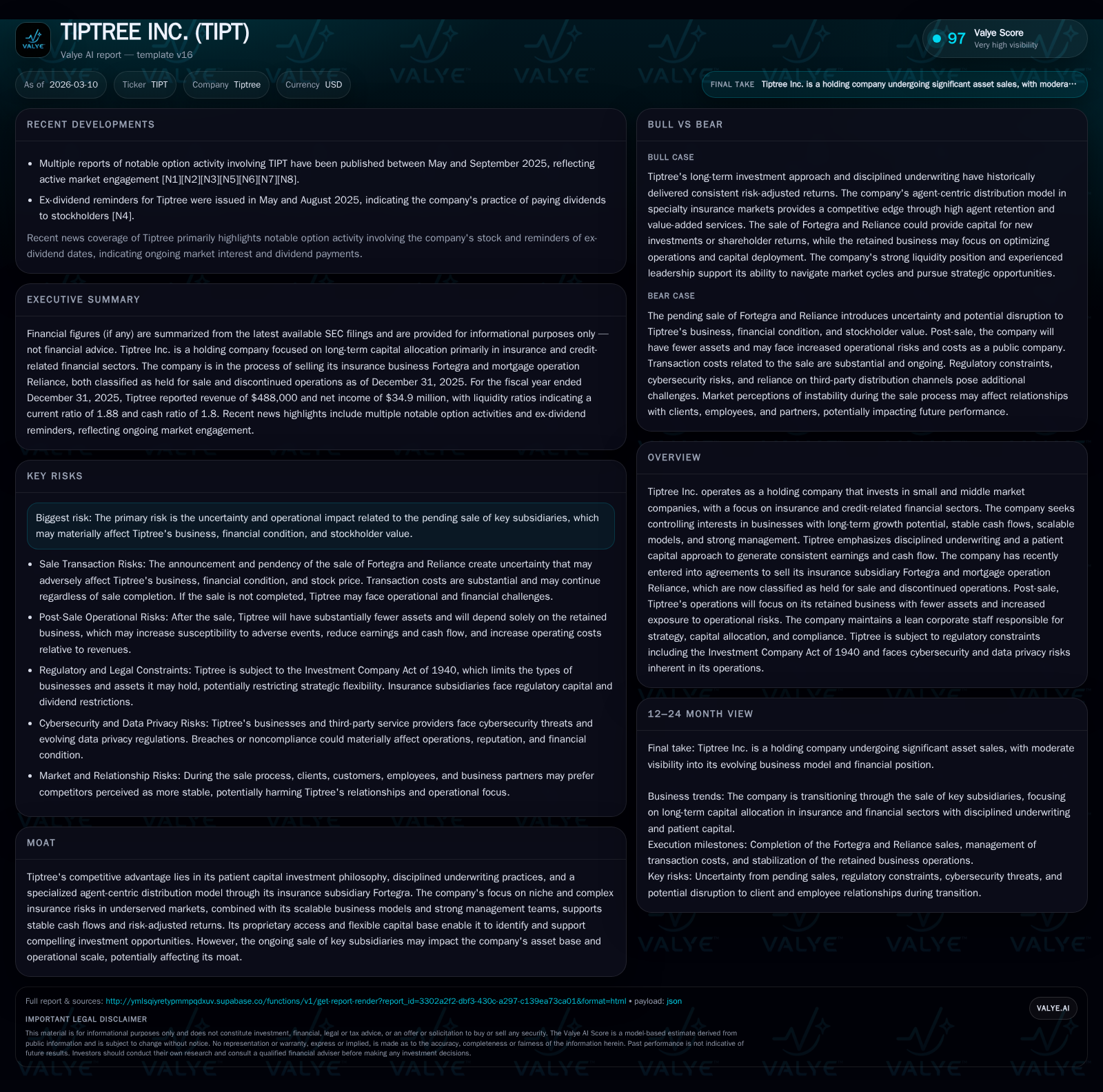

Tiptree Inc. Transitions: Evaluating Strategic Asset Sales and Returning to Core Holdings

Tiptree’s sale of major subsidiaries reshapes its operational scale, financial profile, and risk landscape as it refocuses on a leaner retained business.

Tiptree Inc. has undertaken a transformative pivot by divesting its largest insurance subsidiary Fortegra and mortgage operation Reliance, marking a significant shift away from its historically diversified financial services holdings. This strategic repositioning substantially reduces its asset base and revenue streams but frees considerable capital—proceeds estimated at $1.7 billion—to redeploy or return to shareholders. While the retained operations exhibit stable cash flow generation and modest profitability, the loss of scale introduces greater operational risk and heightened sensitivity to market fluctuations, all under the constraints of regulatory oversight including the Investment Company Act exemption. Future growth and returns hinge critically on management’s capital allocation discipline and ability to navigate a narrower business footprint.

Historical Growth Fuelled by Diverse Financial Services Holdings

Until recently, Tiptree Inc.'s growth was anchored in its controlling investments across small and middle market companies primarily focused within the insurance and credit-related financial sectors. The company's historically diversified operations included the specialty insurance subsidiary Fortegra and mortgage originations through Reliance First Capital. These businesses drove top-line growth from approximately $1.4 billion in FY2022 to over $2 billion in FY2024 per companyfacts data [F1]. This expansion aligned with Tiptree's patient capital philosophy targeting long-term earnings stability through underwriting discipline and scalable niche business models.

Despite robust revenue growth during this period, Tiptree’s net income exhibited volatility: turning positive in FY2023 after losses in FY2022 ($-8.3 million) before peaking at ~$53 million in FY2024 [F1]. Operating cash flow similarly showed uneven trends but remained significantly positive reflecting continued underlying cash generation capabilities.

The FY2025 financials reveal stark transition effects—the top-line collapsed to just $488 thousand due to Fortegra and Reliance being reclassified as held-for-sale and discontinued operations following agreements execution late 2025 [F1][S1][S3]. However, net income stayed healthy at $34.9 million reflecting earnings from retained businesses along with sale-related items. Operating cash flow remained strong at $168 million despite the sharp cut in revenue, underscoring leaner ongoing operations without capital expenditure requirements that year [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0.0 | 35 | 168 | 0 | -100.0% | -34.6% |

| 2024 | 2.0 | 53 | 241 | 4 | +23.9% | +282.5% |

| 2023 | 1.6 | 14 | 71 | 14 | +18.0% | +268.6% |

| 2022 | 1.4 | -8 | 463 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 168 | 6.9 | |

| 2024 | 0 | 237 | 11.7 |

| 2023 | 0 | 57 | 3.3 |

| 2022 | 1727000 | 452 | -2.1 |

Source: SEC companyfacts cache [F1].

Reflects dramatic revenue decline due to sale/discontinuance classification; retained operations maintain positive net income; CFO remains robust despite capex cessation.

Strategic Sale of Fortegra and Reliance: Implications for Scale and Earnings

A pivotal moment arrived in September 2025 when Tiptree executed a sale agreement transferring ownership of Fortegra for aggregate consideration of approximately $1.65 billion in cash subject to customary adjustments [S1]. This subsidiary had been central to Tiptree's insurance segment with a specialized agent-centric distribution model focusing on niche excess & surplus risks coupled with disciplined underwriting—a model praised for aligning distributor incentives with underwriting performance [S19]. Coincidentally in October 2025 came the disposition of Reliance First Capital for an amount estimated near $50 million based on tangible book value metrics [S3][S12]. Both these transactions shifted their respective assets into held-for-sale classification on the balance sheet as of December 31st.

While divesting these key subsidiaries substantially shrinks Tiptree’s operational scale and dramatically lowers consolidated revenue levels in reported results going forward (~zero revenues from discontinued), it releases substantial liquidity enabling strategic flexibility [S1][S3]. However significant transaction costs were incurred and inherent risks remain relating to final sales completion timelines and use-of-proceeds discretion spelled out in risk disclosures ([S1]). Post-sale earnings will exclusively arise from retained businesses which are comparatively modest but generate consistent positive cash flows.

Navigating Capital Allocation Post-Divestiture

The influx of ~$1.7 billion cash positions Tiptree at a crossroads on capital allocation strategy[S1,S12]. Despite strong historical operating cash flows (e.g., $168 million CFO in FY25), recent years show no share repurchases activity noting zero buybacks since at least FY23 per filings[F1], suggesting board prudence amid transition. The dividend stance is similarly conservative; no special dividends connected with sale proceeds have been declared though regular dividend payments continue[S12].

Equity capital expanded moderately reflecting retained earnings accumulation alongside asset sales (equity grew from $397 million in FY22 to $508 million in FY25)[F1], underpinning an approximate trailing twelve months ROE near ~7%, indicative of profitable core unit economics albeit on diminished asset size.

Going forward efficient redeployment or shareholder returns will be paramount factors shaping investor perception given lack of explicit guidance reported[S12]. The company emphasizes allocating capital towards existing portfolio enhancement balanced against market opportunities and disciplined underwriting practices—core tenets framing anticipated capital use.

Projected Growth and Emerging Risks in the Retained Business

Absent formal forecasts or guidance following divestitures[ N/A], future growth potential rests predominantly within the retained portfolio segment(s). The inherent challenge is concentration risk given far fewer assets elevate sensitivity to adverse shocks [S1]. Regulatory strictures related to maintaining its Investment Company Act exemption curtail Tiptree’s capacity to broaden investment types or materially expand via acquisitions limiting upside optionality[S1,S5,S18,S24].

Moreover operating risks escalate around underwriting complexity without scale synergies previously enjoyed—heightened exposure exists regarding insurance claims variability post-sale alongside reliance on external distribution channels whose effectiveness can fluctuate[S5,S19,S27]. Cybersecurity threats remain salient given increasing dependence on information systems both internally and via third-party service providers[S6,S17,S20,S28]. Legal/regulatory frameworks pertaining particularly to privacy laws like CCPA/GDPR impose further compliance burdens with potential fines or sanctions affecting profitability.[S6,S21,S26]

Collectively risk disclosures embed cautionary notes about unpredictable regulatory evolution possibly limiting product offerings or requiring new operational investments dampening growth prospects absent breakthrough initiatives. Managers face notable execution challenges reconciling leveraging limited scale against maintaining underwriting discipline foundational to past success.

Financial Metrics Through Transition: Profitability, Cash Flow, and ROE Trends

(Refer Table Above for summarized financials)

Despite the seismic revenue contraction caused by divestiture accounting treatment from >$2 billion down below half a million dollars by FY25 end,[F1] net income preserved integrity positing above $34 million illustrates resilient retained business economics plus transaction-related gains/losses inclusion.[F1] Operating cash flow trends downward yet remains robust ($168 million vs prior year’s $241 million) signaling lean cost structure post-capital expenditure halt ([F1]).

Equity increments reflect cumulative earnings retention alongside asset rationalization resulting in reported ROE near seven percent—modest but affirming profitable core operations amid transition.[F1]

Regulatory Constraints and Their Operational Impact

Tiptree operates as a holding company subject notably to exemptions under the Investment Company Act of 1940 that impose substantive limits on business scope including the nature of assets it may hold or acquire.[S1] These restrictions necessitate a cautious approach limiting aggressive expansion into sectors outside approved mandates or undertaking large-scale mergers/acquisitions without risking exemption loss.[S5,S18]

Moreover regulatory demands stemming from extensive insurance industry oversight at state levels enforce stringent statutory capital/reserve requirements that fluctuate based on market conditions impacting subsidiaries still owned.[S6,S13]

Data governance mandates such as GDPR/CCPA combined with evolving cybersecurity law add compliance complexity elevating operating costs materially impacting margins.[S21,S26]

Tiptree thus faces structural headwinds navigating operational optimization while remaining compliant within these layered regulatory frameworks potentially slowing strategic pivots.[S24]

Operational Risks After Shedding Key Insurance Subsidiaries

With Fortegra exit realities include a concentrated risk profile reliant upon fewer asset pools increasing susceptibility to adverse events including underwriting volatility or claims surges absent diversification buffer formerly provided.[S5]

Cybersecurity vulnerabilities compound operational risks given reliance on both internal IT systems plus outsourced service providers whose failure could disrupt business functions impacting claims processing or customer interaction adversely.[S6,S17,S20]

Furthermore dependency on independent agents/brokers for distribution exposes residual insurance offerings to channel attrition risk where partner consolidation or shifting sands could degrade revenue streams sharply if distributor relations deteriorate or lose effectiveness.[S19,S27]

Intellectual property protection alongside legal/regulatory litigation exposure add further layers weighing upon reputational resilience important for sustaining stakeholder confidence post-divestiture phase.[S7,S8]

What to Watch: Market Response, Strategic Deployments, and Regulatory Developments

Looking ahead stakeholders should focus intensely on how management deploys freed liquidity from sales proceeds—timing of reinvestments versus returning capital could signal confidence levels around retained businesses' potential.

Surveillance of quarterly earnings for signs of stabilized or improved performance within narrower operations will provide early cues on adjustment efficacy.

Regulatory developments influencing permissible activities under the Investment Company Act exemption or insurance industry compliance requirements bear watching as they could dictate flexibility limits affecting strategic options.

Lastly shareholder returns policy evolution—dividends trajectory or initiation of share repurchases—may shape market perception concerning capital allocation efficiency under new corporate scale dynamics.

This analysis is based solely upon publicly filed documents as of March 10th, 2026 and does not incorporate any non-public information or speculative projections beyond evidenced disclosures. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments