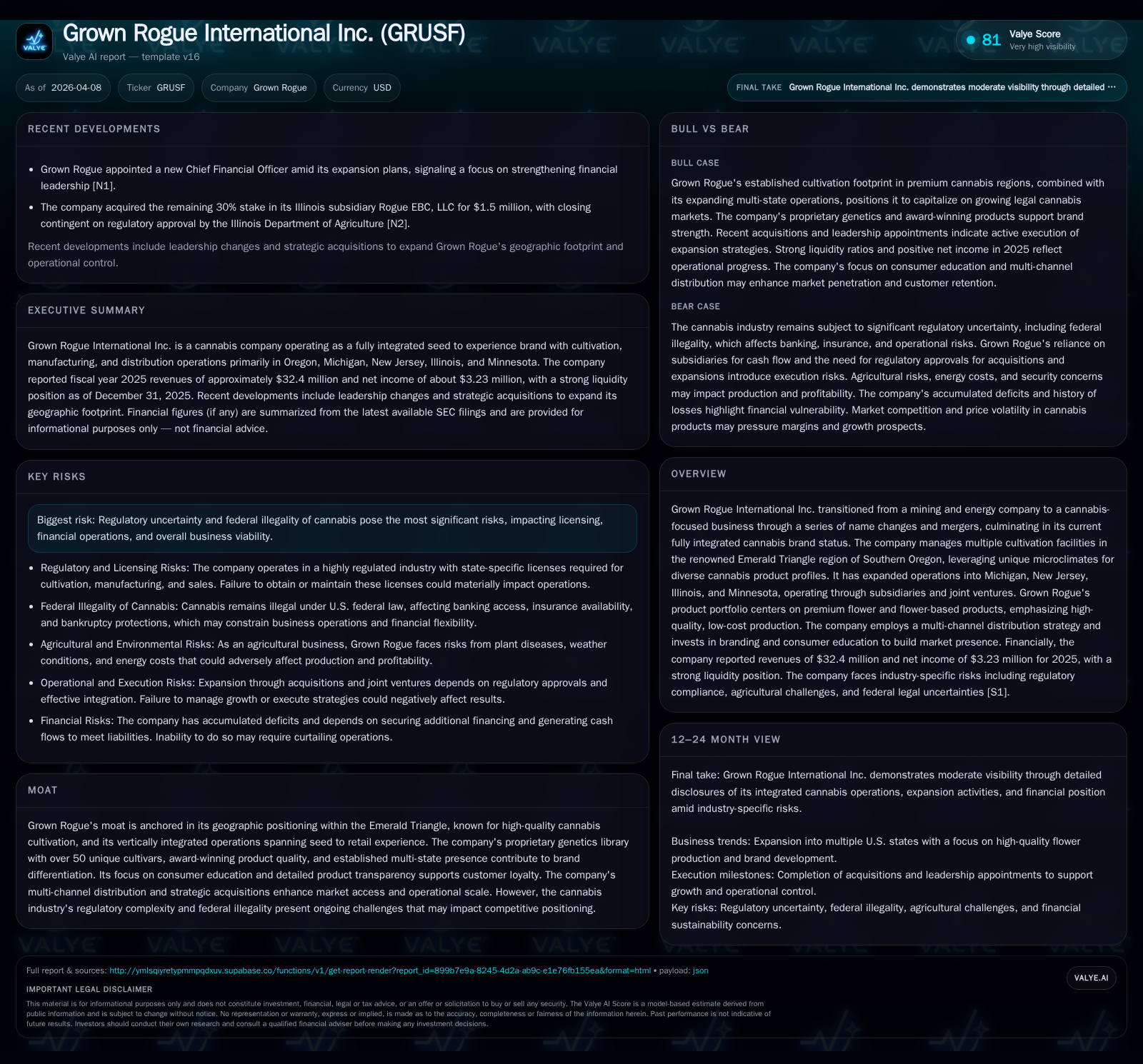

Grown Rogue’s Strategic Rebound: From Mining Legacy to Cannabis Growth Leader

Grown Rogue International has transitioned from its mining origins to become a vertically integrated cannabis producer with growing multi-state operations, leveraging unique regional advantages and operational scale.

Originally founded as a mining company in 1978, Grown Rogue International Inc. has evolved through successive transformations into a fully integrated cannabis business focused on premium flower products cultivated in Oregon’s Emerald Triangle. The company reported a net income turnaround to $3.23 million in fiscal 2025 on revenues of $32.4 million, reflecting operational improvements and expanded geographic footprint including Michigan, New Jersey, Illinois, and Minnesota. Despite positive earnings progress, Grown Rogue continues facing significant challenges from regulatory uncertainties and capital constraints typical of the cannabis sector. Its moat is anchored by premium genetics, cultivation expertise tied to favorable microclimates, and a strategic multichannel distribution platform.

Historical Evolution and Growth Drivers of Grown Rogue

Grown Rogue International Inc. traces its roots to its incorporation in 1978 as Bonanza Red Lake Explorations Inc., initially operating in the mining and energy sectors with multiple name changes over time ([S1]). A strategic pivot began in 2016 when the company divested these legacy assets and briefly entered digital media before fully embracing the cannabis industry through a reverse triangular merger with Grown Rogue Canada and its Oregon subsidiary in 2018 ([S1]). This marked a fundamental shift toward becoming a seed-to-experience cannabis brand.

Central to Grown Rogue's operations is its cultivation footprint within Oregon’s Emerald Triangle — an area renowned globally for its optimal microclimate favorable to sungrown cannabis. The company employs sustainable cultivation methods that capitalize on natural environmental conditions to produce high-quality flower at lower costs compared to indoor grows ([S1], [S8]).

Expansion beyond Oregon has included key acquisitions: the purchase of High Street Capital Partners' growing assets in Medford (2022); acquiring majority interest then full ownership of Golden Harvests in Michigan following regulatory approvals (2023-2025); and entry into New Jersey through ABCO Garden State with licensed cultivation commencing mid-2024 ([S1], [S2], [S24]). More recently, the company has pursued joint ventures and acquisitions targeting craft grower licenses in Illinois and leased cultivation facilities in Minnesota with expected commercial production starting early 2027 ([S13], [S17], [N1]).

Financial Performance Analysis: From Losses to Profitability

The company's financial trajectory shows a significant turnaround from losses to profitability between fiscal years 2024 and 2025 ([F1]). Revenue reached $32.4 million in FY2025 while net income improved dramatically from a loss of nearly $10.7 million in FY2024 to a profit of approximately $3.23 million — representing over a 130% increase year-over-year ([F1]).

Operating income remained slightly negative at about -$0.59 million in FY2025 ([F1]), which may reflect industry-specific tax impacts or non-operating items given the complex Section 280E tax environment affecting cannabis businesses.

Free cash flow was negative around $1.09 million due to ongoing capital expenditures supporting facility upgrades and expansion initiatives despite positive operating cash flow ([F1]). This indicates active reinvestment aligned with growth strategies.

Liquidity remains solid with current assets totaling approximately $22.2 million against current liabilities near $5.7 million as of December 31, 2025, yielding a robust current ratio near 3.9x that supports short-term financial stability amid capital deployment ([F1], [S6]).

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 3 | +130.2% |

| 2024 | -11 |

Source: SEC companyfacts cache [F1].

Note: Cash flow details are discussed contextually due to incomplete uniform disclosure.

Multi-State Footprint and Operational Advantages

Grown Rogue differentiates itself through vertical integration encompassing genetics development, cultivation, processing, distribution channels, and retail partnerships ([S8]). Its proprietary genetics library includes over fifty rigorously tested cultivars supporting product consistency and differentiation—a competitive edge uncommon outside established growers ([S8]). These cultivars leverage Oregon’s unique environmental conditions enabling low-cost premium sungrown flower production.

The multi-state footprint extends vertically integrated capabilities into emerging markets:

- Michigan: Majority ownership of Golden Harvests large-scale cultivation;

- New Jersey: Licensed acquisition of ABCO Garden State cultivation/processing operations along with adult-use dispensary investments;

- Illinois & Minnesota: Joint ventures acquiring craft grower licenses and leasing cultivation facilities targeting commercial production within two years ([S13], [S17], [N1]).

This footprint allows replication of mature Oregon operational expertise across diverse regulatory environments while managing local compliance complexities.

Their multi-channel distribution strategy includes direct-to-retail deliveries where permissible; mandated third-party delivery models (e.g., Michigan); wholesaler relationships; plus supplying raw materials for processors producing retail-ready products—maximizing market penetration while mitigating distribution risks inherent in fragmented U.S. cannabis laws ([S8]).

Regulatory Complexities and Industry Risks

Federal illegality of cannabis remains a primary risk factor contributing to regulatory uncertainty across states ([S4], [S23]). The company faces taxation challenges under IRS Section 280E restricting deductions except for cultivation/manufacturing costs despite efforts such as fiscal year-end changes aimed at mitigating this impact ([S1]).

Licensing delays or failures could disrupt operations significantly ([S5], [S26]), compounded by risks that third-party suppliers may suspend services fearing federal prosecution jeopardizing supply continuity ([S5], [S26]).

Additional challenges include market price volatility requiring adaptive product innovation (reflected by ongoing genetics additions) ([S27]), exposure to rising energy costs impacting operational margins ([S7]), intellectual property protection hurdles due to federal status ([S7]), physical security risks at facilities, alongside potential litigation related to SEC administrative proceedings affecting securities registration status ([S4], [S14], [S29]).

Capital Structure and Allocation Priorities

As of December 31, 2025, Grown Rogue held over $10 million in cash equivalents with total current assets around $22 million against liabilities near $5.7 million supporting working capital needs despite an accumulated deficit exceeding $43 million historically ([F1], [S6]). Trade payables have decreased but remain material reflecting ongoing obligations.

The company does not anticipate paying dividends or conducting share repurchases; capital is primarily allocated toward reinvestment for geographic expansion and scaling operations amid cash flow pressures coupled with capex commitments ([S11], [S24], [F1]). This aligns with negative free cash flow reflecting strategic asset development.

Recent leadership changes including the April 2026 appointment of a new CFO underscore focus on strengthening financial oversight during accelerated multi-state growth amid prior SEC reporting challenges requiring enhanced governance controls ([N1], [S4]). Access to financing remains critical as inability to refinance or raise capital could materially constrain operational continuity ([S6], [S29]).

Leadership Changes and Strategic Expansion Plans

The new CFO appointment coincides with active acquisition efforts such as the pending Illinois Sea Craft craft grower stake purchase awaiting regulatory approval documented as of March 2026 ([S13], [S17]). CEO Obie Strickler emphasizes organic growth complemented by selective acquisitions designed to generate scale benefits without disproportionate dilution risks relative to incremental cash flows generated—supported by controlled equity option pools disclosed for fiscal years ending December 31, 2024 and 2025 ([N1], [F1], [S19]).

Management aims to replicate refined systems proven successful in Oregon across newer jurisdictions balancing licensing risk against first-mover advantages including brand establishment supported by education programs for retail partners integral to sales strategy execution ([S8]).

Market Opportunities Ahead and Key Milestones

Forward-looking guidance is limited per disclosures; however key milestones include:

- Regulatory approvals pending for Illinois Sea Craft acquisition,

- Completion targeted mid-April 2026 for New Jersey Grandview Phase II construction,

- Anticipated commercial product launch early 2027 for Minnesota facility,

- Continued expansion of proprietary cultivar portfolio responding to evolving consumer preferences,

- Strategic positioning for potential federal deregulation enabling interstate export leveraging Oregon’s Emerald Triangle comparative advantage highlighted within sustainability-focused business models emphasizing water reclamation and nutrient recycling critical for cost competitiveness ([S13], [S18]).

Investors should monitor these developments alongside federal legislative trends impacting banking access or national legalization prospects which could significantly alter cost structures presently challenged by Section 280E tax implications.

Disclaimer: This analysis is based solely on information publicly available through SEC filings dated up to April 8, 2026; pertinent news releases; and sector knowledge conventions applicable as of that date. It does not constitute investment advice or recommendations regarding securities mentioned.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments