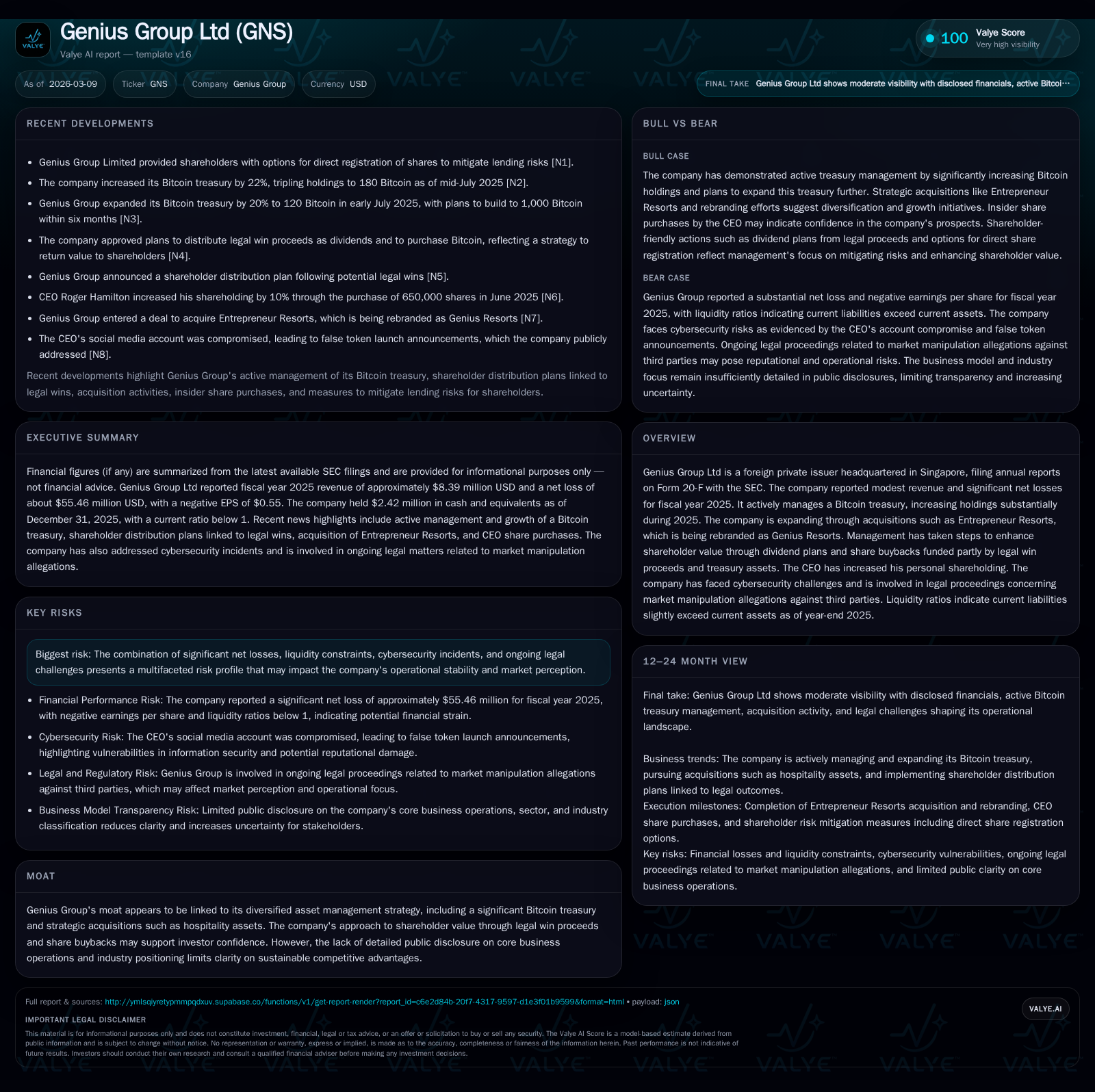

Genius Group's Recruited Growth: Acquisitions, AI-Driven Education, and Hospitality Ventures

Genius Group Ltd pursues expansion through education platform scaling, schooling acquisitions, and strategic hospitality integration despite ongoing net losses and liquidity challenges.

Genius Group Ltd has evolved from a primarily AI-driven Edtech platform provider to a diversified education and experiential hospitality conglomerate by adding schooling services and resort assets in 2025. While revenues grew modestly by about 6% in 2025, net losses deepened significantly, reflecting high operating leverage amid rapid expansion. Management is managing liquidity pressure through bitcoin treasury adjustments, debt paydowns, share buybacks funded partly by legal settlement proceeds, and increased insider shareholding. Ongoing litigation alleging manipulative short selling in the company’s shares alongside cybersecurity vulnerabilities raise operational risks. The firm’s growth hinges on successful integration of recent acquisitions and continued scalable user growth on its GeniusU platform.

Financial Evolution: Historical Growth and Operational Dynamics Through 2025

Genius Group Ltd's revenue trajectory over the past four fiscal years reveals a sharp downturn after a peak in FY2023 followed by modest recovery into FY2025. Specifically, revenue declined from $23.1 million in FY2023 to $7.9 million in FY2024 before rising slightly to $8.39 million in FY2025 — a 6% increase year-over-year [F1]. However, profitability remains elusive as the net loss deepened substantially to $55.46 million in FY2025 from a loss of $24.9 million in the prior year, representing a deterioration of over 122% YoY [F1]. This widening net loss against pared-back revenue highlights significant operating leverage pressures likely tied to integration costs from acquisitions and ongoing investments in technology platforms.

Equity expanded steadily from $13.95 million at end-2022 to $19.7 million at end-2023 and then ramped sharply to $96.6 million by end-2025 reflecting capital injections despite cumulative losses [F1]. The approximate return on equity (ROE) was negative at -57.4% for FY2025 given large reported losses relative to shareholder equity [F1]. The company’s current ratio stood at a concerning 0.86 as of December 31, 2025 with current liabilities ($27.62 million) surpassing current assets ($23.86 million), indicating some liquidity strain possibly due to acquisition-related short-term payables or working capital demands [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 8 | -55 | +6.0% | -122.4% |

| 2024 | 8 | -25 | -65.7% | -336.7% |

| 2023 | 23 | -6 | +26.8% | +89.7% |

| 2022 | 18 | -55 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -57.4 |

| 2024 | -31.4 |

| 2023 | -29.0 |

| 2022 | -395.9 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Summary FY2022–FY2025.

Portfolio Expansion: Strategic Acquisitions Stretching Edtech into Schooling and Resorts

Genius Group's diversification strategy accelerated materially during fiscal year 2025 through pivotal acquisitions fundamentally extending its product offerings beyond online adult entrepreneur education into early childhood schooling and hospitality ventures [S1][S12]. The acquisition of Pro Education Global School in Bali provides the group with physical schooling campuses delivering primary and middle school education integrated with entrepreneurial leadership coursework aligned with Genius Group’s lifelong learning curriculum vision [S1][S12]. This move complements existing digital offerings being scaled via the GeniusU platform.

Concurrently, the group expanded into experiential hospitality through acquiring Entrepreneur Resorts’ portfolio comprising safari lodges in South Africa (Tau Game Lodge and Matla Game Lodge) and villas with café operations in Bali (Vision Villas and Genius Café). These venues host immersive learning environments linking local mentors with global entrepreneurial communities supported digitally by GeniusU’s content ecosystem [S1].

These segments form an internally cohesive model aimed at embedding educational content within tangible networks—an approach potentially conducive to enhancing brand stickiness and driving cross-segment synergies like shared faculty networks and integrated curricula.

Harnessing AI and Entrepreneurship: How Industry Positioning Drives User Growth on GeniusU Platform

At its core still lies the GeniusU platform—a proprietary AI-powered Edtech ecosystem targeting adult entrepreneurs seeking leadership development aligned with emergent technology trends [S1]. The platform benefits from a steady inbound flow of approximately 5,700 new students weekly worldwide throughout calendar year 2024 [S1]. This growth underscores effective digital marketing funnel strategies coupled with scalable content amortization given online delivery dynamics where incremental users cost marginally above fixed platform expenses.

Faculty commissions represent an important cost lever wherein educators delivering online courses receive payments calibrated against course enrollment—indicating a variable cost structure supportive of scalable margins as headcount grows [S1]. This flexible operational expense profile allows Genius Group to increase offerings without proportionate increases in fixed costs.

The company’s emphasis on AI also suggests potential future enhancements such as personalized learning paths or adaptive courseware that could differentiate it within a competitive digital education landscape.

Revenue Streams Dissected: Segmentation of Academy, School, Resorts, and Central Operations

Revenue segmentation elucidates the structural complexity underpinning Genius Group’s diversified business model [S1][F1]:

- Academy Segment: Focuses on adult entrepreneurial education delivered via GeniusU Edtech platform alongside localized Property Investors Network activities primarily in the UK covering property investment courses across multiple city chapters.

- School Segment: Encompasses early childhood through middle school education including Education Angels’ home-based early learning program in New Zealand plus Pro Education campuses acquired recently in Bali providing classroom-based internationally aligned curricula integrating entrepreneurship components.

- Resorts Segment: Generates income from hospitality operations including safari lodges providing accommodation alongside experiential educational programs plus villa rentals and café services supporting community engagement activities.

- Central Segment: Functions chiefly as internal management fee income which is eliminated upon consolidation but bears overhead administrative expenses associated with strategic governance.

- Discontinued Operations: Includes entities under closure or restructuring whose contributions are expected to be immaterial going forward.

Cost structures vary distinctly between segments: the Academy line bears significant digital marketing expenses alongside transactional processing fees reflecting online payment volumes; faculty remuneration constitutes another material expense impacting margin dynamics. Schools incur educator salaries plus real estate maintenance costs including depreciation on right-of-use assets per IFRS lease standards. Resorts naturally carry consumable costs (food/beverage), labor tied directly to client services such as safaris/game drives plus asset depreciation on buildings/equipment critical for service delivery [S1].

Fiscal Pressures: Navigating Net Losses, Liquidity Gaps, and Cybersecurity Challenges

Despite strategic diversification initiatives bolstering revenue streams modestly (+6% YoY), Genius Group is confronted with persistent negative net income trends that widen operational cash burn rates considerably—net losses surged past $55 million for FY2025—a doubling versus prior year losses signalling substantial ongoing leverage costs related to acquisitions integration and platform investment phases [F1][S1].

Liquidity analysis reveals current liabilities slightly outstripping current assets yielding a sub-1x current ratio of approximately .86 as of December 31st 2025 which introduces near-term working capital pressures that management partially mitigates by optimized treasury management practices including Bitcoin sales coupled with debt reduction efforts [F1][S18][S21].

Material weaknesses reported regarding internal control over financial reporting further heighten risk profiles surrounding timely financial disclosures while cybersecurity incidents described raise red flags about operational resilience safeguards—an increasingly critical rating factor given growing digital footprint vulnerabilities amid regulatory scrutiny concerns [S1][S4][S14].

Capital Strategy and Investor Returns: Dividends, Buybacks, Legal Proceedings Windfalls, and CEO’s Stake Uptick

Capital deployment policies reveal proactive measures intended to enhance shareholder value amidst volatile operating results [S8][S11][S17][S20]:

- The Company strategically monetized ~96 Bitcoins between late December '25 and early Feb '26 at average prices near $73k generating gross proceeds of ~$7 million utilized primarily for Bitcoin-backed loan reduction—from $8.5M outstanding down to ~$3.3M—improving balance sheet flexibility while maintaining prudent leverage levels considering absence of other bank debts [S8][S16].

- Concurrently executing share repurchases funded partly through legal settlement proceeds linked to ongoing litigation concerning market manipulation claims against third parties reflects calculated capital return efforts aimed at supporting stock price stability.

- Dividend plans have been introduced reflecting maturing cash flow expectations although explicit declared amounts remain unavailable requiring monitoring for future disclosure updates.

- CEO Roger Hamilton increased his personal stake signaling insider confidence aligned with shareholder interests during volatile trading periods marked by alleged external short-selling abuses.[S11][S20]

These capital moves are framed within a longer-term view balancing opportunistic asset monetization with acquisitions funding while optimizing free cash flow deployment for both operational improvement initiatives as well as market confidence restoration.

Risk Exposure and Legal Hurdles Impacting Stability and Perception

A significant overhang involves complex litigation alleging systematic spoofing and naked short selling predominantly attributed to high-frequency trading entities Citadel Securities LLC and Virtu Americas LLC spanning April 12th 2022 through May 30th 2025—trading days exhibiting manipulative patterns on nearly all sessions analyzed causing artificial price depressions detrimental to Genius stock valuation [S4][S5][S6][S7][S9][S10][S14].

The complaint articulates purported violations of Regulation SHO alongside Rule10b-5 asserting these practices misrepresented supply/demand fundamentals contributing materially to deflated market pricing thereby negatively impacting shareholders who traded during this period.

Compounding reputational risks are disclosures around inadequate supervisory systems by defendants enabling such manipulative conduct along with internal control deficiencies identified within the company's own reporting environment fostering compliance risk considerations.

Cybersecurity incidents disclosed further accentuate risk exposure profiles requiring enhancements in risk event impact mitigation—critical areas especially relevant given heavy reliance on digital platforms spanning multiple geographies.

Collectively these factors impose cautionary overlays on operational continuity assumptions under regulatory scrutiny paired with heightened investor uncertainty.

Future Outlook: What Fiscal 2026 May Hold for Expansion Milestones and Profitability Inflection

Looking ahead into fiscal year 2026 the company’s ramped acquisition strategy sets foundational building blocks whereby successful integration of Pro Education campuses into Genius School paradigms alongside full rebranding/operational rollout of Entrepreneur Resorts as Genius Resorts remain key milestones for assessment benchmarking growth execution capabilities beyond pure organic user base expansion on GeniusU platform currently averaging thousands of new enrollments weekly globally [S2][S3].

Further potential exists leveraging technology-enabled delivery innovation encompassing AI-driven customized learning experiences designed to accelerate engagement metrics sustaining higher margin trajectories long-term.

Near-term constraints may persist stemming from continuing net losses compounded by macroeconomic conditions affecting discretionary educational/hospitality spending patterns.

Market watchers should observe developments around regulatory outcomes relating to ongoing litigation plus efficacy of treasury optimization strategies balancing Bitcoin asset holdings against debt/capital needs as well as monitoring progress toward positive EBITDA achievement targets previously communicated.

This analysis solely synthesizes publicly filed information without offering investment recommendations or forecasts beyond documented facts or clearly labeled forward-looking interpretations specific to Genius Group Ltd's operational narratives as of their latest filings dated March 9th, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments