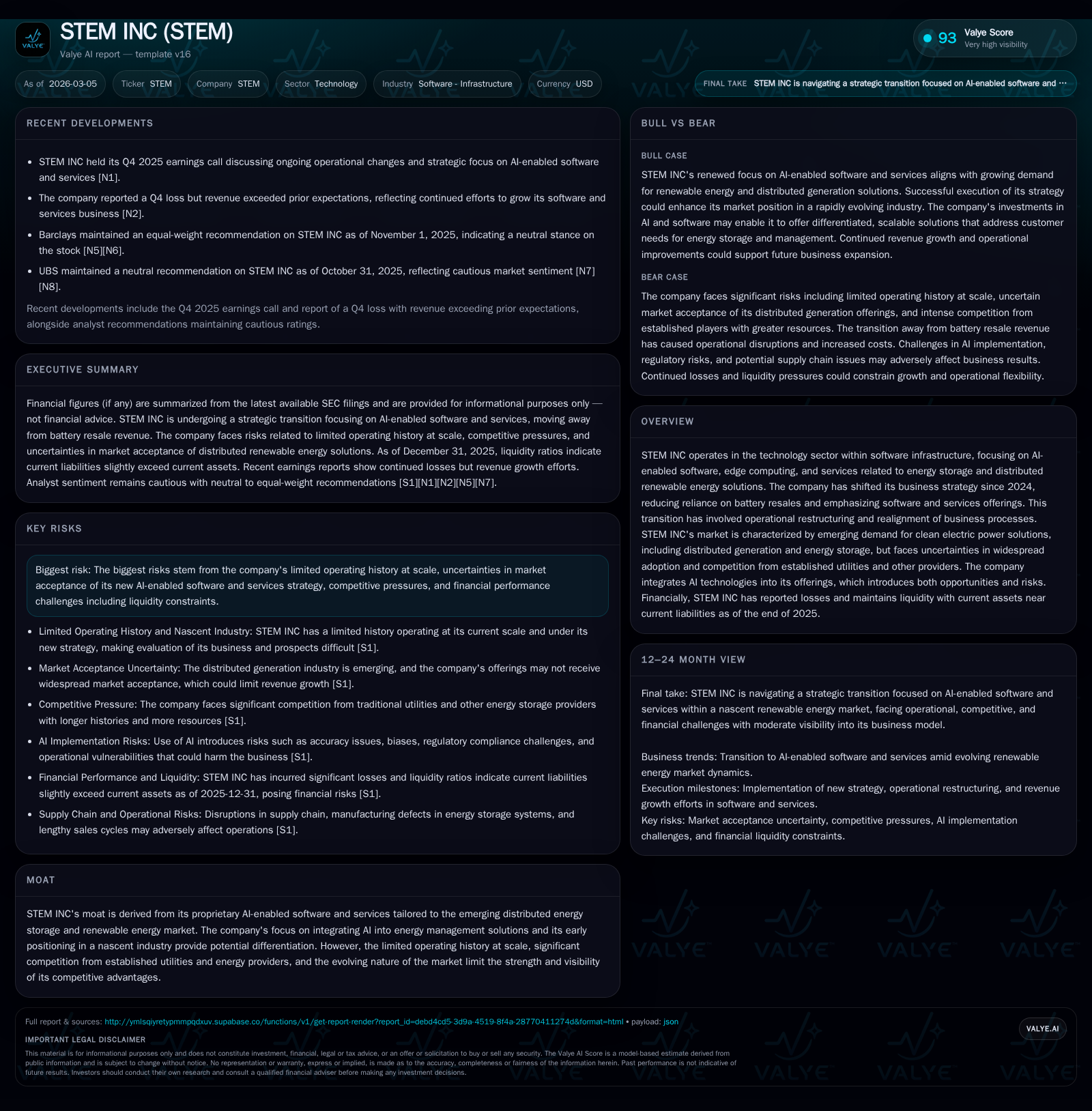

STEM INC's Strategic Shift Challenges Revenue Growth and Profitability Amid Supply and Market Risks

The company’s operational pivot toward AI-enabled software and services presents both a path for future growth and challenges including sustained losses and liquidity pressures.

STEM INC has been transitioning its business model since 2024, moving away from battery resales to emphasize AI-driven software and services in energy storage and distributed renewable solutions. This shift caused revenue decline and operational disruptions, reflected in significant ongoing losses despite improving operating income trends. The future growth hinges on broad customer adoption of advanced AI-enabled offerings amid supply chain constraints, competitive intensity, and regulatory uncertainties. Monitoring sales cycle execution, backlog conversion, and successful scaling of software services will be critical in assessing milestone achievements.

Historical Performance and Past Growth Drivers

STEM INC’s financial history reveals an ongoing transformation marked by heavy losses but signs of operational improvement. The company historically depended on battery hardware resales as the core revenue source. However, in October 2024, STEM announced a strategic pivot emphasizing AI-enabled software services designed for distributed energy storage systems and renewable energy management [S1], [S12].

This pivotal change involved realigning operations extensively throughout 2024-2025, including cost restructuring and scaling back lower-margin hardware sales [S1]. Such measures led to short-term revenue declines but aimed at growing higher-margin software services over time.

The table below summarizes key financial metrics over the past four fiscal years [F1]:

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) |

|---|---|---|

| 2025 | 7 | -56 |

| 2024 | -37 | -839 |

| 2023 | -207 | -179 |

| 2022 | -106 | -131 |

Source: SEC companyfacts cache [F1].

Operating income improved significantly from a deep loss in 2024 but remains negative after more than a decade of accumulated deficits exceeding $1.48 billion by end-2025 [F1]. Notably, operating cash flow turned positive in fiscal year 2025—a key sign of better underlying cash management despite ongoing losses [F1]. Equity turned negative by end-2025 following prior years of positive equity balances indicating balance sheet stress.

Future Growth Prospects

STEM’s renewed focus on AI-driven platforms like its PowerTrack system (formerly Athena) aims to capitalize on growing demand for clean electricity solutions that are reliable and cost-effective [S1]. The potential market resides in integrating distributed energy storage with smarter grids using data analytics to optimize usage.

Nonetheless, market acceptance remains uncertain since widespread deployment relies on evolving regulations, customer financing decisions, and proving technology performance at scale [S12], [S26]. The company must educate customers during lengthy sales cycles lasting up to 18 months due to technical complexity and project permitting [S26].

Additional growth catalysts include leveraging government incentives such as provisions from the Inflation Reduction Act that support renewables [S26], technical enhancements via R&D investments into AI capabilities [S10],[S16], and international expansion tempered by geopolitical supply chain risks [S24].

Conversely, growth could be capped by competition from utilities entrenched with incumbency advantages or better capital access as well as external factors like tariff impacts on component costs introduced after April 2025 [S24]. Supply chain fragility around lithium-ion batteries is another constraint that may affect equipment availability or pricing [S24].

Forecasts, Milestones, and What to Watch

STEM has not issued explicit numeric guidance publicly for fiscal year 2026 or beyond [N2], but strategic priorities center on scaling software services revenue while controlling costs post-restructuring [S26]. Key milestones will likely revolve around increasing booking conversion rates from backlog given the long sales/install cycle; onboarding new customers onto AI platforms; sustaining supplier relationships under tighter capacity conditions; and progress in reducing operating losses towards breakeven.

Managing issues such as software platform stability—including cybersecurity resilience—and product defect mitigation will also influence future adoption rates given reported challenges related to complex third-party licenses embedded within PowerTrack [S9]. Improvement in these areas may accelerate go-to-market effectiveness.

Returns and Capital Allocation Considerations

Financially, STEM remains unprofitable with net losses though improving operating income trends suggested by a near-94% improvement YoY between fiscal years 2024-2025 [F1]. Operating cash flow has rebounded sharply into positive territory ($6.9 million), contributing to an estimated free cash flow surplus after capex adjustments of approximately $5.3 million [F1]. However, the balance sheet remains stressed with current liabilities exceeding current assets (current ratio ~0.91) raising concerns about short-term liquidity [F1].

Equity levels have deteriorated significantly due to cumulative losses eroding net assets (negative $249 million equity as of end-2025) limiting scope for dividends or buybacks for the foreseeable future [F1]. Instead, capital allocation priorities appear clearly focused on R&D investments into AI capability expansion and maintaining operational liquidity amid the strategic transition context [S10], without distributions back to shareholders.

Industry Positioning and Competitive Context

STEM operates within the nascent market of distributed renewable energy coupled with intelligent energy storage solutions shaped by rapid technology evolution and regulatory flux [S14], [S17]. Its moat is derived mainly from proprietary AI-powered software that differentiates its platform performance—yet its competitive position is still vulnerable due to limited scale relative to utilities with established infrastructures.

Competition also emerges from specialized firms rapidly advancing capabilities leveraging AI or cloud infrastructure for grid-scale distributed resources monitoring—making STEM’s innovation execution critical for sustaining differentiation [S12], [S17]. Regulatory risks add complexity given evolving environmental standards installation permitting processes that can delay project deployments or incur additional costs that may reduce price competitiveness or margins [S18], [S21].

Operational Risks Highlighted by SEC Filings

Key company-specific risks documented include:

- Uncertain market acceptance timing for AI-based products requiring sustained investment in personnel skilled in machine learning applications under tight labor markets [S16], [S12]

- Supply chain dependencies on few key OEM battery suppliers subject to geopolitical tariffs and capacity limits affecting delivery schedules or cost structures [S7], [S24]

- Lengthy sales/installation cycles (~9-18 months) heightening exposure to cancellations or delayed payments impacting revenue recognition timing [S26]

- Potential product defects or cyber vulnerabilities within complex software platforms that may disrupt client operations or require costly remediation efforts potentially harming reputation and recurring revenue streams [S8], [S9]

- Risks stemming from intellectual property litigations either defending proprietary tech or addressing infringement claims which can divert funds or restrict offerings if adverse outcomes occur [S6], [S11]

- Substantial historic operating losses forecasting continuation at least through 2026 reflecting substantial challenge converting innovation investments into sustainable profitability yet importance of ongoing R&D to future viability remains high [F1], [S16].

Conclusion: A Strategic Pivot With Tangible Challenges Ahead

STEM INC’s transition toward becoming a predominantly AI-software-driven service provider marks a clear evolution aligned with broader shifts toward clean distributed energy solutions but entails near-term financial pain reflected by sustained losses offset partially by improving operational cash flows. Future success depends heavily on expanding market traction for complex digital energy management platforms amidst significant operational headwinds including supply constraints, regulation uncertainty, competitive pressures from incumbents, and execution risk inherent in long sales pipelines.

Stakeholders will want to watch carefully STEM’s pace in backlog conversions into revenues, maintenance of supplier relationships especially amid tariff regimes post-April 2025, progress on product reliability improvements particularly on cybersecurity protocols within its PowerTrack platform, recruitment/retention of key AI talent required for continued innovation investment effectiveness, debt/liquidity metrics given subpar current ratio signaling working capital pressures; as well as any formal guidance updates which currently remain absent.

This report summarizes information available as of early March 2026 based on SEC filings including the annual Form 10-K for fiscal year ended December 31, 2025 ([F1],[S1]-[S29]) and recent news reports ([N1],[N2]). It does not constitute investment advice but aims at comprehensive analysis respecting source data integrity without speculative extrapolation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments