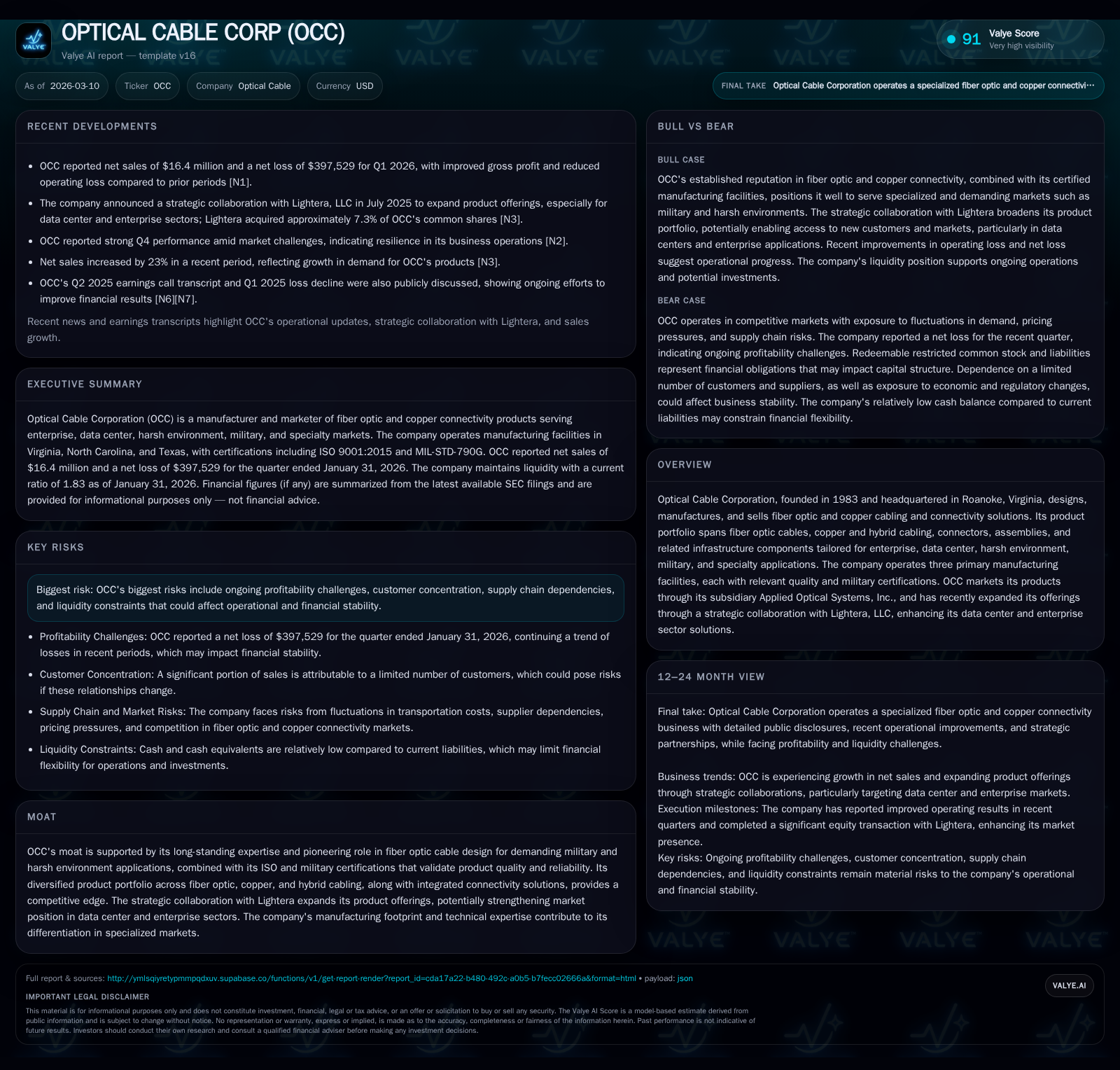

OPTICAL CABLE CORP Balances Niche Expertise with Profitability Challenges

OCC’s specialized fiber optic and hybrid cabling solutions sustain growth amid operational and liquidity risks.

Founded in 1983, Optical Cable Corp (OCC) leverages its manufacturing expertise and certifications to serve enterprise, military, and harsh environment markets with fiber optic and copper cabling solutions. Its strategic partnership with Lightera expands data center offerings, underpinning future growth potential. However, historical financials reveal volatility in profitability despite revenue improvement, with risks from customer concentration and liquidity constraints remaining salient. Monitoring cash flow trends, customer diversification, and successful refinancing of near-term debt will be key going forward.

Company Overview

Optical Cable Corporation (OCC), founded in 1983 and based in Roanoke, Virginia, designs and manufactures fiber optic, copper, and hybrid cabling as well as related connectivity solutions. It targets highly specialized segments including enterprise networking, data centers, military applications, harsh environments, and specialty communications systems. OCC operates manufacturing facilities certified under ISO and various military standards—credentials critical to its niche markets .

The firm's subsidiary Applied Optical Systems Inc. primarily serves U.S. customers but also sells internationally with revenues denominated in U.S. dollars. Since July 2025, OCC has a strategic collaboration with Lightera LLC aimed at expanding integrated cabling offerings within the growing data center and enterprise sectors. This includes Lightera acquiring approximately 7.3% of OCC's shares [S25].

Historical Financial Performance

OCC has shown notable revenue growth over the last decade. Revenue increased from about $10.6 million in FY2013 to roughly $20.3 million by FY2018—an approximate doubling reflecting broader market penetration within enterprise connectivity and specialty cables suited for demanding environments [F1].

However, operating income has been volatile: from $473K in FY2022 to an operating loss near $1.29 million in FY2023 before recovering moderately to $269K in FY2025 [F1]. Net income followed a similar trajectory, declining sharply by 87% year-over-year to $49K in FY2025 compared to $373K the prior year.

Margins are affected by fluctuating product mix; copper-rich hybrid cables tend to yield lower gross margins than pure fiber optics. Supply chain factors such as raw material costs—including precious metals—and production efficiencies also influence profitability [S7][S12][S16].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | 1414075 | 268748 | 295537 | -87.0% |

| 2024 | 0 | -857024 | 662088 | 369630 | -81.9% |

| 2023 | 2 | -395676 | -1291388 | 520847 | +695.4% |

| 2022 | 0 | -1587544 | 472864 | 279810 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 1118538 | 0.3 |

| 2024 | -1226654 | 1.8 |

| 2023 | -916523 | 8.4 |

| 2022 | -1867354 | -1.6 |

Source: SEC companyfacts cache [F1].

*Latest fiscal year data per available filings; YoY denotes year-over-year change where applicable [F1].

Growth Drivers and Limitations

OCC's ISO and military-grade certifications provide competitive advantages in demanding markets requiring ruggedized optical solutions. The Lightera partnership potentially opens incremental opportunities within data center infrastructure through integrated product offerings [S25].

Customer concentration remains significant with one distributor accounting for approximately 15–22% of sales across recent quarters—a key risk factor for revenue stability [S4][S16][S21]. Product mix volatility impacts margins quarter-to-quarter given differing profitability profiles between fiber optic versus copper-enriched hybrid cables.

Supply chain challenges include raw material price fluctuations (e.g., precious metals), specialized manufacturing equipment dependencies, and exposure to tariffs or currency fluctuations despite U.S.-dollar-denominated international sales [S9][S12].

Liquidity & Capital Structure

Liquidity is pressured by the approaching maturity of the Virginia Real Estate Loan (~$2.6 million outstanding) due May 2026 alongside an $18 million revolving credit facility subject to interest rates around 8.5%–9% [S14][S20]. The company intends to refinance this debt.

As of January 31, 2026, OCC held approximately $126K in cash and equivalents with a current ratio near 1.83 indicating manageable short-term liquidity supported by working capital assets exceeding current liabilities [F1][S2].

Capital Allocation & Returns

OCC's trailing return on equity is modest at approximately 0.3%, reflecting narrow net income relative to shareholder equity of about $16.5 million at fiscal year-end 2025 [F1]. Operating cash flow recovered strongly to positive $1.41 million in FY2025 following prior years’ outflows.

Capital expenditures remain moderate near $296K annually consistent with sustaining existing operations rather than expansionary investment [F1]. No dividends or share repurchases have been declared or executed recently indicating focus on liquidity preservation amid financial pressures.

Outlook & Monitoring Points

While explicit guidance is absent from recent filings or earnings calls [N1][N2], key indicators for investors include progress on refinancing near-term debt obligations as well as commercial traction from the Lightera collaboration during calendar year 2026.

Monitoring quarterly revenue growth post-integration alongside margin trends will be critical given historical volatility tied to product mix and customer concentration risks.

Conclusion

Optical Cable Corp remains a specialist player leveraging quality certifications that enable access to demanding markets including military-grade cabling solutions. The partnership with Lightera offers potential growth avenues but financial results highlight persistent profitability challenges compounded by concentrated customer exposure and upcoming refinancing needs.

Investors should closely watch operational cash flow trends alongside debt refinancing outcomes as primary indicators of near-term financial resilience.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments