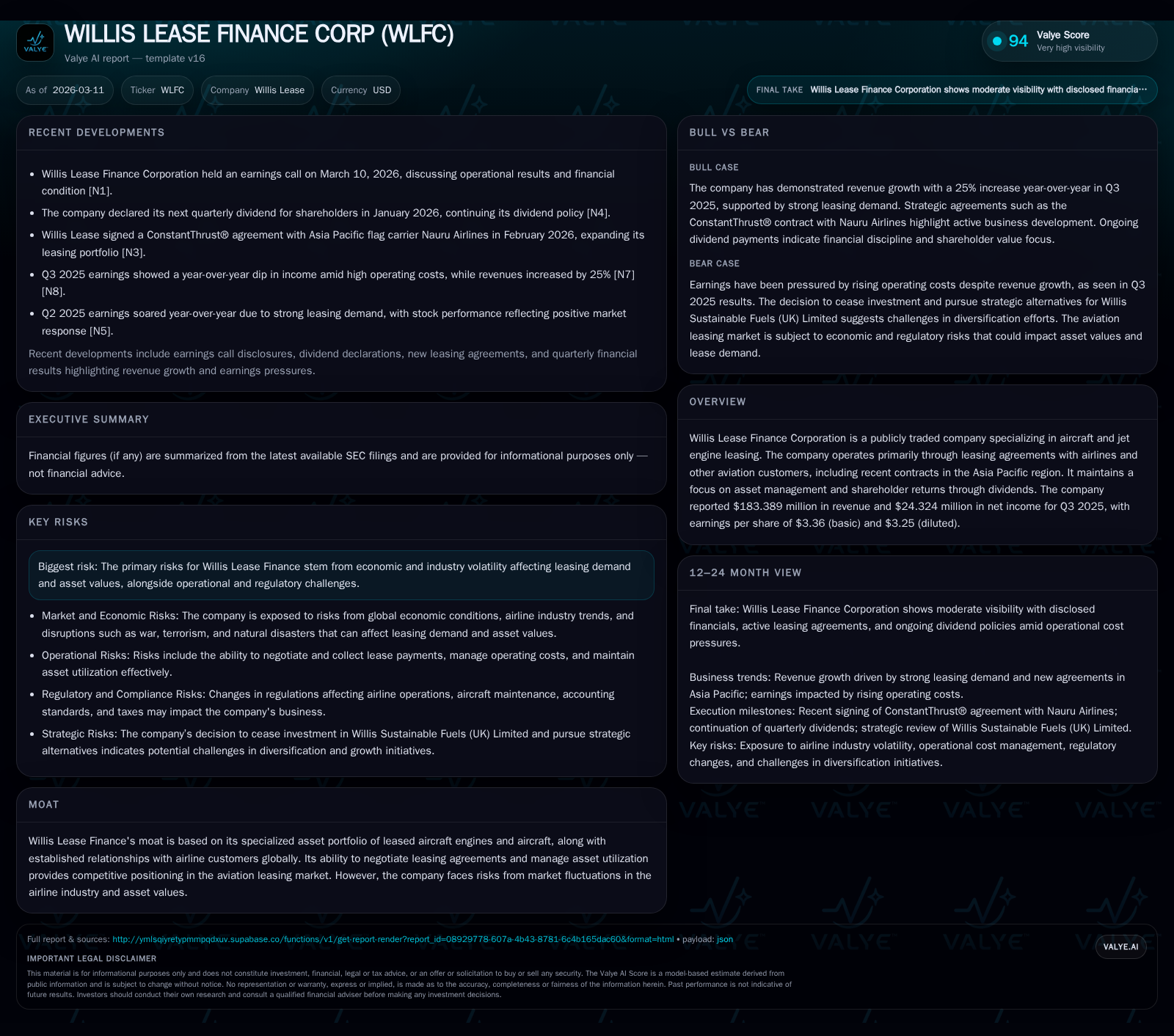

Willis Lease Finance Corp's Earnings Surge and Strategic Shifts Signal New Growth Trajectory

WLFC’s accelerated earnings growth and strategic geographic and capital initiatives highlight a pivotal inflection in aircraft engine leasing performance.

Willis Lease Finance Corporation (WLFC) demonstrated remarkable revenue and profit acceleration through FY2024, underpinned by effective operating leverage from its aircraft engine leasing portfolio. The company’s expanded focus on Asia Pacific markets, exemplified by a recent agreement with Nauru Airlines, aligns with asset portfolio optimization. WLFC maintains capital allocation discipline with increased dividends and buybacks supported by strong free cash flow, while managing liquidity prudently amid aviation sector cyclicality and regulatory risks. Investors should monitor lease utilization rates, incremental contract wins, and capital structure updates as key milestones ahead.

Transformative Growth: Revenue and Profit Expansion Through 2024

Willis Lease Finance Corporation (WLFC) delivered a compelling surge in financial performance by fiscal year-end 2024, showcasing a +36% increase in revenue to $569.2 million from $418.6 million a year prior [F1]. This top-line momentum was accompanied by an even more pronounced uplift in operating income that more than doubled (+124.8% YoY) to $144.4 million from $64.2 million in FY2023, underlying the effectiveness of operational scaling within its aircraft engine leasing specialization [F1]. Net income growth was particularly notable — tripling from a modest $5.44 million in FY2022 to $108.6 million in FY2024 — signaling improved portfolio utilization and yield management of leased jet engines and aircraft assets [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2024 | 569 | 109 | 284 | 144 | +36.0% | +148.1% |

| 2023 | 419 | 44 | 230 | 64 | +34.2% | +704.9% |

| 2022 | 312 | 5 | 144 | 10 | +13.8% | +62.3% |

| 2021 | 274 | 3 | 91 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2024 | 12 | 269 | 19.8 |

| 2023 | 0 | 225 | 10.0 |

| 2022 | 5 | 138 | 1.3 |

| 2021 | 10 | 88 | 0.9 |

Source: SEC companyfacts cache [F1].

This trajectory reflects an expanding footprint in the aircraft engine leasing industry with improved scale effects driving disproportionate profit gains versus revenue.

Key Drivers Fueling Willis Lease’s Operating Leverage

Dissecting underlying dynamics reveals that WLFC has effectively leveraged its asset base through elevated aircraft engine utilization rates — a core sector-native performance metric measuring time engines are actively leased versus idle — which translated into augmented lease yield expansion during the period [N1], [F1]. Management commentary during the March 10, 2026 earnings call emphasized enhanced negotiation outcomes on newer generation engine leases alongside reduced downtime contributing materially to operating leverage [N1]. This operational efficiency coupled with disciplined cost control enabled expenses to grow at a substantially lower rate than revenues, thereby magnifying net income growth.

Furthermore, recent engineering collaborations such as with CFM International aimed at extending operational life of CFM56-5B and CFM56-7B engines offer potential for prolonging lease terms and improving residual values—critical components of profitability given inherent asset remarketing cycles typical in aircraft leasing [N3], [S23].

Shaping the Future: Asia Pacific Expansion and Asset Portfolio Management

A pivotal strategic development underpinning future growth prospects is WLFC's targeted expansion into the Asia Pacific region, evidenced by the February 2026 ConstantThrust agreement with Nauru Airlines — an Asia Pacific flag carrier — seeking optimized engine leasing solutions aligned with regional fleet modernization efforts [N4]. This collaboration reflects WLFC’s deliberate concentration on emerging markets within the aviation sector where increased air travel demand drives heightened leasing appetite for contemporary aircraft engines.

The company also announced early January partnerships with private credit vehicle Blackstone Credit & Insurance (BXCI) to launch a scaled aircraft engine leasing platform deploying over $1 billion into select assets highlighting WLFC’s refined portfolio management strategy emphasizing financing flexibility and specialization within higher-margin next-generation engines [S22]. This joint venture approach may amplify WLFC’s ability to source, manage, and finance desirable aircraft engine stock efficiently.

Evaluating Growth Constraints Amid Industry Cyclicality

Nevertheless, WLFC operates under several constraints primarily tied to cyclicality inherent in the global airline industry, where macroeconomic downturns impact airline profitability thereby affecting leasing demand. Fleet retirements or accelerated phase-outs of older engines can exacerbate residual value risks — that is potential depreciation beyond expected thresholds negatively impacting asset valuations on balance sheets [S4], [S6]. Regulatory developments around environmental standards or aviation safety impose additional compliance costs with possible operational disruptions.

Legal proceedings disclosed within their annual report create a layer of risk that could affect capital deployment if materialized significantly [S4]. Furthermore, fluctuations in oil prices indirectly influence airlines’ operational economics impacting their lease term decisions which WLFC must closely monitor.

Capital Allocation Discipline: Dividends, Buybacks, and Cash Flow Dynamics

On capital returns front, WLFC has displayed prudent discipline balancing shareholder payouts and reinvestment needs. Quarterly dividends have held firm at $0.40/share as declared recently for Q1-2026 reflecting stable income generation capacity amidst reinvestment into fleet upgrades reflected by capex rising over +200% YoY to approximately $16 million in FY2024 from just $5 million prior year [S20], [F1]. Meanwhile, share repurchases resumed with buybacks totaling roughly $11.6 million indicating confidence in capital deployment opportunities at current valuation levels.

Free cash flow (operating cash flow minus capex) remains robust at about $268.8 million supporting sustainable dividend policy combined with reinvestment capability ensuring long-term asset quality maintenance critical for airline customers dependent on reliable equipment availability.

ROE approximated near a healthy ~19.8% demonstrates effective equity utilization consistent with specialized asset-light lessor models prevalent within this aviation segment.

Liquidity and Balance Sheet Health Supporting Strategic Flexibility

WLFC’s balance sheet strength is evidenced by equity increasing steadily to over $549 million as of December-end FY2024 paired with comprehensive management of debt covenants via successive credit agreement amendments enhancing maximum leverage ratios – notably excluding certain financing facilities from total debt calculations—improving room for tactical debt usage if necessary to fund acquisitions or expand platforms [S7], [S16], [S21].

Multiple recent SEC Form 8-K filings between Jan-Mar 2026 document active liquidity monitoring including adjustments favoring flexibility over strict deleveraging indicative of strategic capital structure agility aligned with cyclical demands characteristic of aircraft leasing businesses containing large fixed asset bases .

Emerging Risks: Regulatory, Market Volatility, and Operational Hurdles

Key risk exposures include residual value deterioration linked to rapid technological obsolescence or reduced engine demand seen intermittently in slower global travel phases which directly impairs asset remarketing values—a classic stress point for lessors focused on non-aircraft assets such as jet engines rather than whole fleets alone (which itself carries different risk-return profiles) [S4], [F1].

Additionally, complex regulatory frameworks governing airworthiness certifications along with insurance premiums shifting upwards present potential pressure points on margins necessitating vigilant expense management going forward.

Legal proceedings flagged expose possible contingent liabilities adding uncertainty although disclosures do not currently indicate material adverse impacts, underlining the importance of monitoring developments closely alongside external factors such as geopolitical disruptions or fuel price shocks affecting airline solvency.

Investor Focus: Milestones Ahead and What to Monitor

Looking forward, investors should prioritize monitoring upcoming quarterly earnings releases for sustained metrics improvements notably recurring revenue growth trends tied to new or extended leases appearing among pipeline contract announcements discussed during recent earnings calls and press releases [N1], [N2]. Utilization rates remain a critical indicator reflecting how effectively leased engines generate revenue versus idle times influenced by overall airline traffic patterns.

Capital structure changes involving further credit line optimization or anticipated share repurchase programs will provide insight into management’s confidence regarding valuation support. Likewise dividend stability against net income trends will be telling about cash generative capabilities amid market volatilities.

Overall, Willis Lease Finance Corp presents a compelling narrative around accelerating earnings from core competency-driven operational advantages paired with geographic expansion targeting Asia Pacific leasing segments coupled with robust capital stewardship balancing shareholder returns alongside growth investments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments