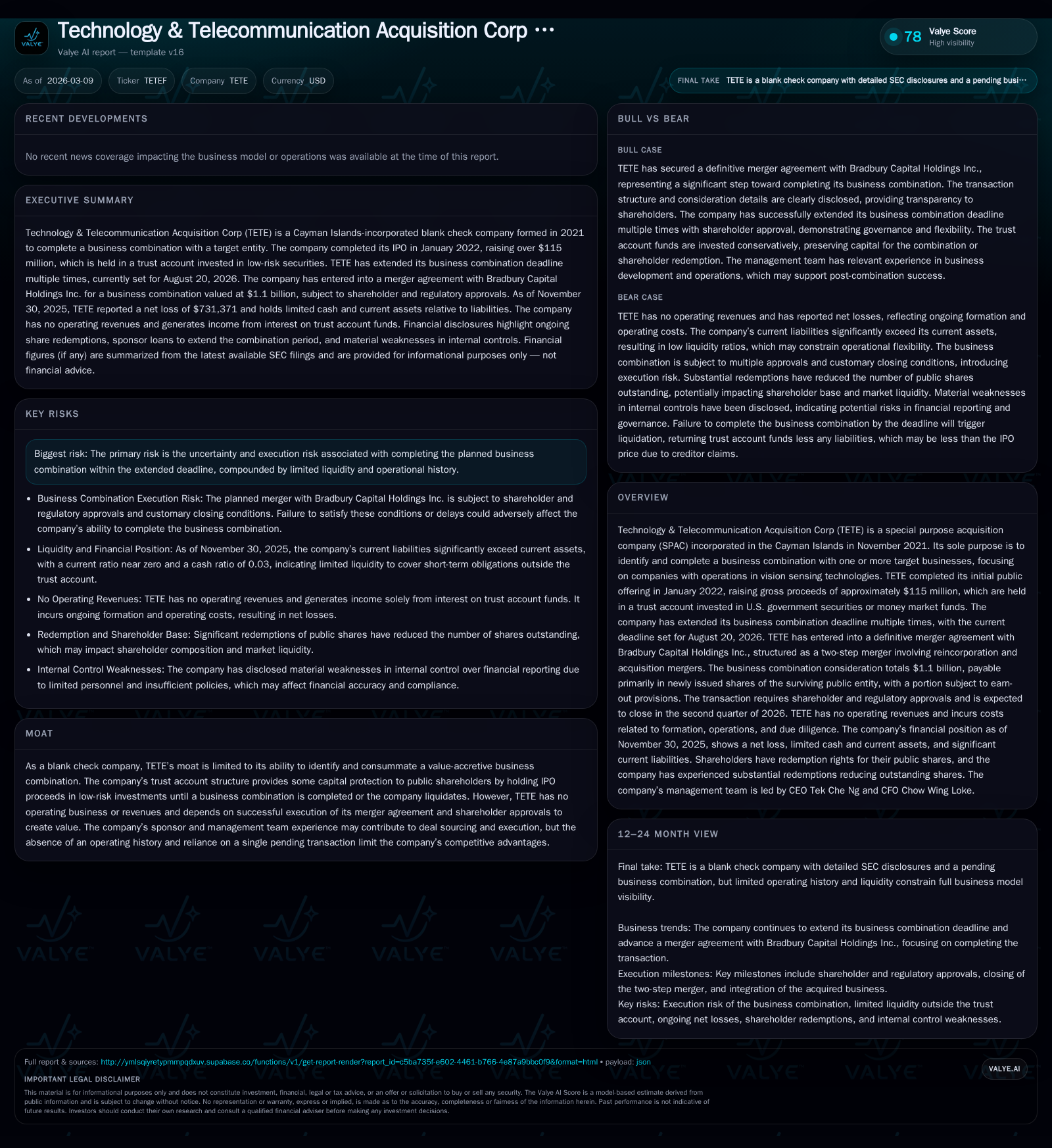

Technology & Telecommunication Acquisition Corp’s Value Hinges on Bradbury Capital Merger Execution

As a special purpose acquisition company, TETEF’s future depends entirely on closing its $1.1 billion business combination with Bradbury Capital.

Technology & Telecommunication Acquisition Corp (TETEF), a Cayman Islands-incorporated SPAC focused on vision sensing technologies, completed its IPO in January 2022 raising approximately $115 million placed in a trust account. The company has extended its deadline multiple times to consummate a business combination, currently set for August 20, 2026. Its sole significant activity is an announced two-step merger agreement with Bradbury Capital Holdings Inc., valued at $1.1 billion. With no operating revenues or business history, TETEF's value creation rests on successful deal closure and shareholder approvals amid shareholder redemptions and execution risks. The company shows sustained losses from ongoing operations as it prepares for the merger.

Company Background and Structure

Technology & Telecommunication Acquisition Corp (TETEF) was incorporated in the Cayman Islands on November 8, 2021, as a special purpose acquisition company (SPAC) targeting businesses primarily in vision sensing technology [S1]. The company completed its initial public offering (IPO) in January 2022, issuing units comprising one ordinary share and redeemable warrants, generating gross proceeds of approximately $115 million including overallotments and private placements [S1][S12]. These funds are held predominantly in U.S. government securities or money market funds within a trust account until the completion of a business combination or liquidation [S1][S12].

Historical Performance and Financial Summary

TETEF operates without an active business or revenues; its financial performance reflects only organizational expenses and costs associated with pursuing a business combination. Over the past four fiscal years through November 30, 2025, the company reported negative operating income worsening slightly year-over-year by about 6.9%, reflecting elevated costs [F1]. Net income turned sharply negative in FY2025 compared to prior years with fluctuations largely attributable to accounting adjustments related to share redemptions rather than operational factors [F1]. Operating cash flow remained negative annually but improved by roughly 53% year-over-year due to reduced expenses and lower cash consumption [F1]. Equity has steadily eroded resulting from accumulated losses.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -731371 | -342483 | -1131512 | -218.5% |

| 2024 | 617298 | -731569 | -1058411 | +243.7% |

| 2023 | 179619 | -781376 | -1844452 | -78.3% |

| 2022 | 826045 | -400965 | -500952 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 7.0 |

| 2024 | -6.6 |

| 2023 | -2.5 |

| 2022 | -22.7 |

Source: SEC companyfacts cache [F1].

Note: All figures sourced from latest SEC filings [F1].

Trust Account and Shareholder Redemptions

At IPO close in January 2022, approximately $116.7 million were placed into the trust account to safeguard shareholder capital [S12][S13]. Since then, substantial redemptions by public shareholders have reduced the balance significantly—from over $31 million earlier to just over $142 thousand as of November 30, 2025—reflecting distributions upon shareholder exercises of redemption rights when extension proposals were put forth [S12][S18][S25]. Redemption prices have ranged around $10–$13 per share depending on timing [S5][S10][S19]. At various points between early 2023 and early 2026,the company obtained sponsor-backed promissory loans totaling around $4.2 million interest-free to cover working capital needs and extension fees required for prolonging the business combination deadline beyond original limits [S6][S16].

Business Combination Agreement with Bradbury Capital

The core strategic development is an amended definitive merger agreement signed on August 2, 2023 that contemplates TETEF merging through a two-step transaction into Bradbury Capital Holdings Inc., a Cayman Islands exempted company valued at an aggregate consideration of $1.1 billion [S1][S4][S5]. This deal comprises:

- A reincorporation merger where TETEF merges into its subsidiary PubCo which remains public.

- An acquisition merger where PubCo’s wholly owned subsidiary merges into Bradbury Capital Holdings making it a wholly owned subsidiary.

Consideration consists of newly issued PubCo ordinary shares valued at $10 each. About $235 million will be paid at closing with the remaining balance subject to earn-out provisions under the merger agreement [S1][S4]. Existing shares held by Bradbury shareholders will be canceled upon closing in exchange for PubCo shares; additionally a portion (10%) of shares issued will be held in escrow against indemnification liabilities [S1][S4]. The transaction requires customary regulatory approvals including SEC proxy clearance as well as shareholder approval from both TETEF and Bradbury Capital [S1]. The deal is expected to close during Q2 2026 pending fulfillment of these conditions [S1][S4].

Future Growth Prospects and Risks

Value creation for TETEF hinges entirely on successfully completing this merger within the extended deadline of August 20, 2026. Failure would trigger liquidation and return of remaining trust funds minus any liabilities and costs [S13]. Given TETEF's lack of operational history or revenue streams—the projected post-merger entity’s financial prospects depend heavily on Bradbury Capital’s underlying vision sensing technology businesses subject to further disclosure post-close.

Execution risks include obtaining all necessary shareholder votes for approval amid ongoing redemptions that dilute public float and increase uncertainty [S5][S9][S21]. The sponsor’s commitment demonstrated through financial extensions likely improves odds but cannot eliminate closing risks including due diligence findings or regulatory impediments.

Additionally,TETEF faces liquidity constraints having exhausted most trust account balance due to redemptions—increased dependence on sponsor loans adds counterparty risk though loans are unsecured and repayable only after closing [S6][S16]. Any claims from creditors could diminish amounts available for distribution to public shareholders upon liquidation if deal fails [S20]. These factors elevate inherent SPAC risks related more broadly to timing extensions’ impact on investor confidence.

Capital Allocation and Shareholder Returns

As a blank check entity,TETEF pays no dividends,generates no operational cash flows,and consumes capital mostly through administrative expenses. Required extension fees reduce amounts held in trust thereby lowering balances available for redemption or distribution [S12][S19]. Share repurchases did not occur outside redemption requests;the Sponsor holds founder shares without redemption rights which may be forfeited or converted per negotiated terms tied to investor non-redemption agreements previously executed but now terminated following approvals[S8][S21].

Return measures such as ROE are not meaningful given continuous losses pre-merger;as of FY2025 TETEF showed negative equity reflecting cumulative deficit from operating losses and redemptions exceeding capital raised[F1].

Operational Overview

TETEF operates with minimal staff—consisting primarily of executive officers facilitating governance,and administrative functions provided under agreements with affiliated Technology & Telecommunication LLC which charges a monthly fee for office space utilities,and secretarial support[S6][S20]. This outsourcing model aligns with typical SPAC structures focused solely on deal-making activities prior to any acquisition closing.

Summary and Outlook

Technology & Telecommunication Acquisition Corp’s current valuation is exclusively linked to its pending acquisition of Bradbury Capital Holdings Inc., a transaction valued at $1.1 billion planned for completion within six months. Absent operational activity or revenues,this transaction represents both the company's highest opportunity for value realization and principal source of risk linked to timing extensions,long-running shareholder redemptions,and deal execution uncertainty.

Financially,TETEF reflects typical SPAC characteristics: increasing net losses driven by administrative costs,reductions in public share count due to widespread redemptions,and diminishing trust account balances offset partially by sponsor loans supporting working capital needs.The pending two-step merger represents the critical catalyst that will define whether TETEF transitions from a shell vehicle into an operating enterprise centered on vision sensing technologies.

Investors should monitor:

- Progress toward satisfying closing conditions for the Bradbury Capital merger,

- Shareholder vote outcomes given redemption activity,

- Regulatory filings including proxy statement disclosures detailing acquired business prospects,

- Updated financial statements post-business combination reflecting operating performance,

- Sponsor financing arrangements affecting balance sheet leverage after closing.

Given the SPAC nature,this entity lacks standalone valuation metrics typical of operating companies,but merits attention as part of broader technological consolidation trends within sensor technology fields where SPACs have actively sought deals recently.A successful close could position TETEF (reincorporated as PubCo) as a platform entity subject to strategic growth dependent on post-merger integration outcomes.

Disclaimer: This analysis summarizes publicly disclosed information regarding Technology & Telecommunication Acquisition Corp as of March 9, 2026 based on SEC filings and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments