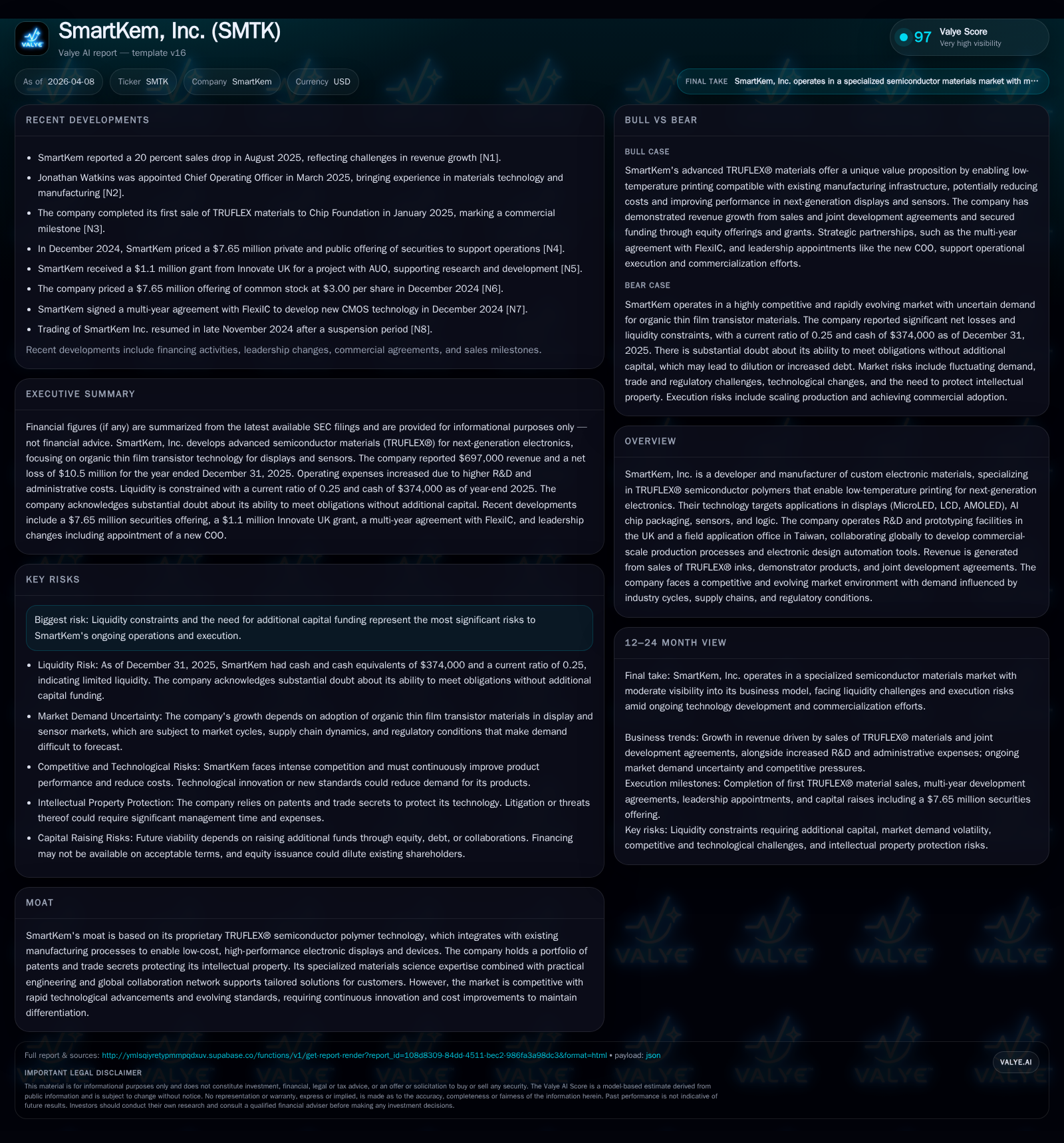

SmartKem’s TRUFLEX Technology: Revenue Surge Meets Capital Strain

SmartKem witnessed explosive revenue growth in 2025 driven by its proprietary semiconductor polymers, while facing pressing liquidity challenges that pose risks to sustained operations.

SmartKem, Inc. achieved a dramatic leap in revenues from sales of its TRUFLEX® semiconductor polymer materials and joint development agreements, increasing top-line nearly ninefold in 2025 over prior year levels. Despite this commercial expansion, the company remains burdened by significant operating losses and a cash runway that is critically short, with liquidity measures indicating notable solvency concerns. Research and development spending supports ongoing product innovation crucial to maintaining its competitive moat, although capital allocation constraints limit optionality. Going forward, the interplay between scaling commercial adoption of its OTFT-compatible materials and securing additional capital funding will be determinative for SmartKem's strategic trajectory.

Strong Revenue Acceleration From TRUFLEX® Ink Sales

SmartKem exhibited a compelling top-line acceleration in fiscal year 2025 with revenue reaching $697 thousand, up sharply from $82 thousand in 2024—a staggering increase of approximately 750% year-over-year [F1]. This surge was largely fueled by ramping sales of its proprietary TRUFLEX® semiconductor polymer inks and demonstration products alongside several completed joint development agreements that collectively contributed $508 thousand to the year’s revenue [S18]. This rapid expansion is illustrative of early-stage commercialization where breakthrough polymeric materials are transitioning from prototype phases toward initial market traction.

However, this revenue growth contrasts markedly with persistent operating losses totaling $12.8 million in 2025, representing a deterioration of roughly 23% relative to the prior year's loss of $10.5 million [F1]. These losses reflect elevated costs associated with production scale-up efforts, prototype fabrication activities involving organic thin film transistors (OTFTs), and general administrative overhead necessary for ongoing R&D and market development [S18]. The net loss correspondingly expanded modestly to $10.5 million [F1], signaling continued cash consumption characteristic of smart materials firms investing heavily ahead of profitable commercial scale.

Evolving Market Dynamics and Proprietary Material Advantages

SmartKem's core technological edge lies in its TRUFLEX® semiconductor polymers uniquely designed to integrate with existing manufacturing processes enabling low-temperature printing techniques essential for next-generation electronics production [S1]. This capability is particularly vital for application fields such as MicroLED and AMOLED displays, AI chip packaging solutions relying on flexible substrates, sensor technologies requiring novel organic materials, and logic components leveraging OTFT architectures [S1]. The advantage stems from materials that accommodate fabrication compatibility with legacy fabs while enabling cost efficiencies through reduced thermal budgets.

Within this sector, competition is intense and marked by continuous innovation pressure where performance enhancements—such as improved charge carrier mobility—and cost reductions drive differentiation [S1]. SmartKem's moat combines proprietary patents protecting its polymer chemistry alongside trade secrets covering manufacturing process know-how—a critical formula given rapid advance cycles within organic semiconductor domains [S1]. However, the company cautions about fluctuating demand tied to industry cycles, supply chain disruptions typical in specialty chemical supply lines, geopolitical trade uncertainties impacting material availability or customer access, as well as standard evolution which can render existing solutions less competitive over time [S1]. Consequently, maintaining leadership requires sustained R&D investment paired with agile go-to-market strategies.

Liquidity Challenges and Funding Imperatives

Financially, SmartKem confronts acute liquidity pressure underscored by a paltry $374 thousand cash balance as of December 31, 2025 down steeply from $7.1 million at end-2024 [F1][S5]. The current ratio stands at approximately 0.25 (current assets of $1.5 million against liabilities near $5.9 million), spotlighting a working capital deficit indicative of immediate solvency risk [F1]. Operating cash flow reflects consistent negative burn -$7.7 million in 2025 slightly improved versus prior years but still draining capital reserves significantly [F1][S4][S28]. Capital expenditures rose moderately due to investments in lab equipment needed to advance prototyping capabilities ($123K in FY25 versus $75K prior) [F1][S9][S15].

To address these gaps, management orchestrated several financings early in 2026: notably a private placement involving Series A Convertible Preferred Stock alongside warrants generating gross proceeds above $4.6 million (subject to issuance expenses) designed primarily for working capital support [S16]. Additionally, the company entered into short-term secured note arrangements aggregating approximately $3.75 million issued at a discount intended partly to bridge funding until further equity raises can be pursued [S20][S26]. While these transactions alleviate immediate stress somewhat, management openly acknowledges substantial doubt about sustaining operations without continued new capital infusions given current burn trajectories and limited near-term revenue visibility [S4][S6]. Equity dilution and debt covenant risks loom large depending on timing and scale of further financings.

Research & Development Investment as a Growth Catalyst

Research and development expenditure grew materially by nearly $2 million reaching $7.0 million in 2025—accounting for almost half (49%) of total operating expenses—reflecting heightened activity around prototyping OTFT devices using the TRUFLEX® portfolio as well as patent filings crucial for preserving intellectual property barriers [S9][S10][F1]. The boost mirrors operational focus pivoting from basic R&D toward applied engineering supporting scale readiness downstream.

Patent and licensing costs continue to be expensed as incurred since realization remains uncertain; however these outlays underscore commitment toward defensive IP strategy important amid aggressive sector patent races [S10]. Governmental research grants and tax credits valued around $1 million annually provide partial offset against R&D spend but do not materially change net cash requirements [S9][F1]. Lab infrastructure capex similarly ticked higher aligned with enhanced experimental throughput needs.

Operational Losses and Capital Deployment

Operating expenses climbed approximately 24% year-on-year driven both by expanding research costs and incremental administrative overhead rising due to professional fees linked with being a publicly listed entity plus investor relations expenditures ($7.4 million G&A expense up from $6.3 million) [S18]. Despite improved revenue scale gains from polymer ink commercialization initiatives, gross margin challenges persist because direct product cost increases accompany volume growth while fixed costs remain largely embedded [S18].

Free cash flow remained deeply negative around -$7.9 million after deducting capex reflecting investment stage status devoid of dividend payouts or share repurchases nor feasible under liquidity constraints—consistent with management focus on extending runway through external capital rather than returning cash to shareholders presently [F1][S27]. Contemplated future funding avenues include equity offerings complementing selective strategic alliances or licensing deals substituting direct spend with collaborator resources as mitigation tactics.

Strategic Risks: Competition, Trade, and Intellectual Property

In an industry characterized by ongoing innovation cycles focused on higher mobility OTFT semiconductor polymers incorporated into flexible electronics manufacturing ecosystems, SmartKem competes against established players investing heavily into similar organic electronic films capable of meeting emerging display resolution demands and sensor integration protocols [S1]. Any lapse or delay innovating could erode market positioning quickly.

Trade policy volatility also poses risk: tariffs or export controls might restrict flows of key raw materials or limit sales channels especially given global supply chain complexities prevalent since recent geopolitical shifts affecting electronics component segments broadly [S1][S8]. To counter intellectual property infringement risks intrinsic to technology niches heavily protected by extensive patent portfolios across jurisdictions SmartKem relies on rigorous patent prosecution plus confidential know-how safeguards complemented by legal vigilance despite currently no active litigation reported [S8][S11]. Nonetheless prospective enforcement actions would consume resources detracting from core technical progress if invoked.

Outlook: What to Watch on Commercial Adoption and Financing

Looking ahead into the coming quarters and medium term horizon several critical factors will determine SmartKem's capability to convert technological promise into sustainable business growth:

- Commercial scale-up: Transition beyond selling demonstrator products toward broader commercial adoption across MicroLED display makers or AI packaging suppliers will signal validation of TRUFLEX®’s utility and ramp revenue materially.

- Partnership & collaboration wins: Expansion of joint development agreements or licensing structures improving recurring revenues while dispersing risk could help diversify income streams.

- Fundraising success: Given current funds cover only limited upcoming months’ expenses amid recurrent sizable losses management’s ability to raise fresh equity or convertible instruments without onerous terms will dictate survival probabilities.

- Cost control: Sustained R&D efficiency improvements enabling flat or reduced absolute spend while expanding output could balance financial position.

Absent visible near-term profitability or robust multi-year contracts the narrative remains one of high innovation combined with high execution risk typical for advanced organic semiconductor material developers reliant on nascent markets adapting complex fabrication integration requirements.

Historical Financial Performance: FY2022-FY2025

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 697000 | -11 | -8 | -13 | +750.0% | -1.7% |

| 2024 | 82000 | -10 | -8 | -10 | +203.7% | -21.5% |

| 2023 | 27000 | -8 | -8 | -10 | -32.5% | +26.1% |

| 2022 | 40000 | -11 | -9 | -10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -8 | 267.1 |

| 2024 | -8 | -156.7 |

| 2023 | -8 | -104.8 |

| 2022 | -9 | -195.4 |

Source: SEC companyfacts cache [F1].

Table notes: Revenue soared on strong TRUFLEX® sales growth driving increased COGs; losses deepened alongside expanded R&D investment; operating cash flow remains substantially negative consistent with growth-stage smart materials firms; capex uptick aligns with upgraded lab equipment procurement [F1].

Disclaimer: This analysis is for informational purposes providing an overview based solely on publicly filed financial data and disclosures as of April 8th, 2026 without investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments