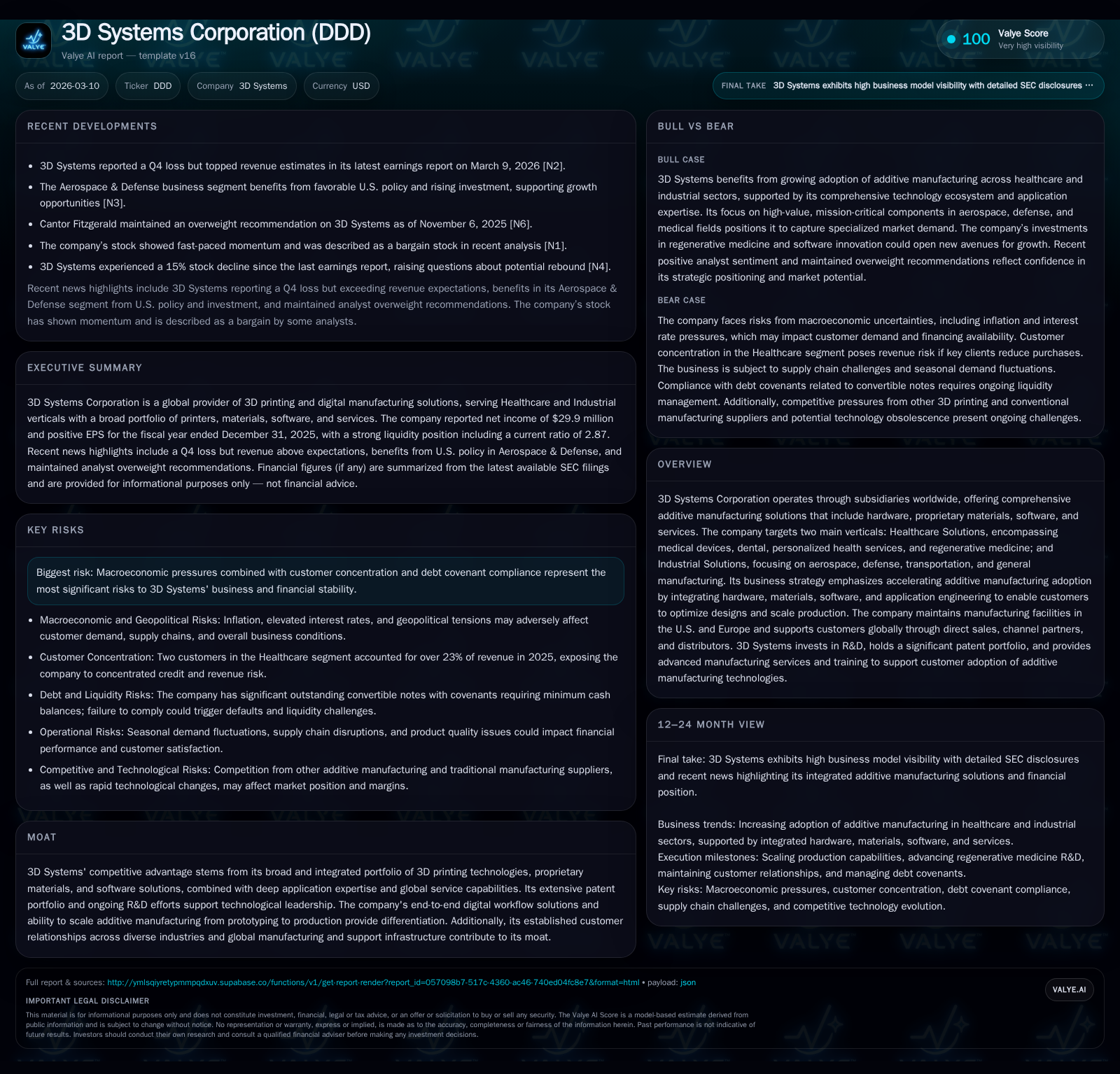

3D Systems Corp’s Recovery Hinges on Scaling Additive Manufacturing Amid Financial Strains

The company leverages its integrated 3D printing ecosystem to drive growth in healthcare and industrial verticals despite recent operating losses and liquidity pressures.

3D Systems Corporation operates a diversified additive manufacturing platform combining hardware, materials, software, and services with a significant patent portfolio. While revenues showed a modest rebound in 2025 after steep losses in prior years, ongoing operating losses and negative cash flow reflect operational challenges and macroeconomic headwinds. The firm’s differentiated end-to-end additive workflows—especially in healthcare and industrial sectors—underpin future growth prospects, balanced by risks from customer concentration, debt covenants, regulatory compliance, and supply chain factors. Investors should monitor the company’s ability to convert application innovation into scalable production alongside capital structure developments.

Overview of Business Model and Market Position

3D Systems Corporation presents itself as a comprehensive additive manufacturing solutions provider integrating proprietary hardware platforms, printing materials across plastics and metals, software suites designed for print process optimization, plus application engineering and advanced manufacturing services [S1][S4]. The company targets two main verticals — Healthcare Solutions encompassing medical devices, dental applications, personalized health services, and regenerative medicine; alongside Industrial Solutions serving aerospace, defense, transportation, and general manufacturing segments. 3D Systems’ competitive moat derives largely from this breadth: an end-to-end digital workflow that enables customers not only to prototype rapidly but also scale additive manufacturing capacity efficiently into production environments [S23].

The company operates globally via subsidiaries spanning the Americas, EMEA, and APAC regions with principal design and production centers located in the U.S. (South Carolina and Colorado) and Europe (France), supplemented by sales channels comprising direct force, channel partners, and distributors [S4][S5]. This geographic footprint exposes it to foreign exchange volatility as well as geopolitical trade tensions that pose supply chain disruption risks [S14].

Historical Financial Performance

Recent annual financial metrics exhibit volatility reflective of transitional industry dynamics alongside company-specific operational difficulties:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 30 | -88 | -96 | 10 | +111.7% |

| 2024 | -256 | -45 | -277 | 16 | +29.5% |

| 2023 | -363 | -81 | -406 | 27 | -195.6% |

| 2022 | -123 | -70 | -117 | 21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | -98 |

| 2024 | -61 |

| 2023 | -108 |

| 2022 | -91 |

Source: SEC companyfacts cache [F1].

*Excerpts mention latest figures up to FY ending Dec 31, 2025 [F1]

Though explicit revenue figures beyond FY2017 are not provided [F1], the sharp narrowing of operating losses from an extraordinary deficit in the hundreds of millions to under $100 million by FY2025 indicates management initiatives to stabilize cost structure or reorient operations were partially effective [F1]. This is coupled with a rare swing back to net income profitability after several years of significant net losses [F1]. However, cash flow trends are concerning as operating cash flow deepened its negative position in FY2025 compared with FY2024 suggesting persistent working capital demands or delayed collections impacting liquidity [F1]. Capital expenditures have also significantly receded likely reflecting tightened investment discipline or reduced expansion plans [F1].

Strategic Growth Prospects

3D Systems explicitly seeks growth through expanding additive manufacturing adoption by offering tightly integrated hardware-materials-software-service bundles capable of scaling from initial prototyping through serial production within customer facilities [S1][S23]. The Applications Innovation Group serves as a focal point for co-developing specialized printing solutions tailored to customer-specific products tackling design complexity and production challenges unique to healthcare or heavy industry uses [S1]. Accompanying this is advanced manufacturing capacity enabling a staged ramp-up model that transfers know-how seamlessly to customer manufacturing operations for volume fulfilment.

The healthcare vertical benefits from demand drivers including personalized implants, dental restorations using biocompatible materials, as well as regenerative medicine applications where emerging bioprinting techniques hold longer-term promise [S1][S18]. Industrial opportunities revolve around aerospace parts consolidation for weight reduction, defense components requiring precision fabrication of complex geometries, transportation sector part customization, and general durable goods leveraging shorter lead times and mass customization enabled by additive processes.

Organic growth may be buttressed by selective acquisitions enhancing material science capabilities or software tools designed for smart print-farm management — moves consistent with sustaining technological leadership amid rapid innovation cycles typical of disruptive manufacturing technologies [S18][S26].

Nevertheless, growth remains constrained by macroeconomic uncertainties including inflation impacts on client capital expenditures particularly in conservative aerospace/defense sectors; customer financing challenges amid elevated global interest rates; plus geopolitical trade disruptions that can affect raw material sourcing or final product exports [S14][S19]. High customer concentration further magnifies revenue volatility risk where top two healthcare clients accounted for nearly one-quarter of revenue in the latest fiscal year [S5][S14]. Ensuring diversification without diluting focus on core sectors is a delicate balance.

Forecasts & Key Milestones (Analysis)

While no explicit future guidance was disclosed in provided filings or news releases ([N1][N2][S24]), several leading indicators can be identified:

- Progress scaling selected beta customers’ additive manufacturing lines into volume stage would signal validation of the company’s core business model.

- Stabilization or improvement in operating cash flow trends could alleviate near-term liquidity concerns.

- Successful acquisition or licensing deals augmenting materials or software portfolios might accelerate adoption curves.

- Resolution outcomes surrounding ongoing SEC investigations or export control compliance would reduce legal overhang mitigating stock volatility.

Investors should watch quarterly order intake patterns especially large contract wins within healthcare or aerospace customers given seasonality effects reported historically skewed toward year-end spend bursts [S5][S24].

Returns & Capital Allocation

Empirical return metrics reflect a business still recovering from prior restructuring phases:

- An approximate return on equity near 12.4% in FY2025 implies cautious improvement after extended periods of losses eroding shareholder value [F1].

- Negative free cash flow approximating $(97.7)$ million signals investments outpacing operational cash generation requiring external financing or balance sheet adjustments [F1].

- Liquidity stood relatively robust with cash & equivalents at about $95.6 million versus current liabilities near $120.6 million yielding a current ratio of roughly 2.87 providing short-term buffer though continual monitoring needed against covenant terms on convertible notes [$92M principal at end-2025] owed by 2030 [F1][S22][S27].

No dividends or share repurchase programs are mentioned arguing reinvestment prioritization over shareholder payouts amid earnings recovery effort [F1][N1]. Prudent capital deployment appears focused on R&D sustaining the patent portfolio which numbered 854 issued patents worldwide at year-end up from previous counts revealing sustained IP buildout driving competitive differentiation [S26].

Sector-Specific Considerations (Analysis)

Additive manufacturing markets are characterized by rapid technological evolution risking product obsolescence absent continuous innovation—a challenge mitigated somewhat by 3D Systems’ sizable R&D commitments and diversified technology platforms allowing multiple entry points across plastics/metal/wax/bioprinting modalities enabling cross-sector application flexibility.

Material science breakthroughs remain critical since proprietary materials often dictate part performance influencing customer lock-in given embedded certification requirements especially relevant in regulated healthcare device markets.

Software intelligence increasingly integrates fleet-wide printer management optimizing uptime essential for industrial-scale deployments contrasting earlier single-machine prototyping use cases empowering higher throughput economies.

Growing sustainability mandates encourage adoption of additive methods promoting waste reduction versus traditional subtractive machining complementing corporate social responsibility narratives vital for reputation-sensitive aerospace and medical industries.

Risks & Challenges Summary

Significant risks identified include:

- Macroeconomic headwinds impacting capital spending decisions of key clients aggravated by elevated interest rates tightening financing availability [S14][S19].

- Concentrated customer base particularly within healthcare segment posing credit risk threats if large clients reduce orders or payment delays emerge leading to impaired receivables affecting profitability & liquidity [S14].

- Legal exposures linked to export controls violations disclosures resolved recently but continuing regulatory scrutiny including an SEC investigation imposing financial costs/distraction risks impacting operational focus [S8][S12][S17].

- Product quality fluctuations given technical complexity causing warranty claims potentially harming reputation & future sales [S7][S28].

- Potential covenant breaches related to note indentures could force accelerated debt repayment challenging refinancing options under unfavorable terms threatening solvency if unaddressed [S22][S27].

- Global expansion introduces currency risks coupled with political instability scenarios necessitating robust risk management strategies for overseas operations [S14][S17].

- Intellectual property litigation costs remain an unknown variable possibly diverting resources from core innovation efforts affecting competitive positioning over time [S15].

Conclusion

3D Systems Corp occupies a pivotal niche within the evolving additive manufacturing landscape driven by its comprehensive ecosystem approach melding hardware innovations with material science expertise plus software intelligence tuned for scalable production workflows primarily focused on healthcare and industrial applications. Despite patchy historical financial performance marked by substantial operating losses compounded by negative free cash flows constraining capital allocation flexibility, recent narrowing losses alongside management’s articulation of application-led scale-up offer signs of strategic progress.

Ongoing macroeconomic uncertainties combined with notable customer concentration and demanding debt covenant parameters underscore continuing execution risks warranting vigilant liquidity monitoring along with clear milestone tracking related to new product commercializations and expansion into volume production realms.

Investors closely following this company should prioritize updates on order volumes especially within large healthcare accounts plus quarterly cash flow evolution while integrating assessment of how legal/regulatory developments alongside supply chain resilience translate into sustainable profitability enhancements over coming periods.

This report is based solely on publicly available information cited herein ([F1], [N#], [S#]) without any projection beyond confirmed data points or speculative assumptions regarding future financial performance or valuation levels.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments