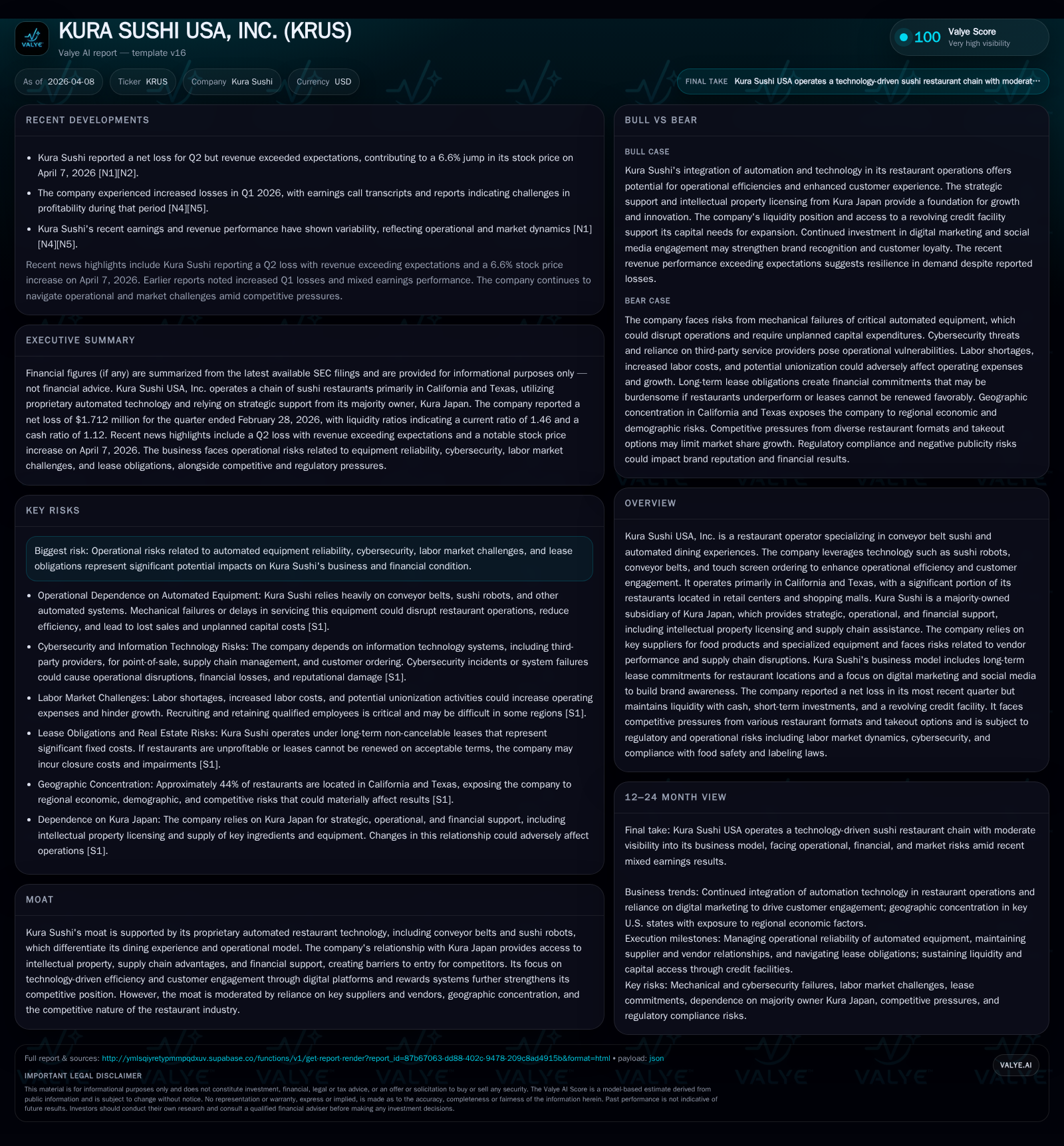

Kura Sushi USA’s Journey Through Innovation and Profitability Challenges

Kura Sushi USA leverages sophisticated automated dining technology to spur growth while grappling with persistent operational losses and heavy capital requirements.

Kura Sushi USA, Inc. operates a technologically advanced conveyor belt sushi restaurant chain focused mainly in California and Texas. Despite its innovative use of sushi robots, conveyor belts, and digital customer engagement systems forming a unique moat, the company has transitioned from a modestly profitable FY2023 to operating losses in FY2024 and FY2025 driven by inflationary pressures and heightened capital expenditures. While operating cash flow remains positive and has grown year-over-year, free cash flow remains significantly negative due to sustained high investment in automation infrastructure. Kura Sushi’s capital allocation strategy reflects a reinvestment approach without dividends or buybacks, underscoring its prioritization of expansion and technological enhancements. Future growth will hinge on managing vendor reliability, geographic concentration risks, and operational improvements tied to automated kitchen robotics.

From Profitability to Losses: Tracing Kura Sushi USA’s Financial Performance

Kura Sushi experienced a notable swing in financial results over the past four fiscal years. In FY2023, the company reported a narrow operating income of $0.33 million after a series of prior losses, signaling a temporary operational improvement [F1]. However, this uptick proved short-lived as FY2024 saw operating income decline sharply to -$11.5 million, followed by a narrower loss of -$4.8 million in FY2025 [F1]. Net income followed a similar trajectory, turning positive in FY2023 at roughly $1.5 million before plunging back into negative territory with losses of $8.8 million in FY2024 and further narrowing to $1.9 million loss in FY2025.

Despite these losses at the bottom line, operating cash flows tell a more nuanced story; CFO rose from $18.1 million in FY2023 to $24.7 million in FY2025 — an increase of approximately 58% year over year [F1]. This divergence between operating losses and solid cash flow generation highlights non-cash expenses or investments weighing on profitability.

The widening losses correspond closely with inflationary pressures cited directly by the company [S1], including escalating costs of food ingredients, labor, construction, and utilities which management has not fully offset through pricing or operational efficiency gains. The company’s fiscal second quarter report underscored these challenges—while revenue beat expectations slightly, operating losses persisted [N1]. This combination suggests top-line resilience tempered by margin compression driven by cost inflation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | 25 | -5 | 46 | +78.4% |

| 2024 | -9 | 16 | -12 | 44 | -686.2% |

| 2023 | 2 | 18 | 0 | 39 | +296.6% |

| 2022 | -1 | 24 | -1 | 27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | -0.8 |

| 2024 | -29 | -5.4 |

| 2023 | -21 | 0.9 |

| 2022 | -3 | -0.8 |

Source: SEC companyfacts cache [F1].

Note: Percentage changes calculated where data allows enabling clear trend observation.

Automated Dining as a Moat and Operational Driver

Kura Sushi’s defining differentiator lies in its proprietary automation technologies that extend well beyond traditional conveyor belt sushi concepts. The firm employs sophisticated automated kitchen robotics including sushi robots that prepare items consistently with precision timing; revolving conveyor belts coupled with express lanes facilitate seamless customer service throughput; Bikkura-Pon rewards machines incentivize repeat visits through gamification; and touch screen digital menus streamline ordering [S1]. This ecosystem fosters efficient labor utilization — a key competitive edge given labor market volatility — while enhancing guest experience through novelty.

However, these benefits are tempered by inherent operational risks contained within high-technology deployments: mechanical failures can disrupt service continuity causing delays or degraded customer satisfaction levels [S1]. Maintenance complexity raises unplanned capital expense risk should aging equipment require replacement faster than anticipated. Furthermore cybersecurity risks loom over integrated point-of-sale systems vital to supply chain management and payment processing [S1]. Managing these technological dependencies gracefully will be crucial for sustaining operational throughput and protecting the moat.

Supply Chain and Vendor Dependencies: Operational Risks and Strategic Implications

Kura Sushi’s reliance on specialized vendors for both food products and automated equipment introduces concentrated supplier risk exposures. The company’s relationship with its majority shareholder Kura Japan delivers advantages around intellectual property licensing and supply chain synergies; however any disruption or deterioration could compromise availability or cost structures [S1]. Additionally the dependency on limited third-party vendors for timely delivery of ingredients or functioning robotic parts means interruptions could lead directly to product shortages or menu limitations impacting same-store sales.

The SEC filings stress this vulnerability explicitly referencing risks tied to vendor performance failures translating into operational bottlenecks or elevated expenses [S1]. Given the custom nature of the automated kitchen robotics employed by Kura Sushi — including proprietary rice washers or vinegarmixing machinery — sourcing replacements or repairs swiftly presents an ongoing challenge intrinsic to capital intensity in foodservice technology.

Growth Catalysts and Geographic Concentration: Opportunities in California and Texas

Operationally concentrated within California and Texas retail centers — particularly shopping malls — Kura Sushi aims to exploit ‘foot traffic optimization’ by situating outlets alongside complementary retail tenants benefiting from ambient consumer flows [S1][N4]. This geographic choice confers accessibility advantages yet simultaneously amplifies macroeconomic sensitivity to regional economic shifts or localized events.

Recent analyst commentary reflects cautious optimism around underlying brand strength given positive consumer response trends signaled ahead of their Q2 earnings [N4]. Expansion plans focus on adding units within existing markets leveraging brand recognition augmented by digital marketing campaigns emphasizing social media engagement.

Nonetheless geographic concentration remains a double-edged sword exposing the company to state-specific regulatory changes or economic slowdowns that could disproportionately impact revenues compared to broader national diversification.

Capital Intensity and Cash Flow Trends: Evaluating Investment Demands

Kura Sushi’s technological edge imposes substantial capital expenditure demands evident from capex figures consistently exceeding $39 million annually since FY2023 rising to $46 million most recently—a more than 70% lift compared to FY2022 levels [F1]. These investments fund new store openings as well as maintenance/replacement cycles covering complex conveyor belts and robotic assets.

While operating cash flow exhibits healthy expansion reaching nearly $25 million in FY2025 [F1], these inflows fall short relative to capex needs producing significant negative free cash flow approximated at -$21 million last fiscal year when subtracting capex from CFO [F1]. Persistently negative free cash flow underscores challenges balancing aggressive growth ambitions with prudent liquidity stewardship common within capital-intensive foodservice technology niches.

This dynamic creates pressures on funding sources—either reinforcing dependence on Kura Japan support mechanisms or necessitating external debt/equity raises—factors worth monitoring as potential leverage implications arise.

Returns, Dividends, and Buybacks: What Capital Allocation Reveals About Strategy

Reflective of its profitability profile marked by net losses over the past two fiscal years coupled with negative returns on equity (approximate ROE of -0.8% in FY2025) [F1], Kura Sushi has not initiated dividend distributions nor engaged materially in share repurchases according to recent filings [F1][S2]. This allocation stance aligns with prevalent reinvestment priorities directed toward expanding restaurant count alongside continuous enhancements in automation technologies.

Preserving capital internally supports addressing operational risks linked to equipment reliability while navigating inflationary input cost pressures without overly constraining liquidity buffers—the reported $26.6 million cash & equivalents balance as of early calendar year lends some cushioning [F1]. Investors should view this measured capital deployment approach as indicative of strategic patience typical among emerging technology-driven chains still refining scale economics.

What To Watch: Future Milestones and Market Catalysts

Key upcoming events warrant attention from market participants assessing Kura Sushi’s trajectory including forthcoming quarterly earnings releases where incremental improvements might emerge reflecting better inflation mitigation strategies or efficiencies gained from tech upgrades [N2][N5][S3]. Additionally management discussions may clarify intentions around debt refinancing options or potential acceleration of new unit openings targeting unmet demand pockets within California/Texas concentrations.

Potential catalysts also encompass evolving digital marketing successes embedded within the Bikkura-Pon system enhancing customer loyalty—an area where subtle shifts could demonstrate improvements beyond raw financial metrics. Conversely unresolved cybersecurity failures or supplier disruptions represent persistent downside threats detailed extensively in SEC disclosures ([S1]).

Navigating these factors will define whether Kura Sushi can transform its innovative concept into sustainable profitability balanced against inherent operational challenges associated with capital-intensive automated dining models.

This analysis is intended solely for informational purposes based on data disclosed up to April 8th 2026; it does not constitute investment advice nor suggest any buy/sell decisions regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments