Ooma Inc’s Revenue Rebound and Strategic Growth Imperatives

The company achieved a pivotal shift to profitability in fiscal 2026, propelled by user base expansion, strategic acquisitions, and disciplined capital deployment amid rising operational costs.

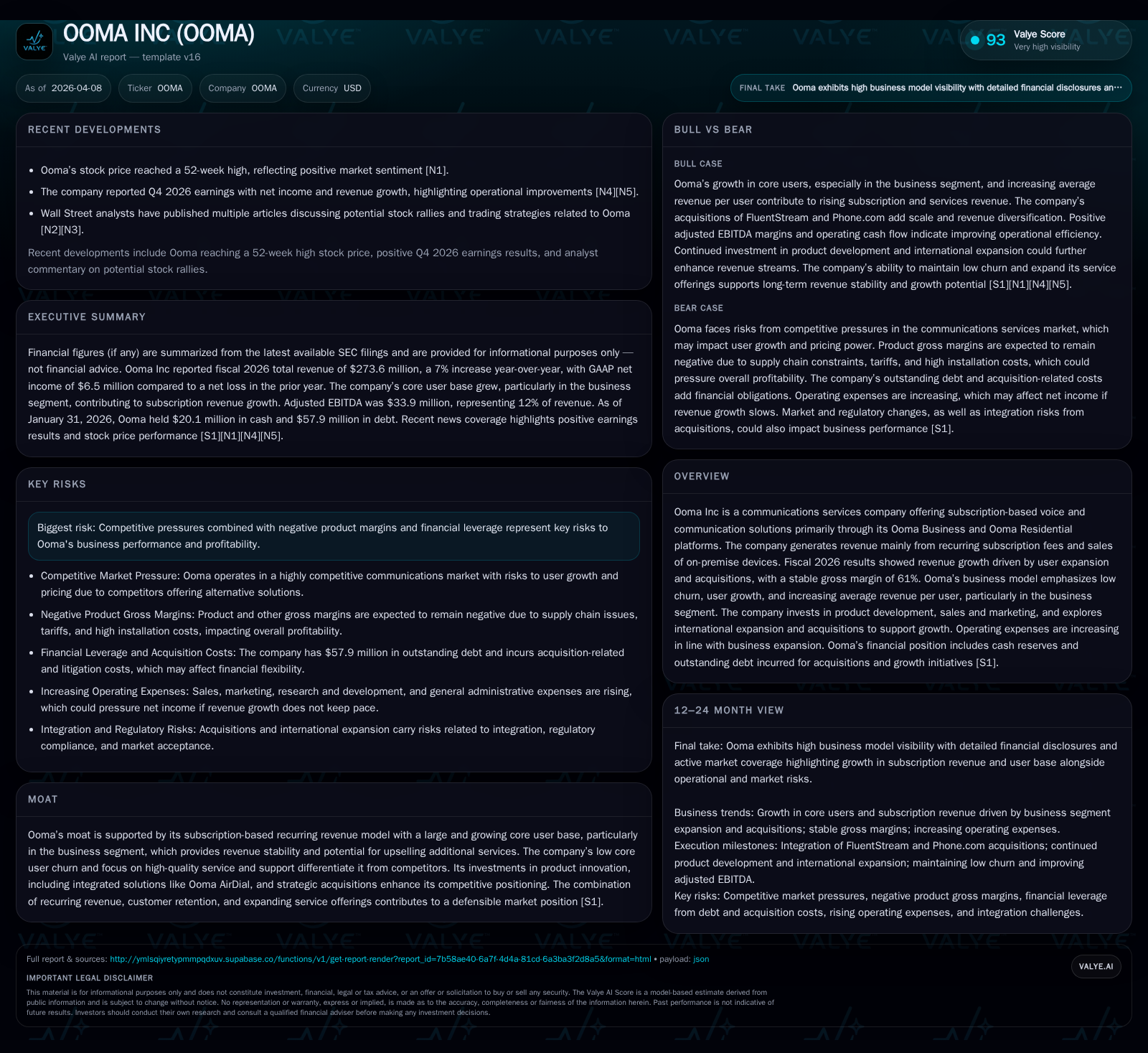

Ooma Inc reversed a multi-year net loss streak in fiscal 2026, reporting $273.6 million in revenue and $6.5 million net income, supported by strong organic growth and acquisitions. The subscription-based model with low churn fosters stable recurring revenues, while recent purchases of FluentStream and Phone.com drive incremental top line but pressure margins short-term. Management focuses on innovation, international expansion, and leveraging integrated solutions such as Ooma AirDial to sustain momentum. Financial discipline is evident in robust operating cash flow and sizable buybacks, balanced against leverage from new debt taken on to fund acquisitions.

Transformation From Losses to Profitability: A Historical Snapshot

Ooma Inc’s trajectory from sustained losses toward profitability is a defining narrative of its recent financial evolution. In fiscal year 2026 (ending January 31), the company generated $273.6 million in revenue, marking a healthy 7% increase year-over-year [S1][F1]. This top-line improvement contrasts sharply with prior years characterized by flat or subdued growth; for example, FY2023 revenue was significantly lower with the business still absorbing structural costs.

A more striking development lies in profitability metrics: after posting a net loss of $6.9 million in FY2025, Ooma recorded a net income of $6.5 million in FY2026 [F1]. The swing reflects not only higher revenues but also operating income recovery—the operating profit jumped from negative $6.9 million to positive $4.3 million over the same period [F1]. Adjusted EBITDA corroborates this turnaround, reaching $33.9 million (12% of revenue) compared to $23.3 million in fiscal 2025 [S1].

Cash flow generation supports these gains; operating cash flow stood resilient at $27.7 million in FY2026 versus $26.6 million the preceding year [F1]. Capital spending moderated slightly with capex down approximately 13% year-over-year to $5.6 million [F1], indicating disciplined investment aligned with scaling operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 6 | 28 | 4 | 6 | +193.6% |

| 2025 | -7 | 27 | -7 | 6 | -726.5% |

| 2024 | -1 | 12 | -4 | 6 | +77.2% |

| 2023 | -4 | 9 | -6 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 12 | 22 | 7.0 |

| 2025 | 4 | 20 | -8.1 |

| 2024 | 6 | -1.1 | |

| 2023 | 4 | -5.8 |

Source: SEC companyfacts cache [F1].

*FY2025 revenue approximated based on YoY given; actual figure not directly stated.[F1] Note: Revenue for FY2024 and earlier omitted due to incomplete series for this table.

This financial turnaround underscores effective cost management alongside top-line momentum.

Driving Forces Behind FY2026 Revenue Growth

Ooma’s reported revenue growth of roughly 7–9% for fiscal 2026 stems primarily from two vectors: organic subscriber expansion within its business segment and incremental revenues from acquisitions finalized late in calendar year 2025 [S1][N2][F1]. Specifically, the Ooma Business subscription services segment alone saw approximately a 10% year-over-year increase fueled by growing user counts [S1].

More than just volume gains, this organic growth signals enhanced market penetration among small and medium-sized enterprises (SMEs), where unified communications solutions continue supplanting legacy telephony systems — a trend Ooma seeks to capitalize on by expanding feature sets tailored for such customers.

Acquisition-driven revenues contributed an additional estimated $6.1 million during fiscal 2026 attributable mainly to FluentStream and Phone.com acquired in December 2025 [S1][N3]. While these bolt-ons extended market reach and service capabilities, they introduced integration complexities (explored later) that put transient pressure on margins.

Crucially, Ooma maintains gross margins steady around the mid-60s percentage mark—61% reported for both fiscal years 2025 and 2026—despite an uptick in device sales which inherently carry slimmer margins relative to subscription services [S1]. This stability reinforces the robustness of core subscription offerings even as hardware components supplement revenues.

Subscription Model Strength: Core User Expansion and Low Churn Dynamics

At Ooma’s core lies its subscription-based recurring revenue structure underpinning its financial steadiness—the so-called “moat” of business stability [S1]. Management emphasizes two intertwined pillars here: sustained growth in core users coupled with impressively low turnover rates (churn).

Core user growth acts as a reliable barometer of expanding market footprint; increased penetration translates into higher Monthly Recurring Revenue (MRR), driving overall revenue resilience even amidst competitive pressures.

Low churn rates—particularly notable within Ooma Business subscribers—stem from customer satisfaction backed by robust service quality and comprehensive support models designed specifically for telephony SaaS clients who value uptime and feature reliability [S1]. In communications SaaS parlance, customer lifetime value (LTV) becomes maximized when retention remains high alongside gradual upselling of additional functionalities or service tiers.

Average Revenue Per User (ARPU), another critical KPI within telecom SaaS metrics, reflects successful engagement strategies that promote adoption of premium voice solutions such as integrated call routing via Ooma AirDial platforms [S1]. Having multiple touchpoints increases switching costs for clients, consolidating revenue streams.

Thus, the consistent ebb of core subscriber addition jointly with limited attrition safeguards the recurring revenue base—a crucial counterbalance amid volatile device sale performance or acquisition-related flux.

Acquisition Contributions and Integration Challenges

FluentStream and Phone.com acquisitions clearly bolster Ooma’s top line but present short-term integration challenges impacting cost structure and profits [S1][N3]. These transactions generated approximately $6.1 million incremental revenues yet incurred around $1.6 million in acquisition-related expenses during fiscal year end [S1]. Additionally, litigation costs tied partially to these deals reached about $1.5 million.

During integration phases common in telecom services consolidations, overlapping functions require harmonization; migrating customers onto unified platforms while aligning product roadmaps can induce temporary operating inefficiencies or elevate personnel expenses.

Such transitional dynamics may contribute to observed negative product margin trends noted as part of risk disclosures—the mismatched cost absorption potentially dilutes expected immediate margin accretion from acquired entities [S1]. The trade-off involves sacrificing near-term profitability impacts to secure broader market access or cross-selling potential ultimately enhancing downstream economics.

This balance between acquisition-fueled scale versus cost absorption pressures represents a strategic imperative requiring vigilant execution excellence moving forward.

Future Growth Trajectory: Product Innovation and Market Penetration

Looking ahead, management underscores continued commitment toward expanding product offerings centered around innovation like the Ooma AirDial integrated platform aimed at replacing legacy analog phone infrastructure for businesses [S1][N2]. This product development aligns closely with broader industry shifts favoring cloud-native voice communications bundled with analytics capabilities.

International expansion efforts are also highlighted as avenues for unlocked addressable markets beyond North America—a typical evolution vector for telecom SaaS providers seeking diversified geographic footprints promoting long-term revenue durability [S1].

Concomitant investments facilitate feature enrichment within the Ooma Business segment focusing on scalability for varying enterprise sizes inclusive of advanced administrative controls and cybersecurity enhancements—features increasingly demanded by SME clientele amid heightened risk awareness.

However, it is prudent to recognize timing uncertainties associated with product rollout effectiveness or international market adoption; inherent execution risks could modulate expected growth pace.

Financial Forecasts and Analyst Sentiment

While explicit company guidance focusing on precise fiscal benchmarks remains circumspect within filings [S1], Wall Street analysts have voiced optimism—some projecting upside rallies ranging approximately from +26% up to +34% over short-term horizons based on anticipated continued earnings momentum and subscriber gains [N4][N5].

These viewpoints emphasize monitoring upcoming quarterly releases closely for sustained user growth rates and margin trajectory clarity—the chief determinants clueing into durable profit improvement vs transitory fluctuations.

Absent firm guidance figures necessitates viewing analyst sentiment as directional rather than prescriptive for valuation cues.

Capital Allocation Priorities: Balancing Buybacks, Investments, and Debt

Ooma demonstrates judicious capital deployment balancing shareholder returns against reinvestment needs amid transformation progressions [F1][S1]. Operating cash flow generation is solid at nearly $28 million annually commensurate with ongoing expansion pressures while capital expenditures taper modestly signaling efficient capex utilization compared with historical outlays.

Noteworthy is share repurchase activity accelerating materially—to about $11.6 million in FY2026 from under half that level previously—which signals confidence in intrinsic valuation amidst profitable turnaround execution [F1]. Meanwhile, the company manages increased leverage strategically—$57.9 million of outstanding debt recorded post-acquisition contrasted against zero debt the prior year—reflective of financing growth initiatives but imposing covenant considerations affecting flexibility [S1][F1].

Return on equity approximates a moderate ~7%, reflecting nascent profitability recovery tempered by equity base expansion coincident with cash accumulation endeavors [F1]. This metric suggests room remains for further capital efficiency improvements as operating leverage deepens alongside expanded scale.

Key Risks: Competitive Pressures, Margin Assumptions, and Operational Leverage

Ooma identifies several material risks pertinent across communications SaaS sectors that could affect its trajectory adversely if unmitigated [S1]:

- Customer acquisition costs must remain controlled lest they dilute margin gains; competition among voice communication vendors intensifies pricing pressure,

- Negative product margins signal vulnerability linked largely to third-party hardware sourcing dependencies introducing supply chain reliability concerns,

- Tariff volatility or trade policy changes threaten cost structures given device imports,

- Operational expense elasticity accompanying scaling introduces financial leverage risk where rising fixed costs challenge sustainable profit margins,

- Service interruptions—including ransomware or cyberattacks—pose reputational hazards directly impacting customer retention,

- Acquisitions entail integration risks including unanticipated expenses or dilution impacts potentially offsetting projected synergies;

- Reliance on resellers/distributors demands attentive channel management lest distribution bottlenecks impair sales execution.

The compounded effect mandates rigorous management oversight particularly regarding customer churn prevention strategies emphasizing network uptime guarantees plus cybersecurity measures essential within hosted telephony infrastructure environments.

Disclaimer: This analysis relies exclusively on publicly available filings ([F1][S#]) and verified news sources ([N#]). It does not constitute investment advice or recommendations but aims solely to inform internal discussions through factual synthesis of recent corporate developments concerning Ooma Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments