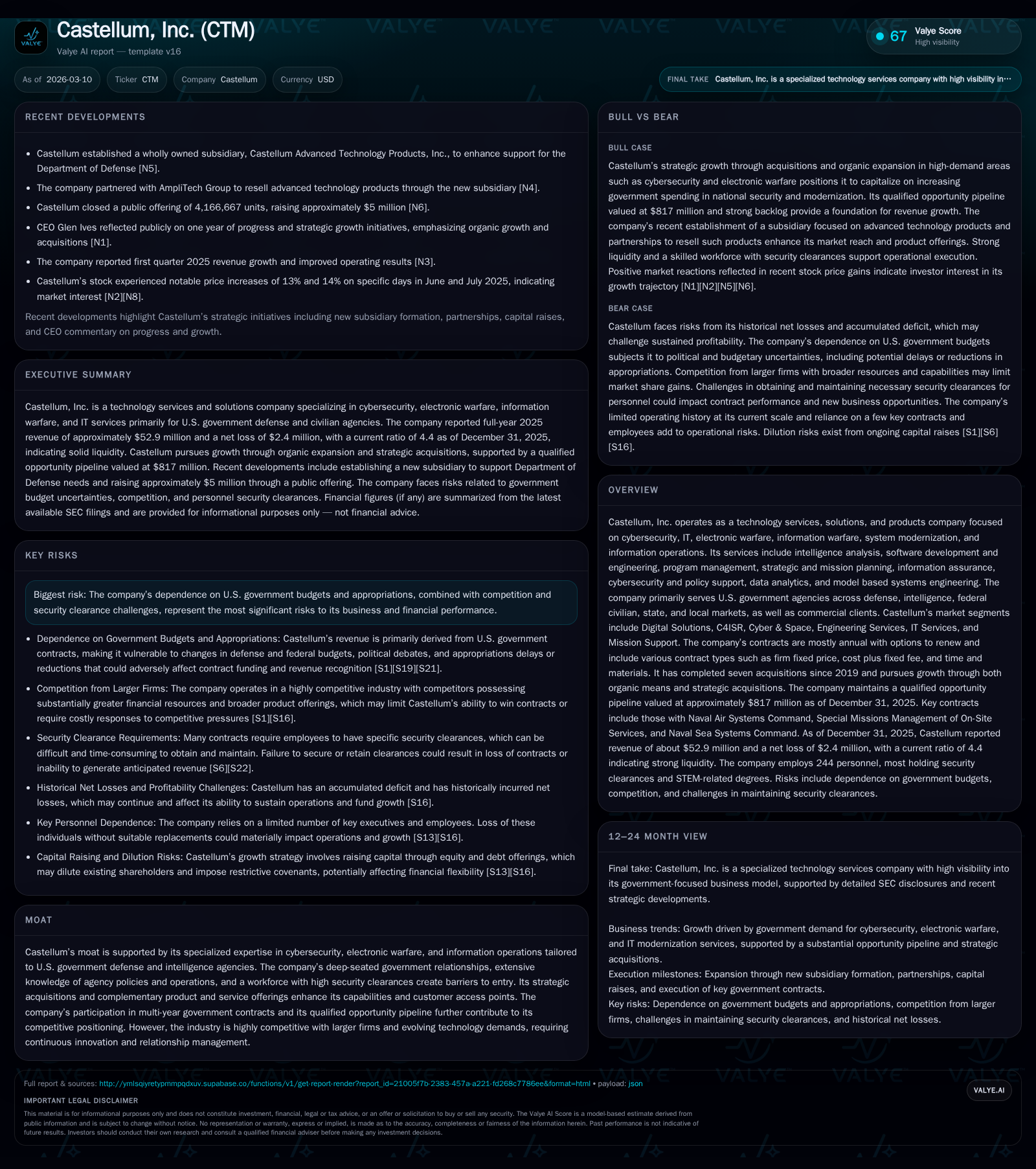

From Opportunity Pipeline to Market Realities: Castellum’s Assessment of Growth and Execution

Castellum, Inc.’s acquisition-driven revenue growth contrasts with ongoing operating losses as it pursues scale in competitive government cybersecurity and intelligence markets.

Castellum, Inc. has demonstrated robust top-line growth primarily fueled by seven strategic acquisitions since 2019 that expanded its footprint across U.S. government technology service sectors including cybersecurity, electronic warfare, and information operations. Despite rising revenues, the company has yet to achieve net profitability, grappling with elevated costs tied to integration, security clearance requirements, and competitive pressures from larger incumbents. With an $817 million qualified opportunity pipeline underpinning future prospects, Castellum’s path to sustained profitability involves addressing workforce constraints and navigating government budget uncertainties while leveraging its expanding contract backlog and diversified service offerings.

Revenue Growth Trajectory Fueled by Strategic Acquisitions

Castellum’s recent financial disclosures highlight a clear trajectory of accelerated top-line expansion, primarily achieved through an acquisition-led strategy. Since 2019, the company completed seven acquisitions targeting capabilities in cybersecurity, IT modernization, electronic warfare, and information operations tailored for U.S. government agencies [S1][S4]. This inorganic growth bolstered annual revenues from approximately $42.2 million in FY2022 to $52.9 million in FY2025 — a compound increase of over 25% across three years and representing an 18.1% year-over-year increase between FY2024 and FY2025 alone [F1].

Executive commentary within filings indicates that while acquisitions have driven much of this revenue momentum, internal organic growth initiatives are being simultaneously developed leveraging the management team’s prior experience scaling related businesses [S1][S4]. The acquisitions not only expanded technical capabilities but also broadened access to multiple branches of the U.S. federal government market across defense, intelligence, federal civilian agencies, as well as select state/local entities.

The company’s portfolio now spans several mission areas segmented into Digital Solutions; C4ISR; Cyber & Space; Engineering Services; IT Services; and Mission Support — reflecting a comprehensive approach to government modernization challenges [S4]. This breadth supports growing demand from U.S. governmental customers needing agile solutions amidst evolving cyber threats and increased emphasis on electromagnetic spectrum dominance.

Operating Losses Amid Scaling Efforts: Cost Structure and Profitability Dynamics

Despite strong revenue gains, Castellum continues facing challenges in translating top-line growth into sustained profitability. Operating income has improved meaningfully — narrowing losses from roughly -$10 million in FY2022 to about -$2.8 million in FY2025 [F1] — yet the company remains unprofitable on both an operating and net basis (net loss approximately $2.4 million for the same period).

These operating losses stem partly from ongoing amortization expenses related to acquisition goodwill and intangible assets as well as elevated costs associated with integration efforts and scaling overheads inherent in an early-stage consolidated entity [S1][S2]. The firm discloses typical early enterprise costs including investments into personnel recruitment (especially security-cleared staff), compliance infrastructure, and process maturation necessary for complex USG contract performance [S1]. Furthermore, given the diverse contract types—ranging from firm fixed price (FFP) to cost plus fixed fee (CPFF) arrangements—the company must carefully manage cost structures amid variable risk exposure [S14].

Operating cash flow deteriorated sharply in FY2025 into negative territory (-$1.95 million), reversing prior positive CFO performance confirming cash burn linked to investment outlays despite topline gains [F1]. Meanwhile, capital expenditure levels jumped by considerable multiples though still modest overall ($152k in FY2025 vs $3k in FY2024) signaling incremental investments in infrastructure or technology assets consistent with buildout phase [F1].

Robust Contract Pipeline Illustrates Opportunities in U.S. National Security Markets

An important validation of Castellum’s forward sales prospects is its substantial qualified opportunity pipeline valued at approximately $817 million as of December 31, 2025 [S4]. This backlog figure encompasses potential future revenue from contract vehicles that have been competed and are under consideration including base year contract values plus all priced options — representing multi-year U.S. government spending intentions across defense modernization priorities.

The diversified contract portfolio includes engagements spanning the Department of Defense’s Naval Sea Systems Command, intelligence community programs focused on electronic warfare capabilities, information assurance projects supporting cybersecurity resilience initiatives, among others [S11]. The company highlights that most contracted work is operationally funded on an ongoing basis aligning well with bipartisan national security imperatives currently driving Congressional budget allocations [S14][S19].

However, it is notable that backlog conversion is subject to inherent uncertainties tied to Congressional appropriations cycles; unfunded backlog elements depend on subsequent budget authorization which can delay or diminish revenue realization [S13][S17]. Effective execution against this pipeline requires optimizing resource deployment against funded awards while managing potential shifts in U.S political and fiscal environments.

Workforce and Security Clearance Hurdles as Operational Constraints

A sector-critical challenge underlying Castellum’s pacing toward scale is the procurement and retention of qualified personnel holding requisite security clearances — a fundamental prerequisite for contract eligibility within the classified cybersecurity space it serves [S2][S5][S16].

Security clearance acquisitions are inherently protracted due to stringent governmental vetting processes affecting hiring lead times and complicating rapid personnel onboarding particularly when expanding contract volumes necessitate swift staffing increases.

This constraint directly impacts revenue recognition potential since uncontested contract awards require cleared staff deployment to fulfill performance milestones on schedule [S2]. Moreover, the company faces competition for talent not only from large incumbent defense contractors such as Northrop Grumman or Booz Allen Hamilton but also from emerging technology firms increasingly entering adjacent cyber domains [S5]. Failure to meet these personnel demands risks contract non-fulfillment or loss thereby pressuring margins further.

Analysis of Key Risks: Government Funding Dependence and Competitive Pressures

Castellum operates heavily concentrated within U.S. government markets making it vulnerable to fluctuations in federal funding tied to political priorities and budget negotiations [S1][S5][S6][S25][S26]. Although current appropriations provisions maintain steady funding through fiscal year-end 2026 for most agencies served including Department of Defense programs, partial shutdowns affecting other governmental bodies illustrate persistent unpredictability impacting overall demand visibility [S20].

Competitive intensity remains high with numerous established firms inhabiting similar niche technologies accompanied by overlapping prime-subcontractor dynamics common across defense contracting [S14][S26]. Larger companies’ broader product suites afford economies of scale advantages sometimes leveraged via aggressive pricing tactics or integrated offerings challenging smaller peers like Castellum.

Furthermore regulatory complexity encompassing FAR compliance, cost accounting standards audits, CMMC certification readiness efforts establish administrative burdens that add operational risk layers potentially inflating bid costs or constraining agility [S10][S23]. Missteps can result in financial penalties or suspension risks detrimental to business continuity.

Capital Allocation Insights: Cash Flows, Investment, and Shareholder Returns

Financial statements reveal Castellum currently exhibits negative free cash flow (approximate -$2.1 million in FY2025) combining operating cash outflows with incremental capital expenditures reflective of reinvestment during growth phases characteristic for emerging government tech services companies aiming for scale-out profitability [F1][S20].

Return on equity remains negative (~ -6.7%) echoing historical net losses accumulated into a deficit north of $56 million as of end-2025 signifying shareholder capital remains burdened by ongoing enterprise build costs without current earnings offset [F1][S1][S18].

There is no indication of dividends or share repurchase programs indicating preservation of available liquidity priority over distributions at this juncture given the capital-intensive nature of acquisitions combined with organic growth investments reported elsewhere.

The Company has articulated a disciplined approach towards acquisitions emphasizing accretive opportunities aligned with strategic capabilities expansion while mindful of net present value considerations supporting long-term financial sustainability ambitions [S20]. However securing additional financing may remain necessary given continued cash consumption patterns highlighted across recent fiscal periods with attendant dilution or leverage risks discussed candidly by management [S21].

Metrics Spotlight: Understanding ROE, Cash Flow Evolution, and Capex Trends

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 53 | -2 | -2 | -3 | +18.1% | +76.0% |

| 2024 | 45 | -10 | 1 | -7 | -1.1% | +43.9% |

| 2023 | 45 | -18 | -2 | -17 | +7.2% | -19.4% |

| 2022 | 42 | -15 | 1 | -10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -6.7 |

| 2024 | 1 | -49.5 |

| 2023 | -2 | -137.5 |

| 2022 | 1 | -85.0 |

Source: SEC companyfacts cache [F1].

*All figures USD thousands: Revenue (Rev), Operating Income (OpInc), Net Income (Net), Operating Cash Flow (CFO), Capital Expenditures (Capex). Year-over-year percentages compare latest fiscal year versus prior.

This view encapsulates Castellum’s dual reality: accelerating top-line backed by successful acquisitions alongside constrained profitability metrics reflecting typical scale-up challenges within federally contracted cybersecurity sectors.

Looking Ahead: Catalysts to Watch and Market Expectations for Castellum

Absent explicit forward earnings guidance provided by management at present [N#], investors should monitor several pivotal elements shaping Castellum’s near-term trajectory:

- Conversion rates from qualified opportunity pipeline within funded backlog into recognized revenues over next one-to-two years amid Congressional appropriation cycles [S13][S19];

- Progress against recruitment goals addressing clearance bottlenecks critical for contract execution velocity reported by leadership as strategic priority [S11];

- Successful integration outcomes from past M&A activity underpinning margin improvements through scale efficiencies;

- Continued engagement with key clients such as Naval Sea Systems Command providing multi-option contract vehicles signaling sustainable revenue streams;

- Macroeconomic or geopolitical developments influencing U.S. defense spending allocations affecting competitive dynamics;

- Regulatory environment evolutions around procurement reform impacting bidding strategies or contractor compliance costs.

Execution risks rest predominantly on balancing rapid capability build with disciplined financial management amidst competitive pressures exerted by dominant industry players with entrenched client relationships and broader portfolios [S5][S26].

For stakeholders tracking companies at the intersection of government cybersecurity modernization services with exposure to complex programmatic funding landscapes and workforce clearance dependencies, Castellum offers a compelling case study revealing operational realities behind acquisition-fueled expansion narratives.

This analysis is based exclusively on disclosed financial data and regulatory filings without extrapolations or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments