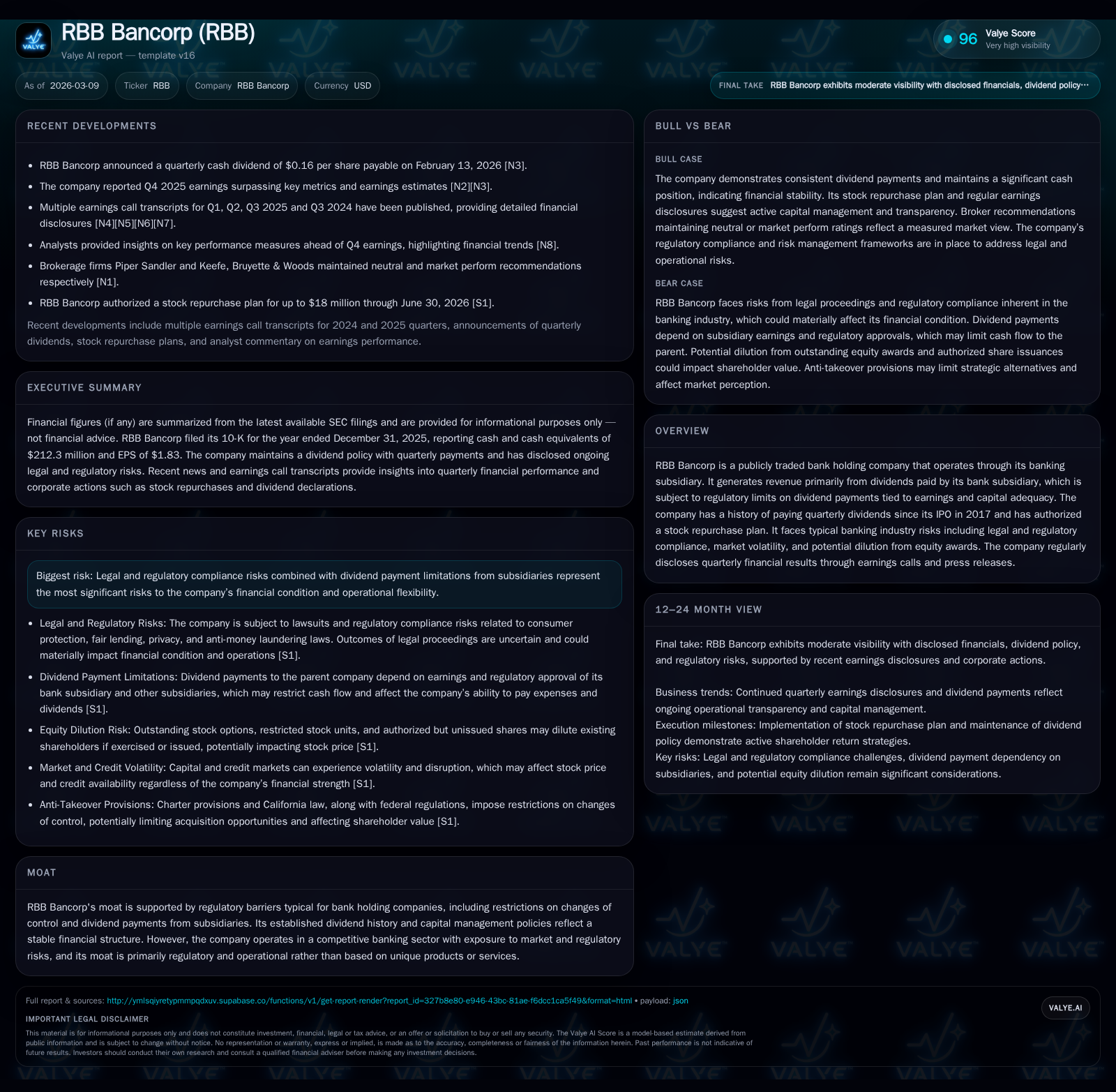

RBB Bancorp’s Steady Dividend Model Constrained by Regulatory Dividend Limits and Industry Risks

Regulatory frameworks and legal exposures notably shape RBB Bancorp’s financial returns and growth outlook.

RBB Bancorp has maintained consistent net income growth since its 2017 IPO, underpinned by dividend payments from its banking subsidiary restricted by regulatory capital requirements. Operating cash flows have softened somewhat recently, while the company sustains its $0.64 per share annual dividend with cautious capital management including an active stock repurchase program. Legal and regulatory compliance risks remain meaningful headwinds, alongside structural limits on dividend distributions from the bank to the holding company. Future growth will depend on navigating these constraints and market dynamics.

Historical Financial Performance

RBB Bancorp has exhibited a stable financial trajectory since its IPO in 2017, driven mainly by dividends received from its bank subsidiary which funds both operational expenses and shareholder returns [S1]. The company paid total dividends of $0.64 per share consistently across 2023, 2024, and 2025 [S1][S5]. Its net income showed upward momentum with a notable increase from approximately $9.5 million in FY2018 to over $10.6 million by FY2019, reflecting a compound average growth supported by measured expense control and asset quality [F1]. Despite this growth in earnings, return on equity remains modest at around 2% based on latest figures (FY2025 net income vs equity) [F1].

Operating cash flows peaked above $93 million in FY2022 but declined to $43.4 million in FY2025—a drop attributable possibly to loan portfolio shifts or changes in working capital components—though still generating substantial free cash flow of roughly $42.6 million after minimal capital expenditures ($798,000 FY2025) [F1]. Capital spending is relatively low reflecting typical banking operations focused on branch infrastructure and technology enhancements.

A sizeable part of capital return comes via share repurchases authorized up to $18 million through June 2026 [S7], with nearly $14 million executed during FY2025—indicating management's commitment to returning excess capital to shareholders alongside stable dividend issuance [F1][S10]. Dividends paid amounted to approximately $11.3 million in FY2025 [F1].

Historical performance (annual)

| FY | CFO ($mm) | Capex ($mm) |

|---|---|---|

| 2025 | 43 | 1 |

| 2024 | 58 | 1 |

| 2023 | 51 | 1 |

| 2022 | 94 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 11 | 14 | 43 |

| 2024 | 12 | 21 | 58 |

| 2023 | 12 | 7 | 51 |

| 2022 | 11 | 20 | 92 |

Source: SEC companyfacts cache [F1].

Note: Historical net income data beyond FY2019 is unavailable; YoY percentages reflect nearest comparable periods.

Future Growth Prospects

RBB Bancorp's future revenue growth is tightly linked to the performance and dividend capacity of its bank subsidiary, which is constrained by regulatory capital adequacy requirements that limit upstream payments to the holding company [S1][S5]. While the company's moat is primarily regulatory and operational rather than product-based innovation or unique client relationships, this regulatory insulation presents a double-edged sword: it limits downside risk but caps rapid dividend expansion.

Growth drivers would include improved profitability at the bank level through loan portfolio expansion, fee income enhancements, or interest margin improvements as macroeconomic conditions permit—but all must balance against maintaining robust capital buffers prescribed by regulators [S1]. Additionally, active capital management including share buybacks suggest management prioritizes shareholder returns within conservative growth bounds [S7][S10].

Risks that could cap growth include heightened legal exposure given extensive regulatory compliance demands across consumer protection laws, anti-money laundering statutes, information security regulations, and fair lending practices — all prominent risk areas for banks today [S4][S6]. Furthermore, market volatility impacting credit availability or increased competition in target geographic markets (primarily California) could pressure net interest margins or loan book quality.

Upcoming Milestones and Guidance Signals

While explicit forward guidance beyond maintaining current dividend policy exists sparingly [N3][N4], key signals to monitor include:

- Quarterly earnings releases providing updates on net interest margins and non-interest income trends [N1][N2]

- Regulatory communications regarding capital ratios impacting dividend capacity [S1][S5]

- Updates on authorized share repurchase activity utilization or amendments [S7]

- Legal proceedings outcomes that might influence contingent liabilities or reserve levels [S4]

These milestones will help gauge the balance between sustainable returns versus potential profit headwinds.

Capital Allocation and Returns Profile

RBB Bancorp exhibits disciplined capital allocation characterized by consistent dividends equating to approximately $0.64 annually per common share since inception in Q3 2017 without obligation thereof [S1][S5]. Dividends totaled roughly $11–12 million annually over recent years despite some fluctuations in operating cash flow [F1]. The company supplements shareholder value via opportunistic buybacks — nearly doubling repurchase activity in FY2024 relative to prior years before tapering slightly in FY2025 yet maintaining material engagement [$14 million repurchased] [F1][S7].

The combination highlights a balanced approach seeking shareholder yield without compromising requisite capital safeguards mandated for bank holding companies.

The approximate ROE calculated from available data stands subdued near ~2%, reflective of the holding company's role primarily as a fund conduit deriving earnings through regulated subsidiaries rather than direct operational leverage expansion [F1]. Cash reserves remain healthy at over $212 million as of December 31, 2025 lending liquidity support amid ongoing market uncertainty [F1].

Legal and Regulatory Risk Considerations

Legal risks span multiple dimensions including lawsuits typical within banking sectors concerning compliance lapses or regulatory investigations; management does not currently expect material adverse impacts from ongoing litigation although contingencies remain inherently uncertain [S4][S6]. Moreover, dividend declaration is at board discretion contingent upon both earnings sufficiency and external regulatory approvals tied directly to subsidiary capitalization — posing a crucial operational limitation uncommon outside banking industries but instrumental here [S1][S5].

Additionally, share issuance provisions allow potentially dilutive equity instruments under incentive plans capped at just under one million shares outstanding for awards as of year-end 2025 which could pressure future market prices if issued extensively [S5][S11]. Anti-takeover clauses embedded within corporate charter impose further controls on ownership concentration providing stability but restricting certain strategic opportunities or premium acquisition scenarios [S11].

Analysis Summary

RBB Bancorp functions principally as a holding entity reliant on dividends from its locally concentrated banking subsidiary constrained by regulatory capital rules affecting payout capacity—an endemic characteristic among similar publicly traded regional bank holding companies emphasizing stability over aggressive growth gambits.

Its steady dividend track record paired with proactive stock buybacks underscore consistent shareholder return priorities within tight operational liquidity frameworks bolstered by significant cash holdings.

Future progression requires deft navigation of tightening capital constraints amidst heightened legal/regulatory scrutiny combined with evolving market lending conditions to sustain profitably incremental expansion without jeopardizing permissible dividend streams or incurring disproportionate risk exposure.

Like many community-oriented banks emerging post-financial crisis IPOs with moderate asset bases yet active capital strategies aimed at maximizing shareholder value under prudential guardrails, RBB Bancorp demonstrates operational resilience though limited upside leverage absent transformative catalysts beyond those currently visible.

Disclaimer: This analysis is based solely on publicly available information as of March 9, 2026, including SEC filings and recent news reports without prediction or recommendation concerning investment action.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments