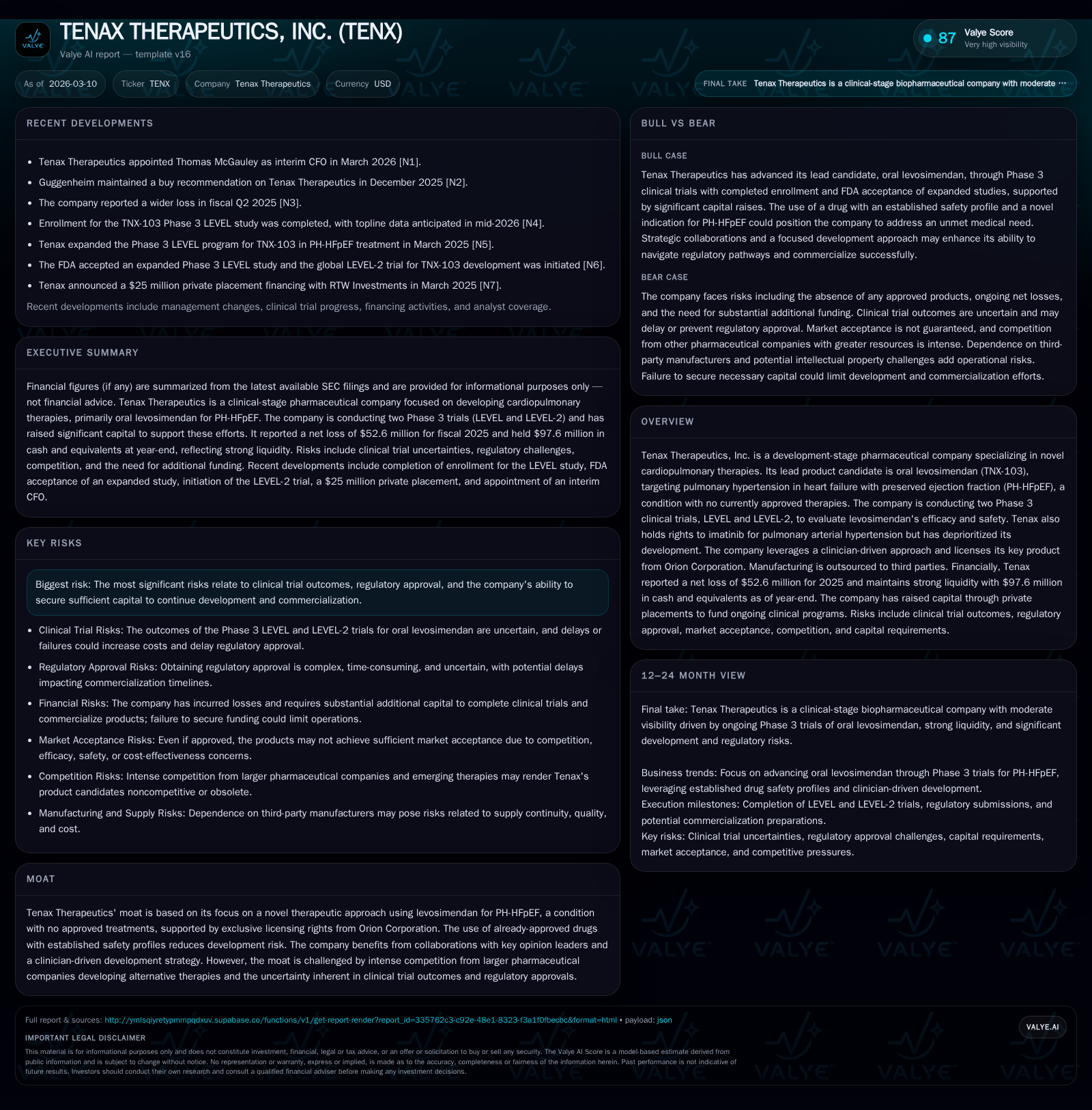

Tenax Therapeutics' Strategic Focus on PH-HFpEF Shapes Financial Trajectory and Clinical Milestones

Tenax Therapeutics advances its oral levosimendan program targeting PH-HFpEF amid escalating R&D expenditure and robust liquidity.

Tenax Therapeutics centers its clinical development efforts on oral levosimendan (TNX-103) for pulmonary hypertension associated with heart failure with preserved ejection fraction (PH-HFpEF), an indication without approved therapies. The company faces intensifying investment demands reflected in widening net losses, reaching $52.6 million in 2025, driven by two ongoing Phase 3 trials, LEVEL and LEVEL-2. Despite the elevated burn rate, Tenax sustains a strong liquidity position with $97.6 million in cash at year-end 2025 and continued capital raises. The uncertain outcomes of late-stage clinical programs, regulatory hurdles, and a competitive landscape constitute significant risk factors, underscoring the critical importance of upcoming clinical milestones.

Operating History: From Modest Beginnings to Escalating R&D Investment

Since at least FY2016, Tenax Therapeutics has reported negligible revenues—zero reported as recently as the end of that year—and operated as a development-stage pharmaceutical company focused primarily on cardiopulmonary therapeutic innovations [F1]. This absence of commercial product sales characterizes its financial narrative through to FY2025.

Net losses have deepened dramatically in recent years. Operating income swung from a positive figure in FY2023 (+$8.2 million) to progressively negative levels, ultimately reaching -$56.4 million in FY2025—a deterioration exceeding 189% year-over-year—the net income metric follows suit with losses scaling almost threefold from -$17.6 million to -$52.6 million over the same period [F1]. The worsening loss profile corresponds directly to escalated investment in late-stage clinical trials evaluating oral levosimendan (TNX-103) for pulmonary hypertension linked with heart failure with preserved ejection fraction (PH-HFpEF).

Operating cash flow deteriorated by over 140% to negative $35.8 million in FY2025 amid these higher R&D outlays; capital expenditures remained immaterial throughout this timeline aligning with standard biotech patterns emphasizing trial spending over fixed asset investment [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -53 | -36 | -56 | -198.8% |

| 2024 | -18 | -15 | -19 | -328.3% |

| 2023 | 8 | -6 | 8 | +169.8% |

| 2022 | -11 | -12 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -54.2 |

| 2024 | -19.1 |

| 2023 | 95.2 |

| 2022 | -740.1 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Overview shows Tenax’s continued zero top-line offset by escalating operating losses aligned with intensified Phase 3 trial investments.

Clinical Development Milestones Driving Current Valuation Focus

Tenax’s lead therapeutic thrust resides in oral levosimendan (TNX-103), licensed exclusively from Orion Corporation. Levosimendan is under investigation in two ongoing Phase 3 randomized controlled trials — LEVEL and LEVEL-2 — aimed at the treatment of PH-HFpEF [N1; S1; S4; S6; S9]. These trials explore an indication characterized by high unmet medical need; currently there are no FDA-approved therapies specifically for PH-HFpEF.

The LEVEL study evaluates efficacy endpoints targeting improvements in hemodynamic parameters and exercise capacity while monitoring safety signals rigorously. LEVEL-2 recently initiated enrollment in late 2025 seeks to expand validating evidence under similar protocols [S1; S4]. Both studies are extensive and cost-intensive endeavors reflective of their pivotal role as potential registration-enabling trials.

In parallel, Tenax holds rights to imatinib (TNX-201), previously considered for pulmonary arterial hypertension (PAH). However, this program has been deprioritized as resources concentrate on levosimendan advancement due to its higher strategic priority and promising preliminary data [S1; S24; S25].

The company engages leading cardiovascular clinicians to guide trial design and execution strategies—a tactic aimed at enhancing scientific rigor and increasing eventual market adoption potential [S26]. Nonetheless substantial uncertainty remains around trial outcomes due to factors like patient recruitment rates and endpoint variability which may impact final data interpretation or delay regulatory reviews [S4; S6].

Market Potential and Challenges in PH-HFpEF Therapeutics

Pulmonary hypertension linked with heart failure with preserved ejection fraction affects an estimated patient population exceeding one million individuals within the U.S., likely underreported due to diagnostic challenges including reliance on invasive catheterization techniques [S24]. The absence of any approved pharmacotherapies places Tenax’s oral levosimendan candidate at a potentially transformative position.

However considerable market entry barriers exist. Successful therapy adoption will depend heavily on demonstrating clinically meaningful efficacy coupled with favorable safety profiles compared to off-label or non-specific treatments currently prescribed despite lack of formal approval [S9; S28]. Pricing strategy will require balancing competitive pressures including low-cost generic compounds exhibiting partial overlapping mechanisms and emerging novel agents under mid-phase evaluation by larger pharma players [S28].

Reimbursement uncertainty adds complexity against backdrop of increasing scrutiny on orphan drug designation benefits and payor policies affecting drug access [S28]. Additionally prescriber willingness to shift entrenched practice patterns toward novel oral therapies will be tested particularly given historical failures or safety concerns with some pulmonary vasodilators used off-label [S9; S28]. Patient convenience favoring oral administration aids acceptance prospects but requires substantiation during clinical program completion.

Capital Structure, Financing Events, and Liquidity Positioning

As of December 31, 2025 Tenax held cash and equivalents amounting to $97.6 million complemented by total current assets around $104.2 million against modest current liabilities approximating $7.2 million—yielding an exceptionally strong current ratio of approximately 14.56 that positions the company well against short-term liquidity risks [F1; S12; S27].

Funding initiatives underpinning this cash reserve include sizable private placement rounds completed during August 2024 followed by a March 2025 offering generating proceeds intended explicitly for advancing Phase 3 development [S26]. In early March 2026 an additional ~$14.5 million was secured via warrant exercises adding further financial runway post-year-end [N1; S12].

Leadership changes such as the appointment of interim CFO Thomas McGauley reflect management focus on financial stewardship amidst complex funding requirements inherent to late-stage biotech operations reliant on external capital raise cycles prior to commercialization [N1].

Licensing agreements impose certain financial commitments including milestone payments totaling up to $45 million contingent upon product launch sales achievements payable to Orion Corporation alongside tiered royalties based on net sales post-approval; these obligations necessitate disciplined capital planning ahead of revenue generation events [S19; S27].

Financial Performance: Chronicling Losses, Cash Burnout, and Capital Reserves

Detailed financial trends depict consistent absence of revenue generation coupled with significant negative earnings trajectories driven by increasing research expenditures related primarily to clinical trials:

Operating income reversed steeply from slight profit ($8.2M in FY23) back into heavy operational loss territory (-$56M in FY25), highlighting intense ramp-up in clinical development spend likely encompassing CRO fees, investigator site costs, drug manufacturing scale-up contracts outsourced per company disclosures [F1; S26].

Net income mirrors this deficit expansion ending FY25 at nearly negative $53M reflecting both operational burn and other expenses without offsetting revenues.

Operating cash flow deteriorated concomitantly signaling substantial consumption of liquid resources consistent with late-phase development mandates.

Capital expenditures remain negligible reflecting typical industry funding allocation heavily weighted toward variable costs rather than fixed assets.

Equity base has increased significantly consistent with documented equity raises aiding balance sheet strengthening resulting in nearly $97M equity as per YE25 figures underpinning solid capitalization status ahead of anticipated further capital needs during NDA submission phases pending trial completion [F1].

Approximate return on equity stands negative at roughly -54%, typical for development-stage biotechs absent product sales.

These financial dynamics illustrate intensity of ongoing trial investment balanced against manageable near-term liquidity reserves but foreshadow potential forthcoming funding requirements conditioned upon trial progression timelines.

Risks: Clinical, Regulatory, and Competitive Pressures on Tenax’s Trajectory

Tenax faces heightened risk concentration due to sole prioritization of oral levosimendan notwithstanding residual interest in imatinib which remains sidelined [S4; S6; S7]. The company recognizes dependence on successful execution of two costly Phase 3 studies whose outcomes bear uncertainty around enrollment completion rates plus potential discrepancies between interim results published preliminarily versus ultimate comprehensive findings verified post-audit procedures [S4; S9; S20]. Regulatory approval remains contingent not only upon positive efficacy/safety evidence but also subject to potential demand for additional studies modifying timing or scope thus elevating expense burdens or postponement hazards [S6; S29].

Intellectual property protections are well-established via multiple patents covering compositions/formulations extending patent life into medium-term horizons providing exclusivity support—but ongoing patent litigation risk along with competitive patent landscapes persist as industry-standard vulnerabilities [S19; S26].

Market acceptance risks include possible competition from big pharma entrants pursuing novel mechanisms or repurposed agents targeting overlapping patient populations often subsidized by broader commercial infrastructure unavailable to smaller developers like Tenax restricting sales reach post-launch absent partnership arrangements [S8; S16; S22; S28]. Reimbursement policies internationally offer wide variability imposing another layer of commercial uncertainty on pricing flexibility vital for recoupment of development investments.

Dependence on third parties for manufacturing oral formulations as well as outsourced CRO operations implies operational risks if these external vendors underperform or face regulatory compliance issues potentially causing delays or quality deficiencies impacting regulatory submissions or product availability timelines [S22; S29].

Next Steps: Upcoming Catalysts and What Investors Should Monitor

While explicit milestone dates have not been publicly disclosed beyond broad outlines indicating intentions to complete LEVEL trial enrollments followed closely by commencement/completion of LEVEL-2 study phases through mid-to-late calendar year horizons [N1; S3], critical upcoming value catalysts encompass announcements regarding:

• Final patient enrollment completions for both Phase 3 trials, • Top-line interim or full data readouts providing insights into therapeutic efficacy/safety, • Regulatory submissions timelines such as NDA filings contingent upon successful trial conclusions, • Potential partnerships or licensing deals that might expand commercialization capacity, • Any signs of manufacturing scale readiness evidencing supply chain robustness ahead of launch preparations.

Monitoring competitive developments especially from frontline contenders evaluated within similar patient segments will be essential given potential overlap affecting prescriber preferences if those competitors secure earlier approvals or demonstrate superior clinical profiles [S28].

In sum the trajectory remains highly binary shaped by crucial clinical outcomes set against firm but finite financial resource cushions emphasizing strategic capital management coupled tightly with operational execution precision over the next multiple quarters.

This report is prepared solely for informational purposes based on public disclosures without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments