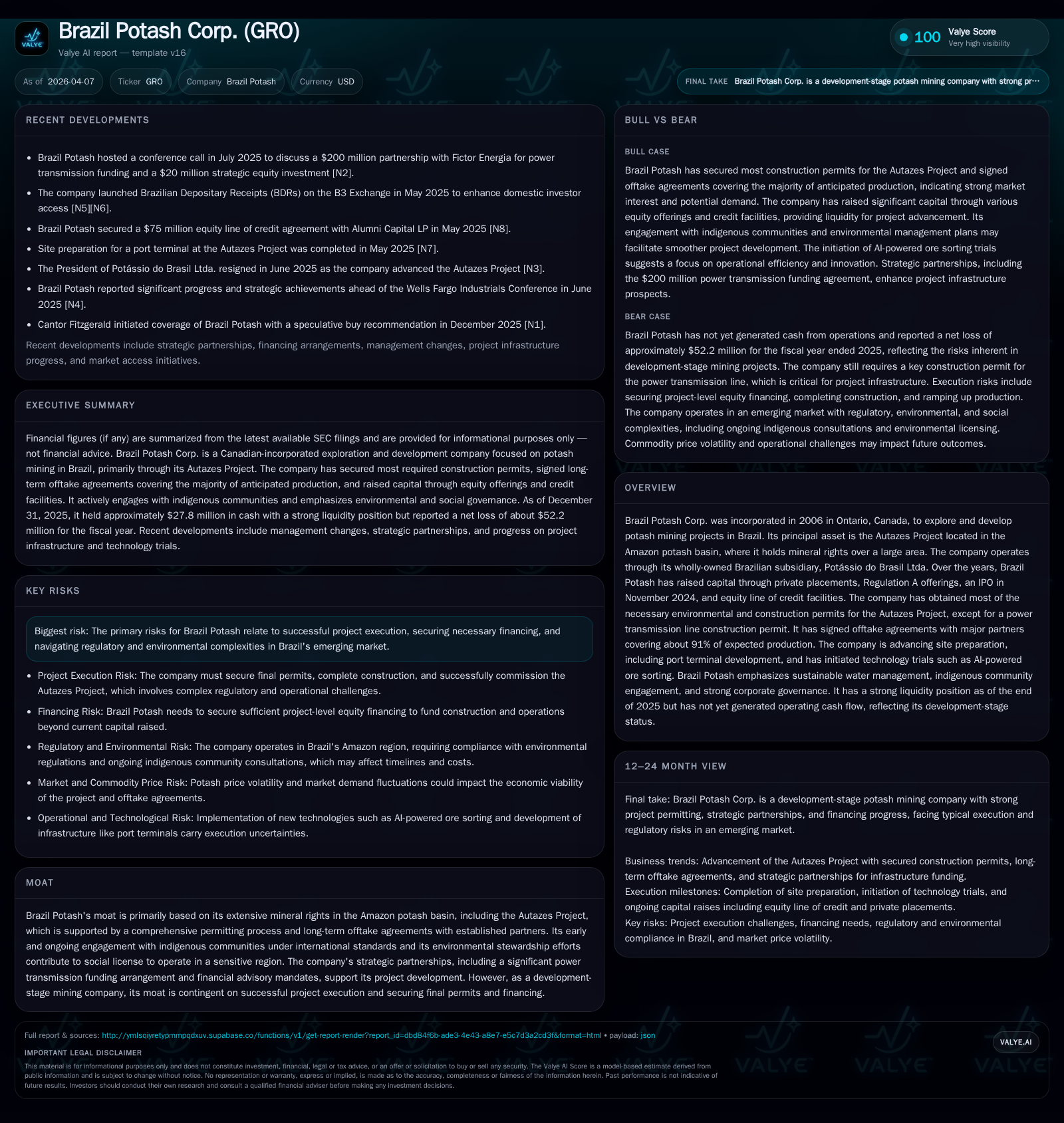

Brazil Potash’s Autazes Project Faces Execution and Regulatory Challenges Amid Development Push

Brazil Potash Corp. advances its Amazon basin potash mining project, balancing permitting hurdles and financing needs.

Brazil Potash Corp., through its wholly-owned Brazilian subsidiary, focuses on the Autazes Project in the Amazon potash basin. Since incorporation in 2006, the company has raised significant capital via private placements, a Regulation A offering, an IPO in late 2024, and equity line facilities to fund exploration and development. Progress includes obtaining nearly all construction permits except the critical power transmission line license, alongside binding offtake agreements covering over 90% of expected production. The company faces ongoing litigation risks related to environmental licensing and indigenous consultations but maintains strong engagement with local communities. Financially, Brazil Potash remains pre-revenue with negative net income and robust equity supporting continued development, highlighting the importance of successful project execution and securing additional financing.

Company History and Strategic Foundations

Founded in 2006 in Ontario, Canada, Brazil Potash Corp. was established to explore and develop potash resources in Brazil’s Amazon basin. Its principal asset is the Autazes Project where it holds extensive mineral rights across approximately 680 square miles. Since incorporation, Brazil Potash has advanced from exploration through permitting by raising roughly $300 million through private placements, a Regulation A offering ($40.5 million), a November 2024 IPO ($30 million gross proceeds), and multiple equity line credit facilities [S1][S8].

Historical Performance and Capital Development

Brazil Potash remains pre-revenue with no cash generated from operations to date. Net losses increased from approximately -$46 million in 2024 to -$52 million in 2025 due to expenditures related to project advancement and operational readiness [F1]. Equity grew from $135 million to nearly $158 million year-over-year reflecting capital raises that underpin liquidity and balance sheet strength [F1]. As of December 31, 2025, cash and equivalents stood at about $28 million—sufficient for near-term activities but necessitating further funding for construction completion [F1][S8].

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | -52 | -12.4% |

| 2024 | -46 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -33.0 |

| 2024 | -34.3 |

Source: SEC companyfacts cache [F1].

This table highlights increased net losses consistent with project ramp-up costs alongside strong liquidity metrics [F1].

Project Status and Permitting

The Autazes Project has secured all required environmental and construction licenses except for one critical permit: the construction license for the power transmission line linking the mine to Brazil’s national electricity grid remains outstanding [S8]. Extensive consultations with indigenous communities were conducted in accordance with International Labour Organization Convention 169 standards as part of licensing conditions [S6][S18][S19]. Legal challenges include a May 2024 civil lawsuit contesting environmental licenses that led to temporary suspensions; however, appellate courts have reinstated these licenses multiple times [S4][S12][S20].

Offtake Agreements and Market Position

Binding offtake agreements cover about 91% of anticipated production capacity with contract durations ranging from ten to seventeen years. Key counterparties include industry participants such as Keytrade Commodities, Kimia Research, and Amaggi Group [S8]. These agreements provide revenue visibility upon commencement of production.

Community Relations and ESG Commitment

Brazil Potash has established a robust social license strategy featuring early engagement with the Mura indigenous peoples—the predominant regional indigenous group—through a preliminary cooperation agreement signed in January 2025. This agreement includes frameworks for sustainable development programs ("Plano Bem Viver Mura"), social investments, cultural initiatives, and socioeconomic support aligned with environmental compliance requirements [S18][S19]. Local employment initiatives focus on training residents for operational roles while prioritizing procurement from indigenous-owned businesses.

Environmental stewardship plans aim for near-complete recirculation of process water to minimize consumption while managing tailings through natural dissolution combined with underground pumping into aquifers to reduce surface contamination risks [S18]. Reflecting these efforts, Brazil Potash received an "A" ESG rating from MSCI [S9].

Financial Position: Capital Allocation & Executive Compensation

No dividends or share repurchases are currently authorized given capital allocation priorities focused on advancing construction and commissioning phases [S5][S7][S10][S11][F1]. Executive compensation includes base fees under consulting agreements aligned with market benchmarks and evolving incentive awards under a 2024 Incentive Compensation Plan designed to enhance retention and align interests with shareholder value creation [S1][S5]. The board comprises a majority of independent directors consistent with NYSE American governance standards [S10].

Future Growth Prospects & Potential Constraints

Near-term priorities center on initiating primary infrastructure construction once outstanding permits—including the transmission line license—are secured. A partnership with Fictor Energia provides approximately $200 million funding under a build-own-operate-transfer (BOOT) model plus a $20 million strategic equity investment that alleviates some upfront capital requirements but underscores reliance on third-party execution capabilities [S8].

Project execution risks remain elevated due to environmental sensitivities inherent to Amazon operations alongside regulatory uncertainties evidenced by recurring litigation despite favorable appellate outcomes [S3][S4][S12]. Financing risk persists as substantial incremental capital will be needed beyond current cash balances despite recent financings. While offtake contracts offer downstream visibility, commodity price volatility and Brazilian infrastructure constraints present logistical challenges potentially impacting costs.

Sector fundamentals reflect growing global demand for potash fertilizers—especially across Latin America—supporting the strategic rationale behind Brazil Potash’s positioning if operational challenges are effectively managed.

Monitoring Milestones

Key developments to watch include final approval of the power transmission line permit; commencement progress on main site infrastructure; adherence to feasibility study targets; additional equity or debt financings; construction ramp-up timelines; resolution status of legal disputes; updates on indigenous community relations; and eventual commissioning or production announcements.

Conclusion

Brazil Potash Corp. exemplifies a classic resource development profile anchored by strategic mineral assets in an emerging Brazilian potash market poised to impact domestic fertilizer supply chains. Its competitive advantage stems from secured mineral rights combined with comprehensive permitting progress supported by proactive indigenous engagement under international frameworks.

However, the company faces notable execution risks associated with environmentally sensitive operations subject to complex regulatory scrutiny requiring continued capital deployment without operational track record. While equity levels provide runway buffers, further fundraising appears likely as construction advances. Investors should closely monitor regulatory outcomes related to pending permits—particularly power infrastructure—and financing developments critical to transitioning from development toward production.

This analysis is based solely on publicly available data as of April 2026 from SEC filings supplemented by proprietary insights into resource project development economics. It does not constitute investment advice or a recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments