Anbio Biotechnology’s Shift from Pandemic Revenues to Diversified Diagnostic Growth

Anbio successfully transitioned from COVID-19 testing reliance to a broad in vitro diagnostic portfolio, demonstrating robust profitability and strategic capital use in 2025.

Anbio Biotechnology matured financially during the COVID-19 pandemic by supplying respiratory disease tests but has since pivoted towards expanding its diversified in vitro diagnostic (IVD) product range. The company posted a 5.6% revenue increase in 2025 driven by growth in non-COVID and customized products, alongside a striking nearly tripled operating income and nearly 170% net income surge. Strong gross margin expansion and disciplined cost controls underpin these results. While operating cash flow turned sharply negative due to working capital build and investing outflows, Anbio maintains ample liquidity with a high current ratio. Its strategy includes global regulatory registrations, product line extension into veterinary diagnostics and dry chemistry, and optimization of supplier agreements, positioning it for continued growth amid industry competition and regulatory risks.

From Pandemic Origins to Sustained Sales Growth

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9 | 6 | -7 | 6 | +5.6% | +169.9% |

| 2024 | 8 | 2 | 2 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 21.2 |

| 2024 | 13.8 |

Source: SEC companyfacts cache [F1].

Founded in mid-2021, Anbio Biotechnology rapidly matured financially during the COVID-19 pandemic by supplying respiratory disease tests including SARS-CoV-2 rapid antigen assays internationally to markets such as France and Germany [S1]. Revenues showed substantial growth from $6.7 million in 2023 to $8.19 million in 2024 (+21.9%), driven primarily by an expanded portfolio beyond COVID-19 testing into other IVD areas and an enlarged customer base across regions [F1][S4]. In 2025, total revenue further increased modestly by approximately 5.6% to $8.65 million, reflecting normalization of COVID-related demand but offset by growth in non-COVID conventional IVD products, animal diagnostics, and custom orders [F1][S4]. This transition from pandemic reliance toward multi-segment diagnostic offerings provides Anbio a broader foundation for sustained growth.

Diversified Diagnostic Portfolio Fuels Competitive Moat

Anbio's product suite covers multiple diagnostic platforms including laboratory-based assays, wellness panels, at-home kits, and point-of-care testing (POCT). The portfolio addresses diverse clinical areas such as infectious diseases (beyond SARS-CoV-2), cancer markers, cardiovascular indicators, pharmacogenomics assays, hormonal tests, allergy panels, diabetes monitoring, and drug abuse screening [S1]. Notably, Anbio has strategically expanded into veterinary diagnostics as well as dry chemistry methodologies suitable for decentralized testing environments—efforts currently progressing through regulatory registration processes globally [S1]. The company leverages well-established IVD technology platforms rather than pioneering wholly novel mechanisms, aiding faster commercialization but requiring ongoing innovation to remain competitive in a fast-evolving market segment with complex regulatory landscapes [S16][S23]. Contractual arrangements with suppliers include advance price notifications that help manage input cost volatility amid global supply chain uncertainties—an important risk mitigant in the biomedical device space.

Analyzing 2025 Financial Performance: Profitability Surges Amid Revenue Growth

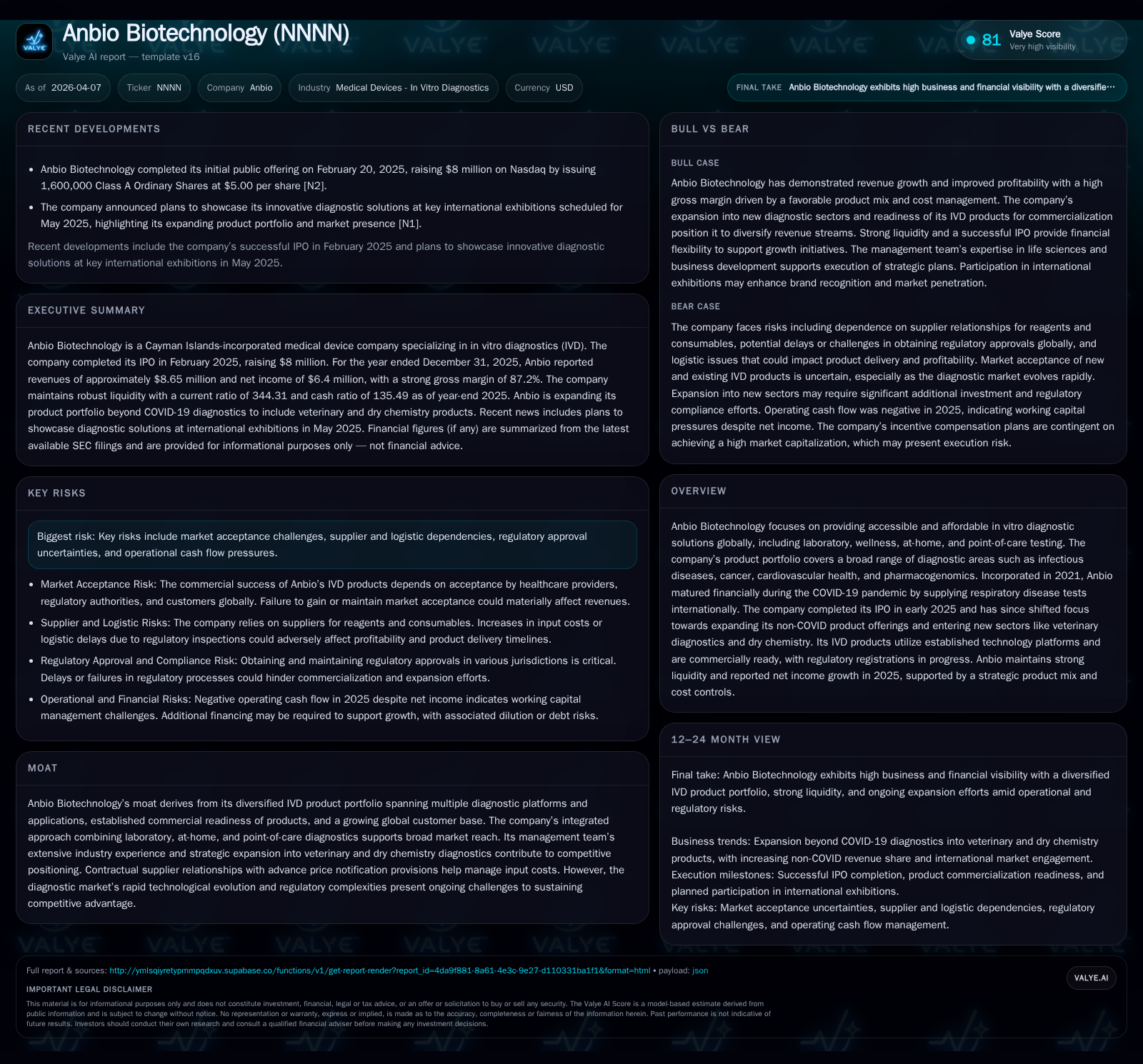

The fiscal year ended December 31, 2025 demonstrated notable profitability improvements even on moderate revenue gains. Revenue reached $8.65 million (+5.64% YoY), supported by steady orders from key clients including increased demand for customized IVD products tailored to regional markets or specific customer needs [F1][S4]. Operating income more than doubled to about $5.77 million — up +189% YoY — fueled by improved unit economics driven by shifting product mix toward higher-margin offerings along with tighter procurement cost controls and disciplined pricing strategies [F1][S4]. Gross profit rose sharply to $7.54 million yielding an exceptional gross margin of approximately 87%, up from roughly 72% the prior year—clearly reflecting enhanced sales profitability and resource leverage within their commercialized product lines [F1][S4]. Selling, general & administrative expenses fell substantially (-54%) following reduced one-time IPO preparation costs and ongoing cost control measures without impairing core operations [S7]. Net income achieved a significant jump to $6.40 million (+170%) highlighting favorable operating leverage and effective expense management in context of the laboratory diagnostics market.

Capital Deployment Strategy Highlights Reinvestment and Shareholder Returns

The company's February 2025 IPO raised gross proceeds of approximately $8 million which are being strategically deployed toward enhancing production capacity for diversified non-COVID IVD products as well as supporting regulatory registrations and global commercial expansion efforts [S1][S5]. While no cash dividends have been distributed yet—a typical stance for early-to-mid stage biotech enterprises aiming at reinvestment—the board retains discretion under Cayman Islands law with flexibility on dividend declarations when warranted by future earnings stability and capital needs [S12][S13]. Share repurchases have not been reported indicating prioritization of growth investments over capital return programs at this stage.

Based on FY2025 equity of around $30.15 million versus net income of approximately $6.40 million yields an estimated return on equity near 21%, signaling strong capital efficiency relative to its size and growth phase [F1]. Continued reinvestment is evidenced by elevated capex levels supporting R&D validation activities geared toward regional regulatory filings rather than new product development which has moderated as the current portfolio matures [S7][S10].

Operating Cash Flow Dynamics and Working Capital Management

Despite strong profits, operating cash flow reversed dramatically from positive $2.08 million in FY2024 to an outflow of nearly -$6.74 million in FY2025 reflecting substantial increases in accounts receivable ($2.59 million), prepayments ($8.39 million), and prepaid expenses aligned with scaling operational infrastructure ahead of anticipated sales growth along with inventory adjustments amidst expanding product offerings [F1][S18][S21]. These changes correspond to typical supply chain and customer financing terms management common at this stage as companies invest working capital aggressively anticipating greater future turnover.

Nonetheless, liquidity remains robust with cash & equivalents of approximately $7.77 million coupled with an extraordinarily high current ratio exceeding 344x attributable largely to minimal current liabilities ($87K) relative to current assets (~$30.24M), underscoring sound balance sheet management supporting ongoing expansion plans despite near-term cash flow pressures [F1].

Global Regulatory and Commercial Expansion Challenges

Launching diagnostic assays globally necessitates navigating stringent regulatory environments which remain a key challenge for Anbio's planned international footprint expansion efforts especially into veterinary medicine segments that entail distinct clearances compared to human diagnostics [S1][S16]. Though no major setbacks are expected currently for obtaining approvals derived from established technology platforms' scientific substantiation processes, delays or failures could materially impact commercial timelines.

Moreover, market acceptance depends heavily on endorsements from healthcare providers’ key opinion leaders alongside successful reimbursement negotiations with payors—a critical barrier given varying insurance schemes across regions that significantly influence test adoption rates within decentralized testing frameworks like POCT or at-home kits common in the IVD industry [S23]. Supplier continuity also represents a tangible risk given reliance on third-party vendors for raw materials where contract terms mitigate price shocks yet do not eliminate exposure completely amid evolving global supply chain risks.

Future Outlook: Product Pipeline and Market Penetration Focus Areas

While explicit formal forecasts are not provided by management currently ([N/A]), publicly disclosed plans emphasize concentrated efforts on extending penetration across existing IVD subsegments while broadening into veterinary diagnostics as well as dry chemistry assays advantageous for rapid point-of-use settings [S1]. The company's ability to capitalize on these opportunities depends on sustaining technological relevance amidst rapid sector innovation cycles as well as executing regulatory submissions successfully.

Growth constraints center chiefly on achieving wide-scale market acceptance beyond initial customers which entails addressing user preferences for convenience alongside technical accuracy; mitigating reimbursement hurdles; maintaining supplier reliability; and competing against entrenched incumbents entrenched through longstanding distribution networks common within the fragmented global diagnostic device space.

Risk Factors Impacting Market Acceptance and Operational Stability

Key risks documented include dependencies on continuing relationships with suppliers critical for manufacturing scale-up; uncertainties around timing of regulatory approvals potentially delaying go-to-market launches; operational cash flow pressures evidenced by recent negative CFO trends even amid profits indicating potential liquidity tightness if expansion outpaces financing sources; foreign issuer status exemption from certain Nasdaq governance protections possibly affecting investor perception; plus exposure to fluctuating demand typical of cyclical diagnostic testing markets influenced by shifting public health priorities such as pandemic ebbing phases or emergent infectious threats [S16][S26].

Overall Anbio’s strategy incorporating diversification across multiple diagnostic verticals combined with prudent management of resources positions it strongly for sustainable long-term growth despite these inherent sectoral challenges.

This analysis synthesizes publicly filed financial data and company disclosures without offering investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments