Kaixin Holdings’ Operating Losses Persist Amid Strategic Restructuring and Diversification

Kaixin Holdings faces continued operating challenges with significant losses in 2025, while pursuing strategic acquisitions and diversification into electric vehicles and AI education. Liquidity constraints and restructuring efforts shape near-term outlook.

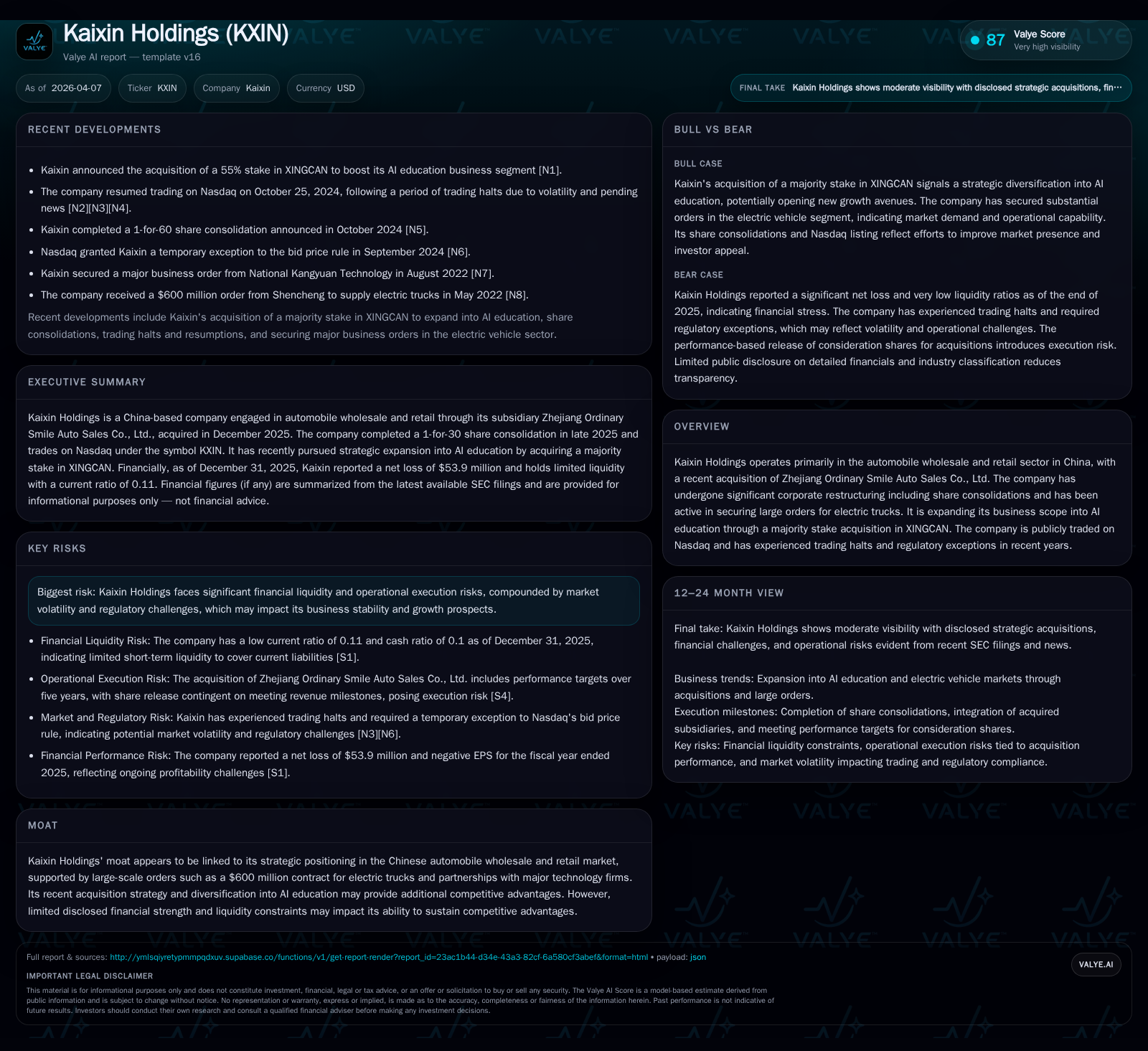

Kaixin Holdings, a China-based premium auto dealership group, reported a 65% year-over-year decline in operating income to a loss of $31.6 million in 2025. The company’s core vehicle sales operations contracted sharply with zero new or used vehicle sales recorded in recent years. Strategic moves include acquiring Zhejiang Ordinary Smile Auto Sales, entering electric truck wholesale with a $600 million order backlog, and expanding into AI education through majority ownership in XINGCAN. Liquidity remains tight with a current ratio of 0.11, prompting a 1-for-30 share consolidation completed late 2025. No dividends or share repurchases have been declared amid ongoing net losses and negative cash flow from operations.

Historical Performance and Market Position

Kaixin Holdings operates as a premium new and used automobile dealership group primarily focused on premium brands such as Audi, BMW, Mercedes-Benz, Land Rover, and Porsche within China [S1]. As of December 31, 2024, it maintained three dealerships across three cities but reduced to one dealership by the end of 2025 following disposals and dissolutions of low-operation subsidiaries during 2024 and early 2025 [S1]. The company sourced approximately 525 vehicles sold in 2023 but reported no new or used vehicle sales in both 2024 and 2025, indicating a significant contraction in its core sales activities [S1]. This volume decline reflects broader structural challenges including shifts in consumer sentiment among affluent individuals and regulatory factors affecting passenger vehicle demand.

Financial Trends: Persistent Losses during Restructuring

From FY2022 through FY2025, Kaixin Holdings consistently reported operating losses despite some improvement over time. Operating income was negative $47.9 million in FY2022 improving to negative $31.6 million by FY2025—a year-over-year decrease of approximately 65% from the prior year’s already negative $19.1 million figure [F1]. Net income mirrored this trend with losses narrowing from $84.7 million in FY2022 to $53.9 million in FY2025 but remaining substantial [F1].

Operating cash flow remained negative but showed slight improvement from -$3.02 million in FY2024 to -$2.58 million in FY2025 while capital expenditures were minimal at $18,000 for both years, indicating limited reinvestment capacity during this period [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -54 | -3 | -32 | 18000 | -31.6% |

| 2024 | -41 | -3 | -19 | 18000 | +23.5% |

| 2023 | -54 | -2 | -21 | 396000 | +36.8% |

| 2022 | -85 | -2 | -48 | 59000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -245.8 |

| 2024 | -3 | -311.0 |

| 2023 | -3 | -117.5 |

| 2022 | -2 | -270.5 |

Source: SEC companyfacts cache [F1].

Strategic Diversification: Electric Vehicles and AI Education

Kaixin has pursued strategic expansion beyond traditional auto retailing through acquisitions and new business lines. Notably:

Acquired Zhejiang Ordinary Smile Auto Sales Co., Ltd., now an indirect wholly owned subsidiary; the acquisition consideration includes up to $15 million in shares subject to escrow release contingent on five-year revenue performance targets ending November 2030 [S6; S7].

Secured an electric truck order backlog valued around $600 million demonstrating entry into China’s growing commercial electric vehicle market segment aligned with decarbonization goals [S6].

Extended into artificial intelligence education via majority ownership of XINGCAN reflecting diversification into technology-driven service sectors outside automotive wholesale retailing [S7].

These initiatives suggest an evolving business model aimed at offsetting pressures on legacy vehicle sales operations.

Capital Structure and Liquidity Profile

Kaixin Holdings faces significant liquidity constraints evidenced by current assets of approximately $1.02 million versus current liabilities near $8.96 million at fiscal year-end 2025 for a current ratio of about 0.11—indicating severe working capital limitations [F1].

To address market trading considerations amid financial challenges the company executed a reverse share split at a ratio of one-for-thirty finalized end-2025 aiming to enhance per-share metrics and investor perception without declaring dividends or initiating share repurchases due to ongoing losses [S4; S5]. Equity increased from roughly $13.2 million to over $21.9 million between years likely reflecting equity issuance linked to acquisitions rather than profitability improvements [F1; S8].

Operational Model and Risk Considerations

Kaixin employs an omni-channel retail strategy integrating physical dealerships with online platforms including third-party automotive advertising enabling broader consumer reach within China’s fragmented car retail industry [S1]. This hybrid approach aims for operational efficiency through digital engagement coupled with traditional showroom presence.

Robust cybersecurity governance is maintained with board oversight supported by experienced internal teams focusing on risk mitigation through quarterly reporting frameworks addressing data security threats—a key operational risk factor [S1].

Risks remain elevated given financial liquidity pressure combined with regulatory complexities inherent to cross-sector operations spanning automotive sales licensing frameworks and emerging technology service compliance within China’s dynamic regulatory environment.

Outlook: Execution Focus Amid Uncertain Timing

While explicit forward-looking guidance is limited within available filings management execution against the sizeable electric truck order backlog along with revenue milestones tied to the AI education acquisition will be critical indicators for future growth potential [S6; S7]. Investors should also monitor any developments regarding dealership network expansion or consolidation alongside effectiveness of digital marketing efforts integral to sustaining customer acquisition.

This analysis is based exclusively on publicly filed SEC documents through April 7, 2026 ([F1], [S1]–[S14]) without speculative assumptions or private information access.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments