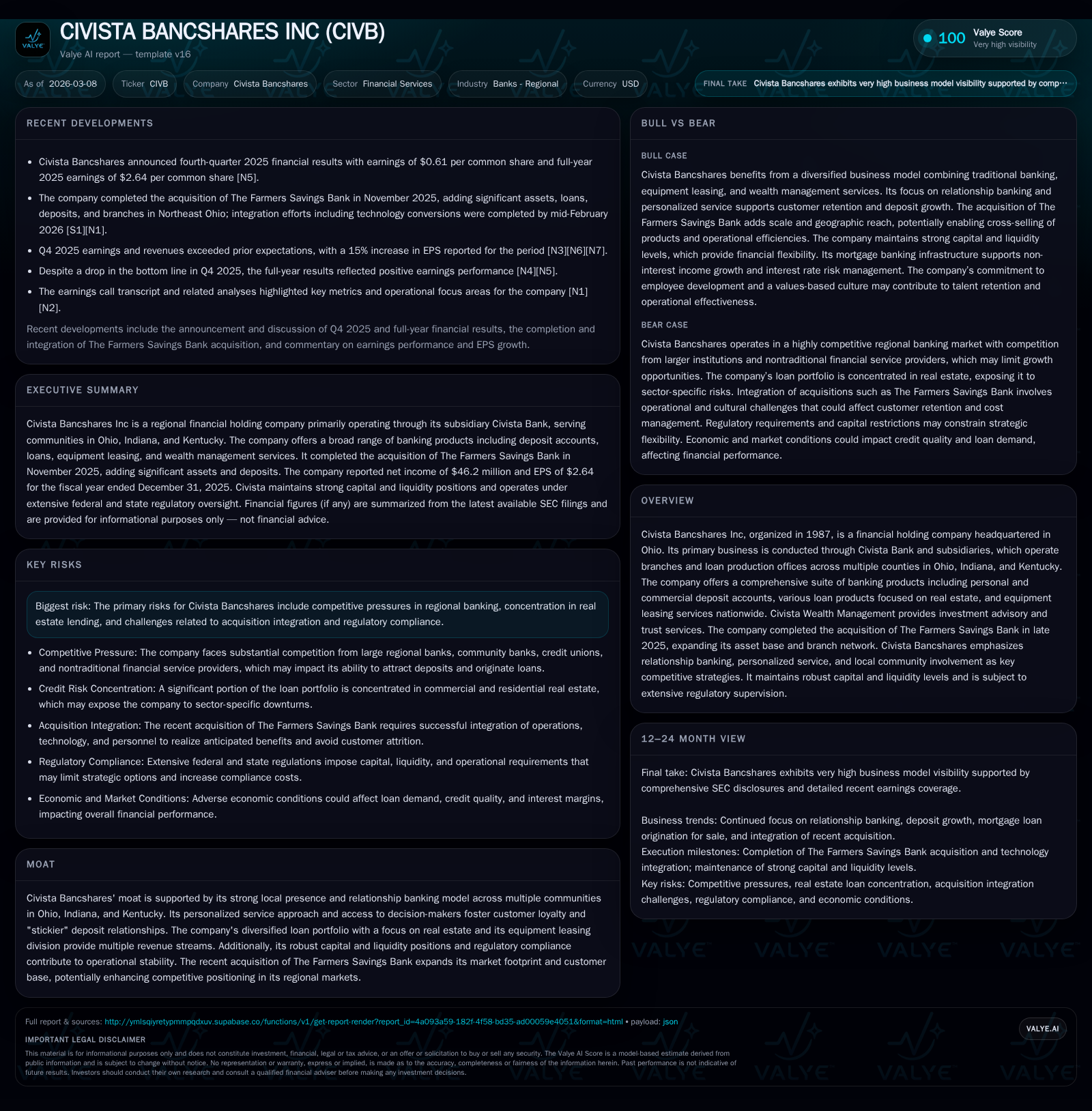

Civista Bancshares Expands Regional Footprint While Maintaining Capital and Operational Discipline

Civista Bancshares grows through acquisition and organic expansion across Ohio, Indiana, and Kentucky with a focus on relationship banking and robust capital management.

Civista Bancshares Inc, a regional financial holding company based in Ohio, delivered solid earnings growth in 2025 driven by expanding loan volumes and the strategic acquisition of The Farmers Savings Bank. The company’s relationship-centric banking model, diversified loan portfolio with real estate emphasis, and expanding equipment leasing business underpin its competitive positioning. Civista maintains a conservative liquidity profile and strong capital ratios, enabling dividend growth and modest buybacks despite a sharply reduced capex spend. Key risks involve competitive pressures in regional markets, concentration in real estate lending, and integration challenges from recent acquisitions.

Historical Performance Overview

Civista Bancshares has demonstrated notable financial resilience over the past several years, culminating in a significant jump in net income during fiscal year 2025. The company's net income rose nearly 46% from $31.7 million in 2024 to $46.2 million in 2025 [F1]. This upward trajectory was supported largely by increased interest income driven by loan volume growth and favorable interest rate movements as detailed in the company’s MD&A [S1]. Interest income from loans increased by approximately $11.9 million on volume expansion while net interest expense fell by about $7.6 million due to changes in funding costs [S1].

Operating cash flows were relatively strong but showed a moderate decline of around 10% to $43.3 million as cash outlays normalized after higher levels in previous years [F1]. Meanwhile, capital expenditures were tightly managed, falling over 70% from prior year levels to just under $1.2 million [F1], signaling prudent reinvestment focusing on efficiency rather than expansion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 46 | 43 | 1 | +45.9% |

| 2024 | 32 | 48 | 4 | -26.3% |

| 2023 | 43 | 63 | 3 | +9.0% |

| 2022 | 39 | 25 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 12 | 0 | 42 |

| 2024 | 10 | 0 | 44 |

| 2023 | 10 | 2 | 59 |

| 2022 | 8 | 17 | 19 |

Source: SEC companyfacts cache [F1].

This performance reflects a combination of steady organic growth complemented by strategic corporate actions.

Business Model and Market Position

Operating primarily through its wholly owned subsidiary Civista Bank, the company serves multiple counties across Ohio, Indiana, and Kentucky with over thirty branch locations complemented by loan production offices and an equipment leasing division nationwide (Civista Leasing & Financing) [S1][N4]. Its business anchors on relationship banking emphasizing personalized service tailored to commercial and retail clientele within these communities.

The company's competitive moat stems from this localized approach—providing client access to decision-makers, quick credit underwriting cycles, and visible community involvement bolstered with technology-infused delivery channels such as mobile/digital banking and remote deposit capture capabilities [S19]. This strategy fosters "stickier" deposit relationships less vulnerable to disintermediation compared to purely transactional or rate-driven competitors.

Loan Portfolio Composition

The loan portfolio remains heavily concentrated in real estate-related lending:

- Commercial real estate loans comprised roughly half of the total portfolio (50%) in 2025,

- Residential mortgage loans grew to represent about 29%,

- Commercial and agriculture loans accounted for approximately 9% [S13][S20].

This concentration aligns with the company’s regional economic exposures but raises potential vulnerability should sector stress arise.

The company actively manages its interest rate risk through originating residential mortgage loans primarily intended for sale into the secondary market, leveraging its mortgage banking infrastructure both as a revenue stream via non-interest income and as a hedging mechanism against longer-duration fixed-rate assets exposure [S6].

Acquisition Impact & Expansion

A pivotal development was the late-2025 acquisition of The Farmers Savings Bank (FSB), which significantly expanded Civista's asset base and branch footprint within Ohio [N4][S1]. This transaction brought additional deposits, new customer relationships, and incremental lending opportunities into Civista’s core markets while offering potential cost synergies through platform consolidation.

Integration efforts are underway but not expected to materially disrupt ongoing operations or regulatory standing given Civista's well-established compliance frameworks [N4][S7].

Capital Structure & Liquidity

Civista exhibits a robust capital position exceeding regulatory benchmarks comfortably:

- Tier 1 leverage ratio stood at approximately 11.3% for the holding company,

- Civista Bank itself maintained an even higher Tier 1 leverage ratio of about12.3% at end-2025,

- Total shareholders' equity expanded toward $543 million during the year reflecting earnings retention and equity issuance proceeds from its mid-year common stock offering that raised roughly $75 million net primarily aimed at paying down short-term Federal Home Loan Bank advances and funding future growth initiatives [S4][S10][S20].

The bank also retained substantial liquidity buffers comprising nearly $77 million in short-term cash equivalents plus over $680 million of readily marketable securities classified as available-for-sale that can be pledged or sold if necessary [S10]. An additional borrowing capacity near $696 million is maintained at the FHLB Cincinnati facility providing supplementary funding optionality.

Returns & Capital Allocation

Return on equity, a key metric for shareholders’ perspective on profitability relative to invested capital, is estimated around low double-digits at approximately 8.5% based on trailing twelve-month net income over shareholders' equity at December 31, 2025 (net income of $46.2M / equity approx. $543M) [F1]. This reflects stable earnings generation given prevailing regional banking conditions.

Capital allocation showed balanced priorities:

- Dividend payments increased about +18% year-over-year reaching approximately $11.8 million in dividends paid reflecting confidence in cash flow generation capacity and commitment to shareholder returns [F1][N14],

- Stock repurchases were very limited ($0.18M), indicating possible conservatism following elevated buyback levels earlier but a pivot back toward preserving tangible capital amid regulatory expectations.

Free cash flow calculated as operating cash flow minus capex shows positive generation near $42M illustrating strong internal funding capability despite softer CFO compared to prior years [F1].

Strategic Priorities Going Forward

According to management commentary, key growth drivers expected include ongoing deepening of existing customer relationships through enhanced service delivery; leveraging newly acquired FSB platform; pursuing prudent commercial loan origins especially real estate-backed; expanding wealth management offerings; and growing equipment leasing operations nationally leveraging integration synergies gained post VFG acquisition merger in August ’23 now operating wholly under CLF branding [N4][S6].

Additionally, ongoing IT investments completed early calendar year ’26 undergird scalability via digital channels supporting efficiency gains without disrupting core operations [S20]. Expense discipline remains a stated priority alongside maintaining "well-capitalized" status.

Industry Context & Competitive Environment (Analysis)

Regional banking remains intensely competitive with entities ranging from large multi-state banks leveraging broad product suites to fintech disruptors targeting core deposit bases with convenient digital alternatives impacting traditional "stickiness" metrics among community bank customers.

Civista competes via personal interaction anchored deeply within local communities—a classic but effective model whereby relationship managers serve quasi-advisory roles beyond mere transactional relationships—a factor increasingly valued even as digital adoption rises.

Still, pressures remain including:

- Larger institutions’ ability to offer more diverse financial products,

- Potential margin compression from competition,

- Regulatory burden especially related to consumer protection laws highlighted recently by CFPB final rule requiring data portability impacting institutions sized between $3B-$10B assets like Civista introduced between now and April ’28, which may require significant systems investment.

Risks Summary from Filings

Concentration risk is notable due to large shares of commercial real estate loans comprising half the portfolio plus continued reliance on residential mortgages which may be sensitive to economic shifts or housing market downturns affecting borrowers’ creditworthiness [S13][S7].

Integration risk accompanies acquisitions though mitigated by planning detailed in disclosures around Farmers Savings Bank deal with no material adverse impact identified through current post-close periods nor any legal contingencies deemed material presently [N4][S11].

Regulatory compliance risk including cybersecurity vigilance remains paramount given increasing sophistication of cyber threats documented alongside comprehensive layered security defenses applied yet acknowledging potential future breach events could materialize impacting reputation or financials nonetheless [S17].

What To Watch Next (Analysis)

Absent explicit forward guidance contained within filings or recent conference calls ([N1]-[N3]), observers should monitor:

- Execution on FSB integration including realized cost synergies,

- Loan portfolio growth trends particularly across commercial real estate balances,

- Developments around CFPB data sharing rule compliance preparedness,

- Dividend policy adjustments potentially reflecting free cash flow stability or capital deployment priorities,

- Effects of macroeconomic variables such as regional economic health influencing credit quality metrics including allowance for credit losses (~$42M reserves at Dec '25) balance sufficiency against emerging risks [S10],[F1],[S13],

- Any further M&A activity pursued using cash raised mid-2025 from equity issuance.

Conclusion

Civista Bancshares sustains solid operational momentum combining organic credit expansion with accretive opportunities such as the recent Farmers Savings Bank acquisition augmenting an already broad foot-print across three states. Its relationship-based banking model supported by robust liquidity reserves alongside conservative capital management has generated stable earnings improvement culminating in almost $46M net income last fiscal year accompanied by strengthened shareholder equity base above half a billion dollars. The company balances disciplined return-of-capital strategies with prudent reinvestment prioritizing technology upgrades enhancing its long-term competitiveness. Nonetheless concentrated exposure in real estate loans coupled with evolving regulatory requirements represent areas necessitating ongoing vigilance. As of early '26 leadership transition plans also introduce managerial continuity considerations critical for preserving established strategic thrusts amidst an evolving regional banking competitive landscape.

This report is intended solely for informational purposes based on available public disclosures as of early March ’26 without investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments