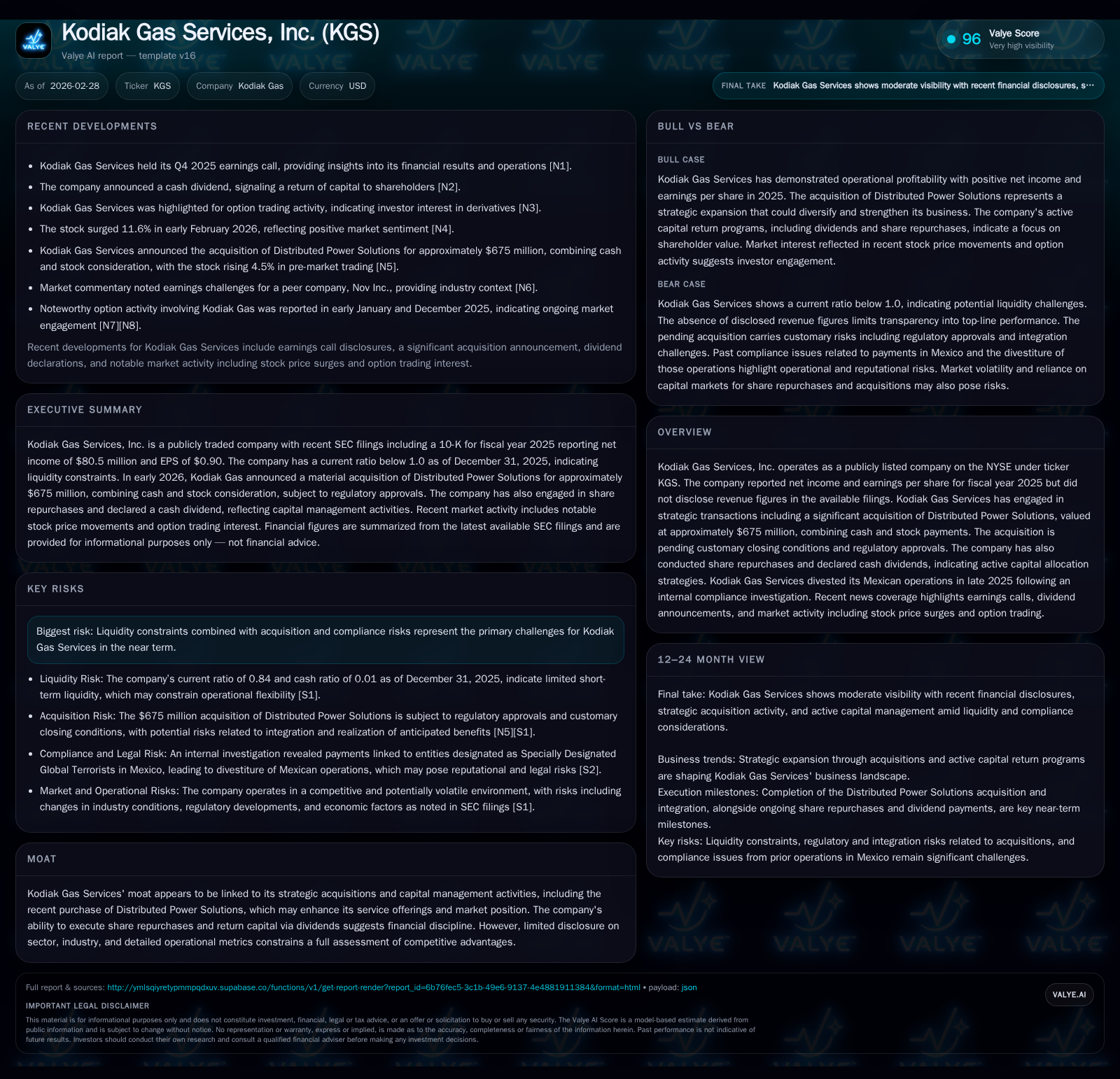

Kodiak Gas Services Bolsters Growth With $675M Distributed Power Buyout

Kodiak Gas Services' 2025 financial surge is driven by its strategic acquisition of Distributed Power Solutions and disciplined capital management despite compliance and liquidity challenges.

Kodiak Gas Services reported substantial growth in operating income, net income, and cash flow for fiscal year 2025, underscoring operational strength ahead of its $675 million acquisition of Distributed Power Solutions. The acquisition, pending regulatory approval, marks a strategic expansion into distributed power services, though integration and compliance risks remain. Kodiak maintained robust capital allocation through increased dividends and share repurchases supported by strong free cash flow, even while navigating liquidity constraints and divestiture of Mexican operations due to a compliance investigation.

Robust Financial Performance Signals Operational Strength in 2025

Kodiak Gas Services demonstrated formidable financial momentum in fiscal year 2025. Operating income climbed to approximately $340 million from $249 million a year earlier, marking a robust 36% year-over-year increase [F1]. This gain was powered by improved operational efficiency which aligns with industry norms where midstream gas service providers optimize workover activities and gas compression services coupled with prudent capital expenditure management to enhance margins. Notably, Kodiak curtailed capex by about 6% after a jump the previous year reflecting capital discipline juxtaposed with expansion needs [F1].

Net income leapt to just above $80 million from $50 million in FY2024—a remarkable 61% increase—highlighting both top-line operating leverage and effective cost controls amidst a complex business environment [F1]. Operating cash flow nearly doubled to around $600 million during this period, an impressive +83% gain that underscores significant improvements in working capital management and collection efficiency [F1]. These cash inflows provided a foundation for Kodiak’s aggressive capital deployment strategies.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 81 | 600 | 340 | 315 | +61.4% |

| 2024 | 50 | 328 | 249 | 337 | +148.7% |

| 2023 | 20 | 266 | 244 | 220 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 160 | 104 | 284 |

| 2024 | 36 | 40 | -9 |

| 2023 | 30 | 47 |

Source: SEC companyfacts cache [F1].

Table: Annual financial summary reflects Kodiak's operating strength and growing shareholder distributions [F1]

Strategic Acquisition of Distributed Power Solutions: Implications and Risks

In early February 2026, Kodiak announced it would acquire Distributed Power Solutions (DPS) for roughly $675 million funded through approximately $575 million in cash plus issuance of about 2.4 million shares valued at some $100 million [S3][S8][S9][N7]. This transformative transaction extends Kodiak’s footprint into specialized distributed power generation services where DPS operates.

The deal hinges on customary closing conditions including regulatory approvals under the Hart-Scott-Rodino act; expected closure is targeted for early April with a May “Outside Date” for termination rights if conditions lag [S9][S19]. The purchase agreement embeds lock-up provisions constraining DPS sellers from disposing stock for six months post-close plus restrictive covenants limiting competitive behaviors over three years — typical protective measures for integration risk mitigation [S11].

Acquisition accounting will likely introduce goodwill reflecting DPS’s intangible assets; however, synergy realization is contingent on effective integration post-closing with risks including talent retention challenges and customer disruption [S8][S9]. Additionally, Kodiak secured representations and warranties insurance (RWI Policy) to partially hedge indemnification exposures linked to DPS’s pre-acquisition liabilities [S21].

The DPS integration represents both an opportunity for margin expansion via cross-selling between midstream gas services and distributed power solutions but also amplifies exposure to competitive dynamics in distributed generation sectors which face supply chain fluctuations for power equipment [N7][S9].

Capital Allocation Strategy: Dividends, Share Repurchases, and Cash Flow Management

Kodiak’s capital discipline came to the fore as its free cash flow (operating cash flow minus capex) ballooned to roughly $284 million in FY2025 facilitating sizeable shareholder returns despite strategic acquisition spending [F1]. Dividend distributions soared more than fourfold to approximately $160 million from only $36 million in prior year underlining management’s commitment to yield enhancement even amid transitional investments [F1][N3][S14].

Share repurchase activity intensified markedly reaching around $104 million versus $40 million a year prior as part of an ongoing buyback program that also included a notable stock purchase during the late-2025 secondary offering at prices near $33 per share [S25]. Maintaining such capital return initiatives augments investor confidence in Kodiak’s operational cash flow yield optimization tactics amidst cyclical volatility.

Balancing aggressive dividends/buybacks with acquisition funding demonstrates prudence but will require close monitoring of leverage ratios given liquidity headwinds signaled elsewhere [F1][S14]. This dynamic interplay between inorganic growth investments and shareholder payout mandates illustrates Kodiak's evolving financial stewardship approach.

Compliance Setbacks and Market Reactions: Assessing the Mexican Operations Divestiture

Late in calendar year 2025, Kodiak divested its Mexican operations following an internal compliance investigation—an episode casting short-term reputational risk shadows over the company’s governance profile [N6]. Though not quantified materially within disclosed figures, the divestiture materially trimmed the company’s geographic diversity.

Investor reactions surfaced swiftly reflected in pronounced volatility including an approximate double-digit percentage surge in stock price shortly thereafter as broader market participants digested potential risk containment benefits versus operational contraction concerns [N6]. Regulatory scrutiny on cross-border operations remains a persistent risk vector warranting vigilance considering Kodiak's expanding footprint through DPS acquisition.

Liquidity Challenges and Debt Profile: Navigating Near-Term Financial Constraints

Kodiak concluded FY2025 with current assets totaling about $323 million against current liabilities marginally higher near $386 million yielding a suboptimal current ratio of roughly 0.84—a key indicator spotlighting liquidity tightness despite strong cash generation capacity [F1][S7].

This less than one-turn working capital ratio underscores reliance on efficient receivables collection cycles and revolving credit facility access for bridging timing mismatches amid elevated debt levels incurred from acquisition financing activities [F1]. Leasing commitments tied to equipment operations further weigh upon liquidity reserves.

The company faces upcoming maturities within its debt schedule requiring railing on covenant compliance benchmarks while preserving buffers essential for operational agility throughout DPS integration phases [S7][S16][S17]. Although free cash flow coverage appears adequate presently, incremental leverage pressure mandates cautious monitoring.

Future Growth Outlook: Opportunities Amid Industry Dynamics and Integration Risks

Management’s forward-looking commentary highlights optimism regarding organic growth potentials fuelled by enhanced distributed power offerings post-DPS deal completion together with synergies extracted from cross-selling upstream midstream services into new client bases [N2][N7][S9]. Expectations are set on expanding market share leveraging combined technological expertise while pursuing margin uplift via operational scale.

However, these prospects are tempered by execution uncertainties intrinsic to large-scale acquisitions including cultural fits, supply chain disruptions especially given recent global generator shortages affecting distributed power sectors, alongside potential competitive encroachments within core markets [S9]. A deliberate focus remains on synergy realization timelines critical for validating acquisition rationale against inherent integration costs.

Analyst Expectations and Key Milestones to Watch Through 2026

Recent earnings calls forecast continued EPS growth alignment driven by full-year contribution from DPS alongside sustained strong operating cash flows underpinning dividend policies that may trend higher given robust payout ratios realized thus far [N1][N2][S3]. Share repurchase programs remain active but will be calibrated consistent with liquidity provisioning amid debt servicing needs.

Investors and analysts will keenly monitor regulatory clearance progression for the DPS acquisition expected around April-May timeframe alongside quarterly performance metrics signaling integration success or emerging headwinds. Dividend declarations scheduled quarterly starting February pay date offer immediate yield visibility supportive of valuation frameworks.

Overall market focus coalesces around balancing growth ambitions anchored by inorganic expansion against maintaining capital discipline manifested via returns consistency amid ongoing compliance risk management.

This report synthesizes publicly available SEC filings and recent news coverage without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments