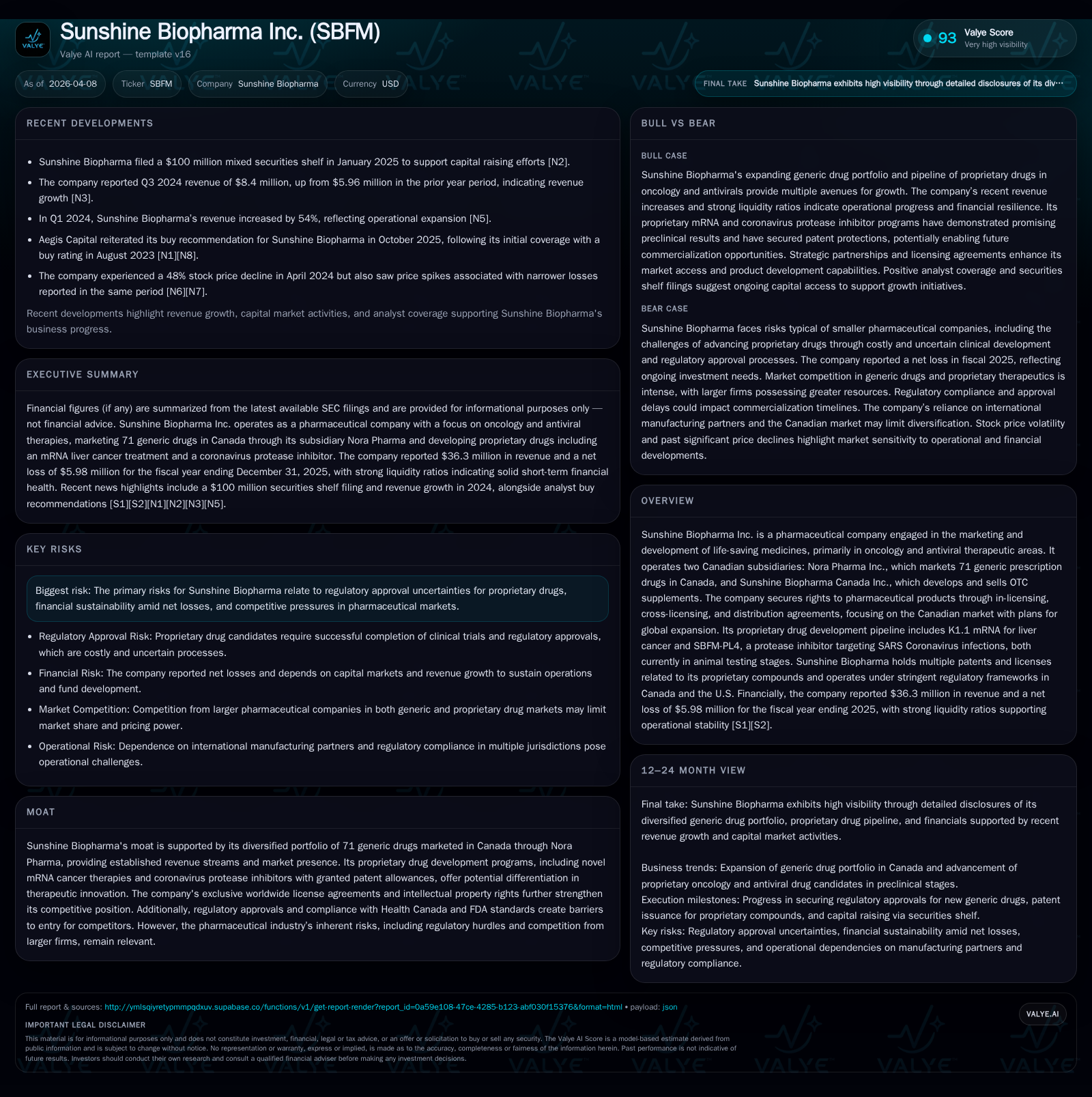

Sunshine Biopharma’s Struggle to Balance Generic Sales and Proprietary Drug Development in 2025

The company’s 2025 financials reveal modest revenue growth from generics against persistent net losses, while its pipeline advances remain early-stage and capital-intensive.

Sunshine Biopharma Inc. leverages its Canadian subsidiary Nora Pharma’s portfolio of 71 generic drugs to generate steady revenue, marking a clear progress trajectory since its 2022 acquisition. However, despite a 4.1% year-over-year revenue increase to $36.3 million in 2025, the company continues to report significant net losses, driven by operational costs and extensive investments in proprietary drug development programs targeting oncology and antiviral therapies. Its cash flow remains negative with free cash flow close to -$5.5 million in 2025, underscoring ongoing funding challenges as it navigates regulatory complexities and competitive pressures within the generic pharmaceuticals market and beyond.

Historical Growth and Financial Performance

Sunshine Biopharma's growth since acquiring Nora Pharma in October 2022 illustrates a clear ramp-up in revenues driven predominantly by generic pharmaceutical sales in Canada. Annual revenues surged from approximately $4.3 million in fiscal year (FY) 2022 to $36.3 million by FY 2025 — representing nearly a ninefold increase over three years [F1]. This growth stems from actively expanding the portfolio to include 71 generic prescription drugs across various therapeutic categories.

Despite this top-line momentum, profitability remains elusive. The company recorded net losses each fiscal year since at least FY 2022, albeit with incremental improvement: a loss of about $26.7 million in FY 2022 narrowed to roughly $6 million by FY 2025 [F1]. Operating income follows a similar pattern with negative results each year and an operating loss of approximately $6.2 million in FY 2025, indicating ongoing operational cost burdens linked to commercial activities and R&D investment [F1].

Operating cash flows have been negative throughout this period but showed marked progress improving from nearly -$12.5 million in FY 2024 to -$5.3 million in FY 2025 [F1]. Capital expenditures declined steeply in FY 2025 relative to prior years, reflecting perhaps a more cautious investment approach amidst cash constraints [F1]. Equity remained relatively stable around the $23 million mark through these years.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 36 | -6 | -5 | -6 | +4.1% | -16.4% |

| 2024 | 35 | -5 | -13 | -6 | +44.7% | -13.9% |

| 2023 | 24 | -5 | -9 | -5 | +454.4% | +83.2% |

| 2022 | 4 | -27 | -5 | -27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -6 | -25.9 |

| 2024 | 3 | -14 | -21.8 |

| 2023 | -9 | -21.2 | |

| 2022 | -5 | -123.7 |

Source: SEC companyfacts cache [F1].

Note: All figures are USD; "Rev" indicates revenue; "OpInc" operating income; "Net" net income; "CFO" operating cash flow; "Capex" capital expenditure; YoY denotes year-over-year growth

Drivers Behind Historical Performance

The central catalyst behind Sunshine Biopharma's past revenue gains is Nora Pharma's growing footprint within the Canadian generic drug market. Nora Pharma's strategy involves acquiring rights via in-licensing agreements or cross-licensing arrangements to market approved generics under its label after Health Canada's regulatory approvals [S1]. The company's ability to scale offerings moderately smooths revenue volatility inherent to generics amid drug price erosion pressures.

However negative margins underline intrinsic challenges faced by generic pharma companies: pricing competitiveness leads to thin profit margins while supply chain vulnerabilities — exacerbated by global macroeconomic instability post-pandemic and geopolitical conflicts — threaten consistent product availability [S1]. Nearly all generics marketed by Nora Pharma are made outside North America which subjects supply chains to risks tied to tariffs or sanctions.

Further constraining profitability are local reimbursement policies governed federally and provincially which control prices payable for drugs— tightening those parameters threatens revenue stability [S1]. Launch delays due to regulatory hurdles could also blunt short-term sales growth prospects.

Proprietary Drug Pipeline and Future Growth Potential

Beyond generics sales stability efforts focus heavily on a proprietary pipeline addressing critical unmet needs primarily in oncology and infectious disease therapeutics:

- K1.1 mRNA: An encapsulated lipid nanoparticle (LNP) mRNA therapy targeting liver cancer currently undergoing animal testing.

- SBFM-PL4: A protease inhibitor aimed at combating SARS coronavirus infections also in preclinical evaluation stages [S1].

These projects benefit from granted patent allowances conferring protective intellectual property rights globally which could eventually anchor differentiated high-margin products if clinical development advances successfully [S1].

Nonetheless the programs remain early stage without near-term clinical trial data or regulatory milestones publicly disclosed—increasing uncertainty around timelines for potential commercialization or return on R&D investment [S1]. Rigorous regulatory frameworks under Health Canada (and planned FDA compliance) impose long lead times adding complexity and risk.

Financial Expectations and Monitoring Points

Sunshine Biopharma has not publicly issued formal revenue or earnings guidance for upcoming periods within SEC filings [S1][S2], complicating precise forecasting.

For investors and analysts monitoring this company’s trajectory key indicators should include:

- Quarterly performance of Nora Pharma’s generics portfolio sales volume amidst supply chain conditions,

- Progress updates on preclinical and eventual clinical trial milestones for proprietary compounds,

- Regulatory approvals or delays announcements related to new generic launches,

- Cash flow evolution given existing net losses combined with capital expenditure demands,

- Any changes or expansions in licensing agreements signaling geographic or product diversification initiatives.

Absent explicit forecasts these proxy signals are vital data points for assessing whether commercial operations can sustain growth momentum while balancing investment into innovative drug candidates.

Capital Allocation and Returns Analysis

The company’s capital allocation profile reveals no dividends paid historically nor share repurchases during FY 2025 following a modest ~$3.1 million buyback initiative implemented in FY 2024 [F1]. Preserving cash amid significant net losses appears prudent for funding ongoing operational costs and pipeline R&D.

Return metrics exemplify typical early-stage biopharmaceutical development profiles where losses overshadow equity; Sunshine Biopharma’s approximate ROE calculated at around -25.9% reflects continued negative earnings relative to book value [F1]. Free cash flow remains negative near -$5.5 million driven largely by sustained operating outflows exceeding reduced capital spending [F1].

Liquidity appears sufficient given current assets considerably surpass current liabilities with a strong ratio above four times providing buffer but necessitates ongoing external financing consideration if current loss trends persist [F1].

Regulatory Environment and Industry Risks

As per filings from April 2026 [S1], Sunshine Biopharma operates within stringent regulatory confines: Health Canada approval processes take on average about one year for newly licensed generic dossiers whereas cross-licensed products achieve faster approval within approximately two months post submission.

These timelines impose execution risks especially when trying to maintain product launches that offset price erosion effects prevalent across generics sectors [S1]. Furthermore macroeconomic instability—resulting from known global conflicts—and resultant supply disruptions represent added operational hazards affecting manufacturing sourced predominantly overseas [S1].

Pricing pressures tied to national reimbursement schemes introduce further uncertainty about sustainable profit margins.

Legal Proceedings Summary

A legal dispute involving a former legal counsel alleging wrongful termination was resolved decisively with Sunshine Biopharma prevailing as of March 2026 [S1]. This outcome minimizes contingent liabilities or financial distractions emanating from the matter going forward.

Conclusion

Sunshine Biopharma walks a delicate path between leveraging an established portfolio of generics generating steady albeit low-margin revenues against ambitious proprietary drug development efforts that carry typical biotech risks related to lengthy clinical paths and uncertain returns. Recent annual financials show clear revenue scaling but persistent losses highlight continuing challenges covering operational costs without significant bottom-line improvement yet.

Success hinges on managing complex supply chains amid volatile global conditions while advancing novel therapeutic candidates through preclinical phases toward clinical trials—without clear near-term milestones publicized—making future growth outcomes subject to considerable unpredictability.

Stakeholders should continue watching commercial execution efficacy at Nora Pharma combined with scientific progress reports from the specialized drug pipeline alongside liquidity management as primary barometers shaping longer-term viability.

This analysis is provided solely for informational purposes based on publicly available data through April 8th, 2026 including SEC filings and company disclosures. It does not constitute investment advice or recommendations regarding securities of Sunshine Biopharma Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments