Axil Brands’ Financial Momentum Faces Headwinds After Key Retail Gains

Growth fueled by prominent retail partnerships gave way to Q3 earnings pressures, prompting scrutiny of Axil’s operational resilience and capital use.

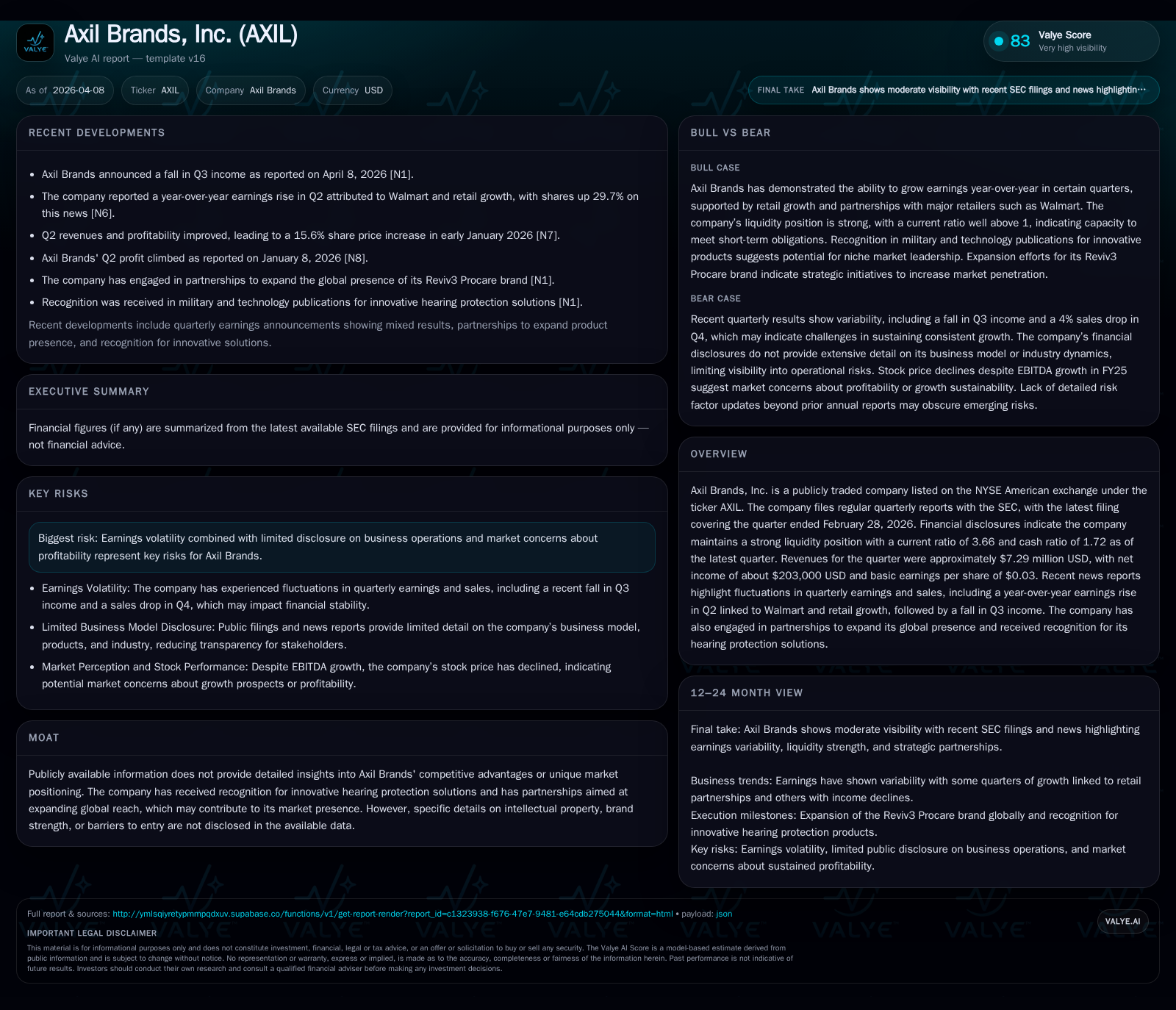

Axil Brands, Inc. demonstrated strong revenue expansion through FY2024 driven largely by retail distribution channels, including Walmart, which bolstered top-line growth and profitability. However, fiscal 2025 showed a modest decline in revenue alongside sharper contractions in operating and net income, culminating in a pronounced dip in Q3 earnings early in 2026 amid margin challenges and elevated costs. The company maintains robust liquidity with a current ratio well above 3.5, supports shareholder value through ongoing share repurchases, and pursues global market expansion despite inherent scaling risks. Profitability metrics indicate improving operating cash flows that contrast with the net income softness, underscoring working capital dynamics that require monitoring going forward.

Revenue Trajectory and Historical Growth Drivers

Axil Brands recorded substantial revenue growth between FY2023 and FY2024, expanding from approximately $23.5 million to nearly $27.5 million USD—a notable 17% increase year-over-year [F1]. This acceleration followed earlier years marked by modest or negative revenue trends; FY2022 revenue was roughly $2.3 million before the sharp upswing commenced. The subsequent fiscal year ending May 2025 saw a revenue contraction of about 4.5%, settling at $26.3 million USD, signaling pressures emerging after the peak growth phase.

Operating income tracked a similar pattern but with amplified volatility: from a negative operating income position of -$211k in FY2022 to over $1.9 million in FY2023, before retreating more than 20% in FY2024 and another substantial decline of nearly 23% in FY2025 to about $1.16 million USD [F1]. Net income mirrored these swings but with steeper declines; it peaked at over $2 million USD in FY2024 then fell by approximately 57% down to under $855k USD in FY2025.

These figures indicate that while top-line growth initially accelerated strongly due to favorable sales channels and possibly enhanced brand acceptance (discussed below), cost structures or margin pressures eroded profitability significantly during the latest fiscal period.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 26 | 1 | 2 | 1161365 | -4.5% | -57.3% |

| 2024 | 27 | 2 | 0 | 1503380 | +16.9% | +9.8% |

| 2023 | 24 | 2 | 3 | 1984211 | +906.8% | +1097.6% |

| 2022 | 2 | 0 | 0 | -211403 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1246490 | 2 | 8.9 |

| 2024 | 1246490 | 0 | 26.0 |

| 2023 | 3 | 27.3 | |

| 2022 | 0 | -99.0 |

Source: SEC companyfacts cache [F1].

Figure notes: Values rounded; buybacks data associated with FY24 and FY25 indicate consistent repurchase activity.

Retail Channel Impact and Partnership Contributions

Retail partnerships have been central to Axil’s revenue acceleration, most prominently an expanded distribution deal with Walmart which drove notable sales volume increases registered during recent quarters [N1][S2]. The company's hearing protection products gained retail shelf presence, enhancing brand visibility among mass market consumers.

Such retail channel penetration typically enhances turnover but introduces complexities including promotional pricing pressures and tighter margins due to competitive shelf-space dynamics—a scenario consistent with observed operating margin contractions post initial volume gains.

Moreover, logistics associated with servicing large retailers often require significant coordination of inventory flows and compliance with strict vendor requirements, potentially impacting cost structures during rapid scale-ups.

Q3 Earnings Decline: Dissecting the Recent Setback

Despite previous quarter gains, Axil’s Q3 results disclosed a decline in net income highlighting operational headwinds [N1][S2]. Margin compression appears paramount—heightened cost of goods sold coupled with fixed expenses undermined operating leverage benefits.

Inventory adjustments may also have contributed as management seeks to optimize stock levels post-retail ramp-ups.

The combination of these forces curtailed profitability despite sustained revenue levels close to prior quarters, illustrating the sensitivity of earnings to supply chain efficiencies and pricing power constraints within competitive retail environments.

Global Expansion Efforts and Market Penetration

Continuing efforts toward global footprint expansion are underway via new strategic partnerships aimed at leveraging Axil’s hearing protection solutions beyond core domestic markets . While explicit details are limited, such scale-up initiatives face challenges including regulatory diversity across jurisdictions and incremental channel development costs.

Success depends on effective localization strategies alongside maintaining innovative product features that differentiate offerings against entrenched international competitors.

Current Liquidity Strength and Capital Structure Overview

Axil reported strong liquidity metrics as of February 28, 2026: a current ratio of approximately 3.66 reflects substantial short-term asset coverage beyond liabilities [F1][S14].

This liquidity provides operational resilience to absorb episodic market pressures or fund strategic investments without immediate external financing dependence.

Debt appears minimal or managed conservatively given the absence of significant disclosures indicating leverage risks; thus capital structure supports flexibility amidst earnings cycle fluctuations.

Capital Allocation Strategy: Buybacks and Investments

Share repurchase programs have been consistently implemented since at least FY2024 with annualized buybacks totaling around $1.25 million USD each year [S7–S11][F1]. These indicate a priority on returning capital or supporting equity price stability rather than dividend distributions—the latter notably absent from recent communications.

Capital expenditures increased by over half in FY2025 compared with prior years but remain modest relative to operating cash flows suggesting measured reinvestment focused likely on capacity or capability enhancements rather than aggressive expansion capex bursts.

Profitability Metrics and Return on Equity Analysis

Despite net income softness, Axil’s operating cash flow surged dramatically to almost $1.93 million USD for FY2025—an increase exceeding seventy thousand percent compared to negligible CFO reported for FY2024—likely reflecting improved working capital management or non-cash adjustments [F1].

Such disparity warrants attention as cash flow health partially offsets headline earnings weakness offering some cushion for funding operations or returns.

Return on equity approximates near 8.9% for FY2025 using net income over equity values pointing to positive value creation albeit at modest levels given volatility context.

Risks Amid Earnings Volatility and Market Ambiguities

Risk disclosures remain largely static over recent filings emphasizing historical themes related to earnings variability and limited operational disclosure scope impacting investor clarity [S4–S6].

Lack of a clearly articulated competitive moat combined with profit pressure stemming from competitive retail channels present ongoing challenges for sustainable margin improvements.

Additionally, evolving regulatory environments internationally add uncertainty as global expansion proceeds.

Outlook Considerations and Key Indicators to Monitor

Looking forward, critical monitoring areas include sales momentum within expanding retail alliances versus wholesale segments; gross margin trends reflecting input cost pressures; efficiency ratios tied to capital expenditures; progress on international partner integrations; and quarterly cadence updates particularly for Q4 fiscal periods per disclosed reporting calendars [N1][S2].

Potential downside scenarios may emerge if global rollout delays materialize or if competitive-driven margin squeezes intensify beyond manageable thresholds.

This analysis synthesizes publicly available financial data alongside recent corporate disclosures pertinent to Axil Brands’ evolving business profile through early calendar year 2026 without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments