Custom Truck One Source Rebounds Revenue Above $1.9 Billion Despite Net Losses

CTOS delivered top-line growth near $1.94 billion in fiscal 2025 while grappling with a net loss and navigating cash flow improvements amidst operational pressures.

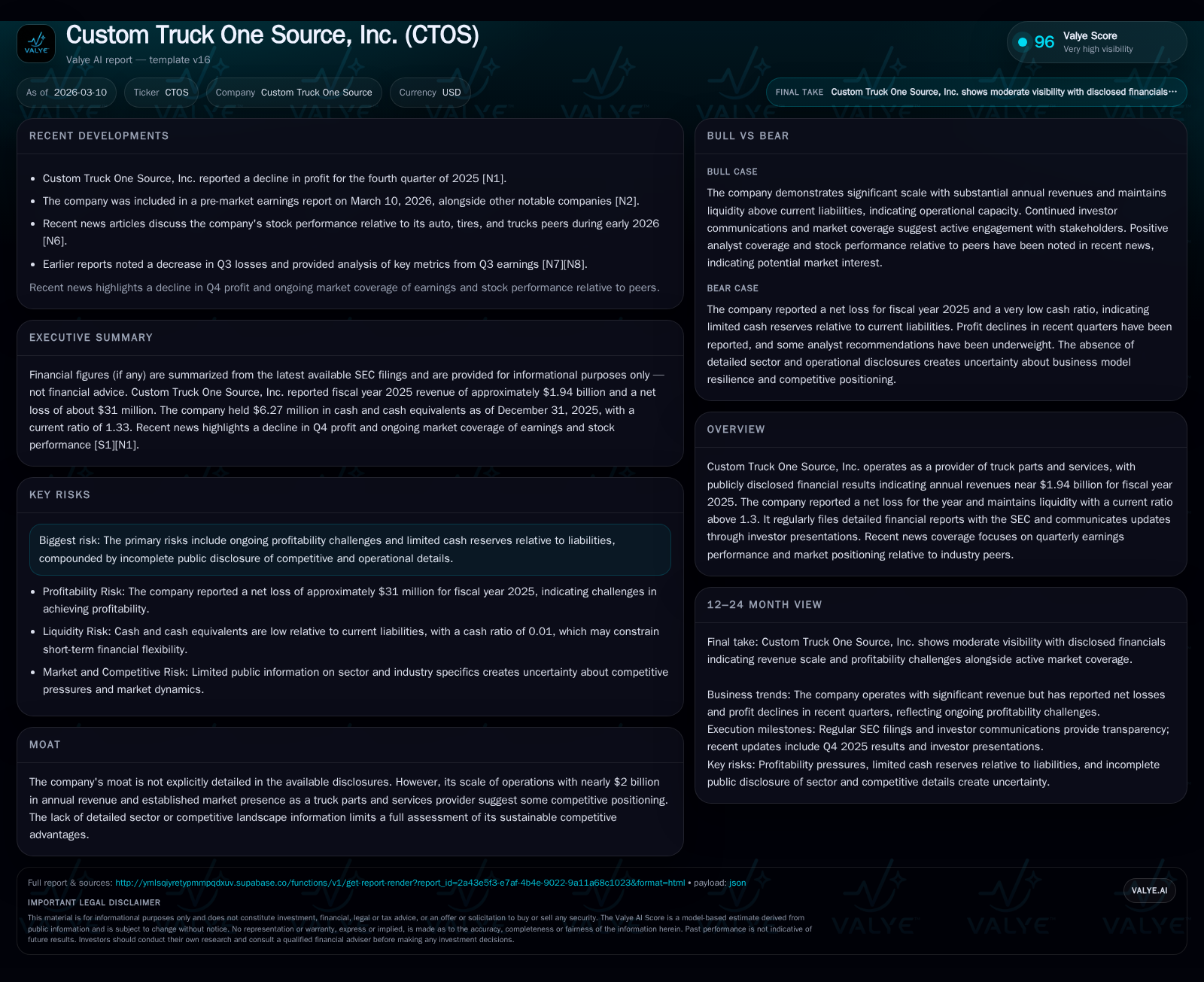

Custom Truck One Source, Inc. reported a 7.9% revenue increase for fiscal year 2025 reaching nearly $1.94 billion, driven by sustained demand in truck parts and services. Operating income declined slightly by 1.1%, and the company recorded a net loss of $31 million, reflecting margin pressures and non-operating costs. Improved working capital management fueled a 154% surge in operating cash flow, enabling robust free cash flow generation despite weak earnings. Capital allocation was cautious, with share repurchases increasing moderately and capex remaining low. Liquidity metrics remain stable but highlight limited cash reserves relative to liabilities, underscoring ongoing financial risks amid sector uncertainties.

Revenue Surge in Fiscal 2025: Growth Drivers and Historical Context

Custom Truck One Source posted revenues of approximately $1.94 billion for fiscal year 2025, representing a 7.9% increase from $1.80 billion in the prior year [F1]. This rebound follows a dip in FY24 and reflects sustained demand across its truck parts and service offerings amid favorable industry conditions. The historical revenue trend shows fluctuations with revenues of $1.87 billion in FY23 falling to $1.80 billion in FY24 before the recent uptick [F1]. This suggests CTOS has regained market traction after uneven periods.

Profitability Under Pressure Amid Net Loss Persistence

Operating income declined slightly by 1.1% from about $126 million in FY24 to roughly $125 million in FY25, indicating margin compression possibly due to higher input costs or logistics expenses affecting profitability [F1]. Despite positive operating earnings, the company reported a net loss of approximately $31 million compared to a loss of around $28.6 million the prior year [F1]. This divergence points to non-operating charges such as financing costs or impairments impacting the bottom line as detailed in risk disclosures [S4][S5].

Cash Flow Strength: Operating Cash Flow and Free Cash Flow Expansion

Operating cash flow increased significantly by over 154%, reaching approximately $310 million versus about $122 million in FY24 [F1]. This improvement is largely attributed to better working capital management enhancing cash conversion cycles. Capital expenditures remained low at just over $1 million, yielding free cash flow near $309 million—highlighting strong cash generation despite net losses [F1].

Capital Allocation: Buybacks Increase While Dividends Remain Undeclared

The company’s capital allocation strategy appears conservative; share repurchases rose modestly to approximately $32.6 million from around $29 million the previous year [F1]. No dividends were declared according to filings and investor communications, signaling a focus on liquidity preservation and operational stability over direct shareholder payouts currently [S11][S15][S16].

Liquidity Profile: Balance Sheet Highlights and Risks

Liquidity metrics show a current ratio of about 1.33 with current assets near $1.16 billion against current liabilities around $873 million as of December 31, 2025 [F1]. However, cash and equivalents stand at only about $6.3 million, indicating limited immediate liquidity despite overall working capital coverage [F1]. Equity was approximately $809 million for the period but has declined over recent years [F1]. Risk disclosures note potential refinancing needs and covenant considerations amid market conditions that could affect financial flexibility [S8][S10][S13].

Outlook and Risk Considerations

No formal forward guidance has been issued recently by CTOS; thus, analytical focus rests on operational metrics like margin recovery efforts and sustained free cash flow generation as indicators of financial health going forward [N4][S3]. Key risks highlighted include earnings volatility tied to input cost fluctuations, tight liquidity buffers increasing refinancing risks, and limited visibility into competitive dynamics within the sector [S4][S5][S7]. The absence of detailed competitor data or strategic outlooks adds uncertainty around future performance.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1944 | -31 | 310 | 125 | +7.9% | -8.4% |

| 2024 | 1802 | -29 | 122 | 126 | -3.4% | -156.5% |

| 2023 | 1865 | 51 | -31 | 171 | +18.6% | +30.3% |

| 2022 | 1573 | 39 | 46 | 103 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 33 | 309 | -3.8 |

| 2024 | 29 | 121 | -3.3 |

| 2023 | 39 | -33 | 5.5 |

| 2022 | 10 | 46 | 4.4 |

Source: SEC companyfacts cache [F1].

Table shows annual financial performance with percentage changes where available; capital expenditures remain modest relative to revenue scale.

This analysis is based strictly on official SEC filings combined with recent news reports without extrapolation beyond documented facts concerning Custom Truck One Source’s financial condition through early-2026.

Disclaimer: This report is presented solely for informational purposes without investment advice; readers should consult primary filings and qualified advisors before making investment decisions related to CTOS.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments