approving such mergers. Regulatory approvals—as applicable depending on target jurisdictions—will also be key milestones signaling deal viability. Monitoring engagement updates from financial advisors like Thunder Rock Capital provides insights into transaction structuring developments impacting deal terms.[N1] Stock price movements around deal announcements may reflect market sentiment improvements tied directly to clarified growth outlook post-business combination closure—which remains pivotal given absence of standalone fundamental results until then.

Disclaimer: This analysis is for informational purposes only reflecting publicly available data as of April 2026 without investment advice or recommendations. Readers should perform independent due diligence before making any financial decisions regarding Cal Redwood Acquisition Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments