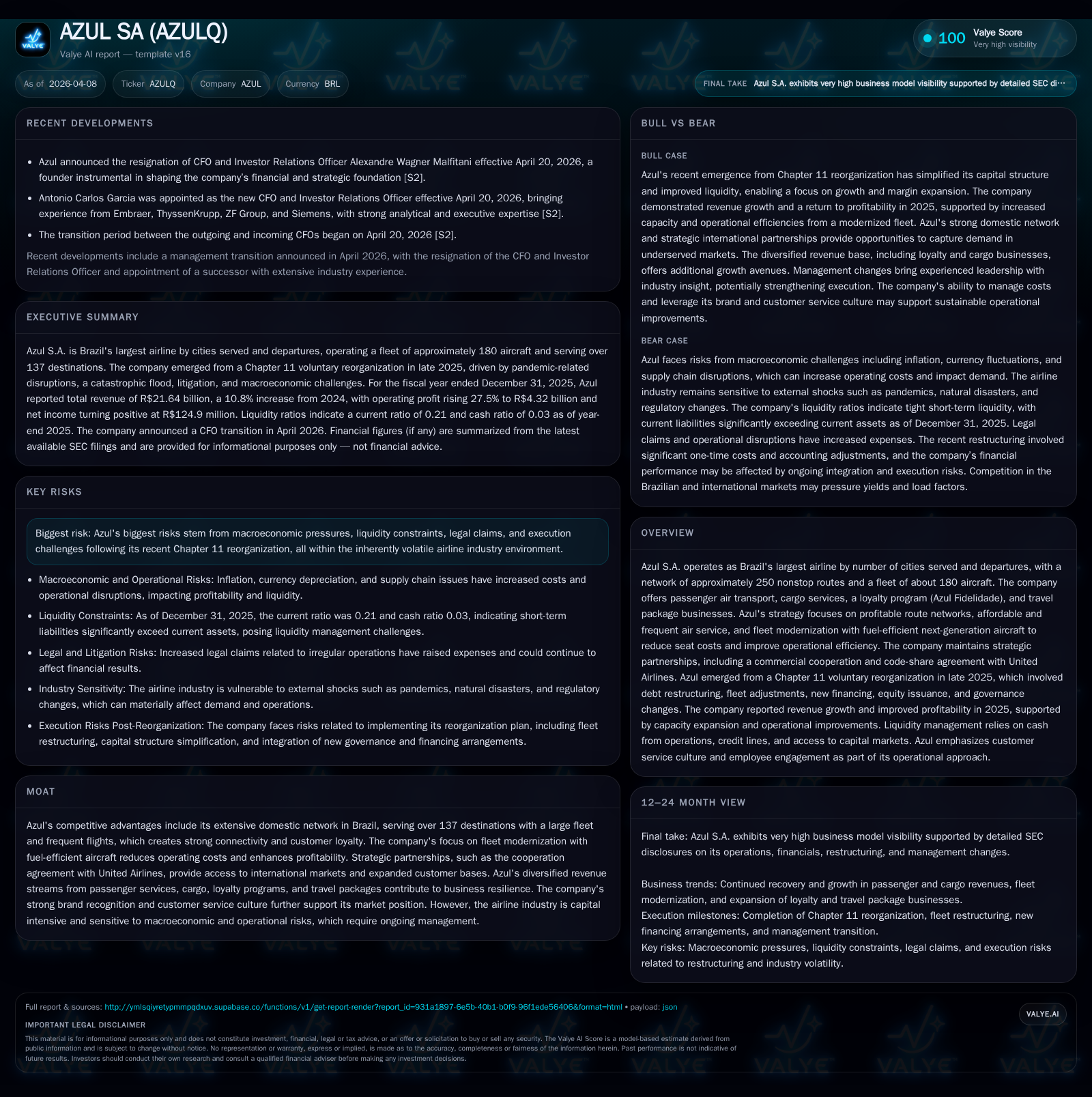

Azul SA's Rebound and Restructuring: Brazil’s Leading Airline Charts a New Course

Azul SA emerged from Chapter 11 in late 2025, undertaking significant capital and operational restructuring to position itself for sustainable growth in Brazil’s aviation sector.

The airline experienced a notable financial turnaround in 2025, transitioning from steep losses to modest profitability driven by revenue growth and operational improvements. Its Chapter 11 exit entailed deleveraging through debt equitization, new equity injections, fleet rationalization, and fresh financing facilities, all underpinning a leaner capital structure. Operationally, Azul enhanced its domestic network breadth and punctuality while embracing fuel-efficient aircraft to reduce unit costs. Leadership changes, including the appointment of a new CFO with deep aerospace finance experience, signal strategic continuity and strengthened financial stewardship. Going forward, growth prospects remain anchored in network expansion and diversified revenue streams but face macroeconomic headwinds and execution risks inherent to the industry.

From Distress to Recovery: Azul’s Financial Turnaround in 2025

Azul SA delivered a striking financial recovery in the year ended December 31, 2025. After several years plagued by heavy losses—including net income deficits of over BRL -9 billion in 2024—the company swung into positive territory with a modest net profit of approximately BRL 125 million [F1]. This turnaround was fueled chiefly by a strong revenue uptick of roughly 10.8%, lifting the top line to BRL 21.6 billion from BRL 19.5 billion in the prior year [F1]. Operationally, passenger traffic expanded robustly; Revenue Passenger Kilometers (RPKs) climbed about 12% while Available Seat Kilometers (ASK) capacity grew by roughly 10%, reflecting tightly managed capacity responses amid recovering demand domestically [S1].

This progress unfolded despite headwinds including currency depreciation of about 3.5% against the US dollar and elevated fuel prices averaging $65 per barrel WTI—an environment that historically pressures airline margins. Yet Azul managed margin improvement partly via disciplined pricing strategies and leveraging its extensive Brazilian route network which serves around 160 destinations as of year-end [S1]. Improving service quality led to enhanced punctuality standings worldwide: from #10 in global rankings in prior years to reaching #4 according to Cirium data, bolstering customer satisfaction metrics essential for retention and competitive differentiation within Brazil’s dense domestic market [S1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 21.6 | 0.1 | +10.8% | +101.4% |

| 2024 | 19.5 | -9.2 | +5.2% | -284.4% |

| 2023 | 18.6 | -2.4 | +16.3% | -229.5% |

| 2022 | 15.9 | -0.7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -0.4 |

| 2024 | 30.1 |

| 2023 | 11.2 |

| 2022 | 3.8 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow for FY25 reflects negative outcome partly due to restructuring cash effects [S6]; capex decline signifies scaled-back aircraft investment aligned with fleet restructuring.

The Imprint of Chapter 11: Restructuring Impact on Capital and Fleet

Azul’s voluntary reorganization under Chapter 11 marked a transformative juncture concluded late 2025 after protracted negotiation with creditors and stakeholders. The confirmed Plan centered on equitizing substantially all unsecured funded indebtedness—including exchange offers converting existing notes into common shares—thus deleveraging the balance sheet materially [S1]. Concurrently an Equity Rights Offering garnered fresh capital with contributions from key strategic investors including United Airlines and secondary investors through American Warrants mechanisms providing latent liquidity underpinning.

Complementing these financial maneuvers were operational initiatives: fleet optimization streamlined through rejecting onerous operating leases and restructuring aircraft commitments—a move designed to reduce fixed cost burdens amid uncertain demand recurrences post-pandemic —balanced against securing new exit financing facilities replacing interim DIP financing with longer maturities at improved terms [S1]. Governance changes introduced a more consolidated board structure aimed at agile decision-making necessary for swift execution.

The accounting treatment of the reorganization featured significant one-time gains/losses arising from derecognition of retired liabilities coupled with valuation impacts from equity issuances altering reported equity into negative territory approximating BRL -29 billion at FY end despite improving operations—a symptom typical where legacy accumulated losses dwarf recent earnings improvements following complex restructurings [F1].

Analyzing Revenue Growth Drivers and Market Position Expansion

Azul leveraged its competitive interplay within Brazil’s fragmented domestic market characterized by varying economic conditions—including inflationary pressures (~4.26% IPCA inflation in Brazil during ’25)—to grow passenger revenues supported by expanding route density across more than 160 cities served as of end-2025 [S1]. The carrier’s breadth remains unparalleled nationally offering ~250 nonstop routes enabling strong connectivity especially across underserved regional segments.

Additionally contributing were beyond-core passenger revenues: cargo logistics operated under Azul Cargo showed double-digit growth feeding diversification alongside loyalty program gains via Azul Fidelidade which continues engaging customers with enhanced redemption opportunities integrated into travel packages run by Azul Viagens [S1]. These units bolster resilience against cyclicality inherent in pure passenger travel revenues.

Despite challenging macroeconomics – Brazilian real depreciation against USD averaging about 3.5%—Azul demonstrated resilience attuned through disciplined pricing allowing partial surcharge pass-through without impairing volumes materially given firm leisure/business travel demand recovery witnessed post-pandemic rebound [S1].

Operational Excellence: Punctuality, Route Network, and Fleet Modernization

Operationally Azul made strides beyond scale enhancing service quality crispness evidenced by improving punctuality rankings globally climbing from tenth position earlier to fourth according to independent analytics firm Cirium—a critical metric influencing customer preference within price-sensitive markets such as Brazil’s commercial aviation sphere [S1].

Moreover commandeering operational efficiency stemmed largely from accelerated adoption of next-generation aircraft featuring superior fuel burn metrics—reducing seat costs appreciably while elevating environmental compliance fostering long-term sustainability advantages amid sector-wide green scrutiny pressures [S16]. Their fleet averaged only about seven years old excluding small Cessna Caravans compared favorable to peers whose aging assets manifest higher maintenance expenses escalating operational risk profiles.

Crucially half-plus of maintenance exposure rests on power-by-the-hour contracts offering predictable servicing cash flows cushioning volatility particularly against fluctuating flight hours induced by demand shocks or regulatory interruptions—a best practice increasingly adopted among leading carriers globally for cost certainty management [S16].

Alongside human capital investments driving punctuality are system integrations utilizing sophisticated booking platforms powered by Oracle and Sabre licenses enabling optimized yield management supporting revenue maximization per ASK unit flown aiding margin recovery objectives [S16].

Leadership Transition Amid Growth: New CFO Appointment Influence

April 2026 ushered a pivotal executive change when co-founder Alex Malfitani resigned as CFO after architecting much of Azul’s foundational financial strategy since inception—his tenure marked by landmark initiatives including IPO preparation and guiding restructuring processes culminating recently under Chapter11 proceedings [N2]. Malfitani's departure signals potential evolution towards refreshed financial steering aligned to post-restructuring growth phase.

His successor Antonio Carlos Garcia arrives equipped with substantive industrial finance credentials honed at Embraer—the world-renowned Brazilian aerospace manufacturer—where he helmed investor relations and finance at executive levels supporting complex asset acquisition cycles paralleling Azul’s fleet capital requirements and financing complexities [N2]. Garcia’s prior tenure at ThyssenKrupp managing global finance further underscores his capability handling multinational strategic complexities crucial for advancing Azul’s ambitions within volatile macroeconomic settings.

Under Garcia's leadership expect refinement of capital allocation frameworks emphasizing liquidity preservation while ramping investments selectively congruent with sustainable growth imperatives shaped by his analytical rigor gained through Harvard Business School Executive Program also noted for corporate governance focus enhancing investor communication modalities elevating market confidence levels.

Future Outlook: Growth Prospects and Potential Constraints

Looking ahead Azul projects continued expansion grounded in robust Brazilian leisure/business travel resurgence complemented by scaling loyalty program monetization initiatives plus aggressive penetration into cargo logistics fulfilling e-commerce-driven freight needs domestically [S1]. Capacity expansion planned aligns conservatively with macroeconomic tailwinds moderating consumer spending power insofar influenced by inflation trends hovering above central bank targets plus intermittent political uncertainties impacting business confidence broadly within Brazil.

Fuel price fluctuations remain a critical sensitivity given indexing embedded in operating costs although hedging policies currently cover limited ~7-8% of anticipated consumption requiring vigilant risk management adaptation should price spikes occur unexpectedly reducing margin cushions presently scaffolded by operational efficiencies achieved recently [S17]. Currency volatility may challenge import-dependent maintenance inputs hence currency risk mitigation instruments might be amplified beyond current scope.

OEM supply chain bottlenecks could delay aircraft deliveries constraining newer model induction while simultaneously affecting parts availability potentially inflating short-term maintenance outlays which could weigh on near-term operating leverage unless offset through dynamic scheduling adjustments implementing higher utilization regimes compatible with crew duty cycle regulations intrinsic within the sector.

Capital Allocation Strategy: Debt Profile, Dividends, and Shareholder Returns

Post-restructuring Azul exhibits a markedly reshaped balance sheet characterized by substantial equity infusion juxtaposed against decreased overall indebtedness though still harboring large nominal debt obligations denominated chiefly in US dollars totaling upwards of BRL ~23 billion involving aircraft leasing liabilities among principal constituents [F1]. Despite this scale leverage persists materially due principally to historic accumulated losses rendering equity negative near BRL -29 billion which distorts traditional ROE evaluation metrics ([F1]).

Cash balances approached BRL 992 million at year-end furnishing essential liquidity yet current liabilities exceeding current assets resulted in constrained current ratio (0.21), cautioning tight working capital governance imperative amid uneven collections related primarily to installment credit sales prevalent regionally within retail sectors including aviation ticketing structured largely via multi-month credit card platforms guaranteeing bank advances diminishing counterparty credit risk effectively . Management opted against dividend payouts reflecting prudent cash conservation stance while initiating share buyback authorization limited at roughly up to 2.5% outstanding shares signaling accommodative valuation discipline rather than yield distribution priority currently .

The contractual restrictive covenants embedded within debt instruments entail affirmative/negative provisions constricting some operational flexibilities; however successful emergence from Chapter11 has neutralized enforcement risks temporarily enabling robust refinancing latitude contingent on covenant compliance advances hence strategic focus must maintain stringent adherence enabling future capital market access vital for funding ongoing fleet upgrades plus network developments without incurring disproportionate financing expense escalations visible previously under interim DIP facility arrangements now retired .

Key Risks in a Volatile Aviation Landscape

Several salient risk vectors persist demanding comprehensive ongoing mitigation efforts. Macroeconomic turbulence featuring persistent high interest rates elevated inflation erodes discretionary travel budgets directly impinging load factors while increasing debt servicing costs challenging liquidity buffers cultivated post-restructuring alongside foreign exchange exposure disproportionately affecting U.S.-dollar denominated liabilities compounding refinancing difficulties.[S18]

Legal contingencies stemming from customer litigation episodes during pandemic lockdowns alongside prolonged closure impacts such as the flood-induced Porto Alegre airport suspension amplify reputational vulnerabilities amplified by judicial outcomes unpredictability necessitating reserve provisioning diluting earnings prospects concurrently.[S18]

Operationally disruptions fueled by OEM delays compounded by supply chain shortages constrain scalable growth ambitions potentially elevating unit operating costs amidst tightening competition domestically—requiring dynamic network realignment agility leveraging analytic-driven scheduling optimizations balancing profitability imperatives against capacity commitments fundamental within airline economics.

Sector-wide capital intensity coupled with cyclical demand patterns traditionally predispose airline companies like Azul toward profit volatility necessitating nimble financial management balancing aggressive growth capture against conservative fiscal discipline especially pertinent given recent distressed history.

Monitoring Milestones: What to Watch Next for Azul

Investors and analysts should track pivotal forthcoming developments including the Annual General Meeting slated April 30th 2026 where approval of FY25 results alongside governance remuneration decisions will provide insight into board priorities amidst transitional management dynamics following CFO changeover effective late April.[S3]

Further attention is warranted regarding progression on fleet delivery schedules particularly amid OEM constraint headwinds impacting narrow-body next-gen aircraft integration shaping capacity profiles vital for sustaining market share gains; periodic disclosures illuminating these transitions will be critical.

Finally monitoring evolving credit metrics especially leverage ratios derived post-restatement once full IFRS accounting effects emerge during FY26 filings will signal whether liquidity stabilization continues or if renewed refinancing pressures arise necessitating additional capital measures.

Continued evaluation of operational KPIs such as punctuality rankings sustained improvement trends alongside incremental revenue contributions from non-passenger business units–loyalty programs & cargo–will shed light on diversification effectiveness underpinning margin expansion potentials.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments