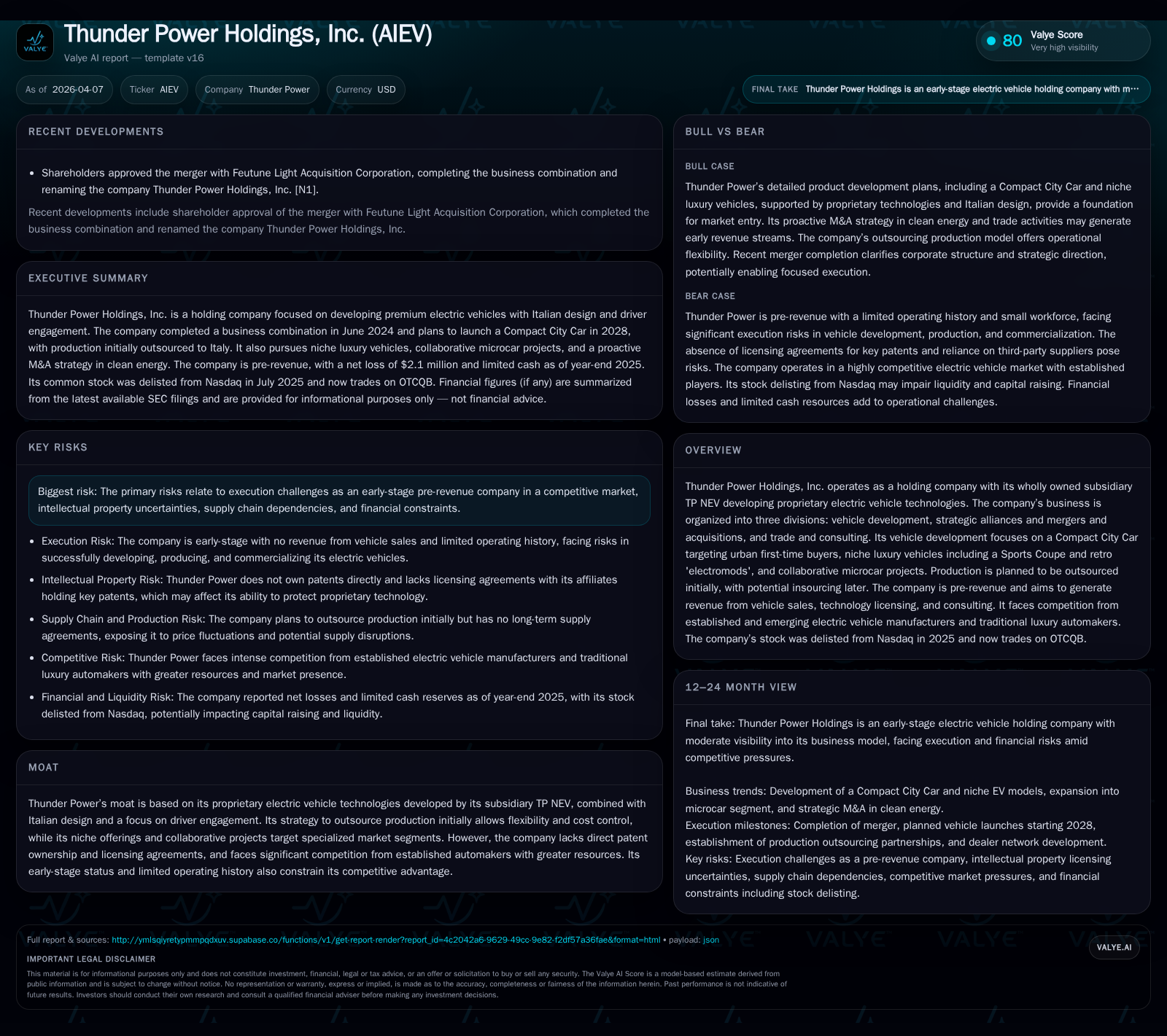

Thunder Power Holdings’ Financial Turbulence and EV Ambitions in 2025

Thunder Power navigates the intersection of early-stage electric vehicle innovation and financial strain amid unproven commercial operations.

Thunder Power Holdings is an emerging electric vehicle company focused on proprietary technology and niche market segments. The company remains pre-revenue and operates at increasing losses with liquidity constraints, while facing significant legal and regulatory challenges tied to its controlling shareholder. Outsourced production and modular vehicle design underpin its go-to-market approach, but competitive pressures from established players limit its moat. Key near-term developments include commercialization milestones, cash flow management, and legal risk resolution affecting investor confidence.

Historical Performance: Early Losses Reflect Development Phase

Thunder Power Holdings' recent financial results illustrate typical challenges faced by early-stage electric vehicle developers progressing from technology development toward commercialization. Operating income declined sharply from -$508K in fiscal year 2022 to approximately -$1.25 million in 2023, a year-over-year deterioration of about -145.8% per SEC filings [F1]. Net income also turned negative again after a brief positive period, reaching a loss of roughly -$2.12 million by fiscal year-end 2025. Operating cash flows have consistently been negative, closing fiscal 2025 at approximately -$1.51 million—down roughly 23.4% year-over-year—reflecting sustained investment without offsetting revenue generation [F1]. Equity fluctuated over the period but was positive at about $4.82 million at the end of 2025.

These figures depict a capital-intensive development stage characterized by ongoing expenditures on research, product development, and operational build-out without commercial sales contributions. Return on equity is approximately -44%, underscoring the absence of profitability during this phase [F1]. This financial profile aligns with expectations for nascent automotive technology ventures refining capabilities before scaling production.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -2 | -2 | +15.3% | |

| 2024 | -3 | -1 | -287.2% | |

| 2023 | 1 | -3 | -1249577 | +230.4% |

| 2022 | 0 | -1 | -508379 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -44.0 |

| 2024 | -38.4 |

| 2023 | -21.8 |

| 2022 | -14.5 |

Source: SEC companyfacts cache [F1].

Note: Operating incomes before 2024 are not available; YoY measurements shown where possible.

Proprietary Technology and Product Pipeline Overview

Thunder Power operates primarily through its wholly owned subsidiary Thunder Power New Energy Vehicle Development Company Limited (TP NEV), which has developed proprietary electric vehicle technologies forming the foundation for its planned model lineup [S1]. The company focuses on three core product categories: a Compact City Car targeting urban buyers; niche luxury vehicles such as Sports Coupes and "electromods"—electrified restomods appealing to enthusiasts seeking modern performance combined with vintage aesthetics; and collaborative microcar projects aimed at bridging motorcycles and passenger vehicles in growing urban mobility segments [S10][S19].

No models have yet reached commercial production or sales stages; Thunder Power remains pre-revenue. Its proprietary innovations include battery management systems and modular chassis frameworks designed to support future licensing opportunities alongside direct vehicle sales [S1]. The design is led by European stylists emphasizing driver engagement and brand identity.

Strategic Focus: Niche Urban, Luxury, and Collaborative EV Models

Thunder Power's strategy emphasizes differentiation through targeted niche segments rather than mass-market penetration. Initial production will be outsourced to Italian manufacturing partners to maintain capital efficiency while ensuring quality aligned with premium positioning; insourcing options are planned around 2030 to enable scale economies [S10][S19].

Key aspects include:

- Compact City Car combining affordability with Italian design tailored for urban environments.

- Luxury Sports Coupe using modular platforms for grand touring attributes.

- Electromod projects converting classic vehicles to electric powertrains tapping into sustainable retrofitting trends.

- Microcar collaborations targeting an addressable market projected by McKinsey to reach $340 billion annually by 2030 in Europe and Asia [S10].

Strategic alliances involve platform sharing with original equipment manufacturers for exclusive markets to expand footprint without heavy internal manufacturing investment.

Regulatory and Legal Risks Impacting Growth Prospects

Legal challenges linked to controlling shareholder Wellen Sham create reputational risks and possible leadership distractions. Mr. Sham faces criminal prosecution in Taiwan related to securities indictments involving alleged related-party transactions and misleading disclosures valued in multimillions USD; concurrent civil claims seek damages and removal from affiliated boards [S5][S24].

While these proceedings do not currently implicate Thunder Power directly in legal or financial terms, they introduce uncertainty that could affect partner confidence or access to capital markets given the company’s OTCQB listing status following Nasdaq delisting in 2025 [S3][S5].

Additionally, compliance with evolving international regulations—including EU GDPR data privacy rules, US safety certifications requirements, environmental laws—and cybersecurity mandates adds operational complexity requiring ongoing management focus [S6][S7][S21].

Capital Allocation: Liquidity Position and Cash Flow Challenges

As of fiscal year-end 2025, Thunder Power held current assets of approximately $13.15 million against current liabilities of about $8.36 million yielding a current ratio near 1.57—a moderate liquidity cushion. However, cash reserves were just under $1 million as of mid-2024 amid rising operating cash flow deficits exceeding $1.5 million annually due to sustained R&D spending without commercial revenues [F1][S10].

Negative free cash flow trends paired with recurring net losses underscore reliance on external financing absent significant revenue or cost reduction measures. The company neither pays dividends nor conducts share buybacks consistent with its early-stage reinvestment focus [F1].

Growth Outlook and Commercialization Milestones

Thunder Power targets initial commercial production through outsourced manufacturing hubs beginning circa 2028 with its Compact City Car launch followed by luxury models alongside low-volume joint venture microcars expected from 2027 onward pending market pricing validation [S10]. Full independent microcar models may follow post-2030 conditions permitting.

No explicit revenue guidance or volume forecasts are disclosed; progress monitoring should focus on prototype completions, technology validations such as battery performance benchmarks or regulatory certification achievements [S1]. Outcomes of strategic alliances including licensing or collaboration agreements will also be key indicators of revenue diversification prospects beyond direct vehicle sales.

Competitive Environment and Moat Considerations

Despite proprietary technologies developed via TP NEV combined with Italian design influence enhancing brand appeal, Thunder Power's competitive moat is limited due largely to lack of enforceable patents protecting core innovations versus well-capitalized incumbents like Tesla or BYD who possess extensive intellectual property portfolios plus established supply chains and large-scale manufacturing capacities [S14].

The company faces technology licensing risks stemming from this IP gap plus scale disadvantages common among emerging entrants but seeks leverage through strategic partnerships enabling rapid market entry without legacy overheads.

Consequently brand differentiation through design excellence must complement technical uniqueness for sustainable competitive positioning within crowded premium urban mobility niches.

Governance Issues Affecting Investor Confidence

Ongoing litigation involving Mr. Wellen Sham undermines leadership stability amid public scrutiny over multiple securities-related charges linked indirectly to Thunder Power’s corporate structure [S3][S5][S24]. This environment may distract management from executing complex automotive scaling initiatives.

Trading on OTCQB after Nasdaq delisting limits market liquidity potentially depressing valuation sentiment which could raise capital costs or restrict access if reputational fallout extends.

Smaller public companies facing executive legal challenges often navigate difficult communications balancing transparency with legal constraints—a governance challenge relevant here.

This analysis is based exclusively on audited SEC filings up through April 7th, 2026 supplemented by official company disclosures reflecting verified financial data without speculative extrapolation.[F1] It aims solely to provide an informed perspective on Thunder Power Holdings' evolving operational landscape shaped by financial metrics and strategic context.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments