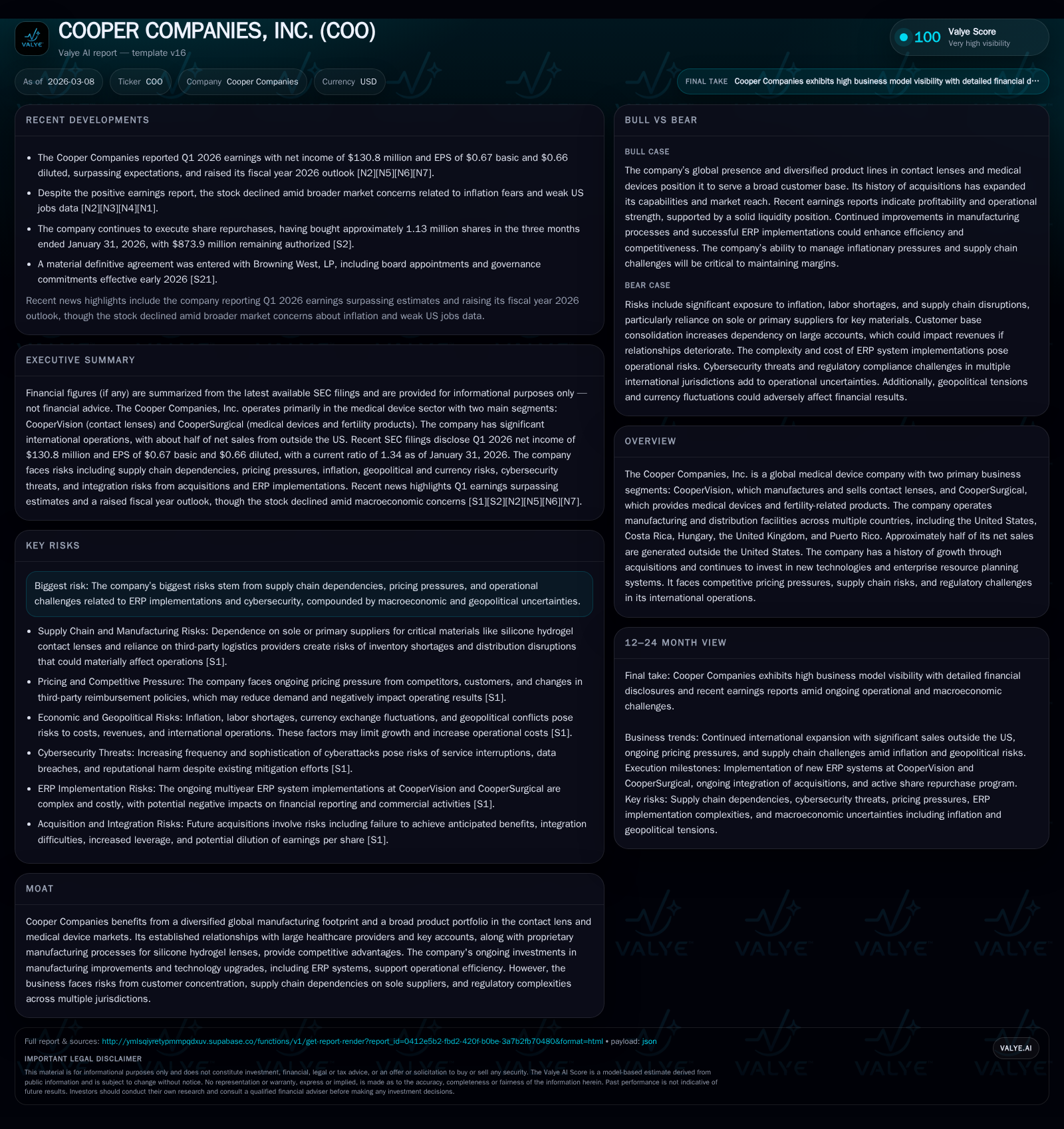

Cooper Companies Balances Global Expansion and Regulatory Challenges with Strategic Capital Deployment

The company exhibits resilient operating cash flow generation amid modest net income pressure and intensifying market headwinds.

Cooper Companies, Inc. operates through its two main segments—CooperVision for contact lenses and CooperSurgical for medical and fertility products—generating roughly half of its sales internationally. Recent years show steady operating income growth until a slight decline in FY2025, reflecting pricing pressures and operational costs. The firm continues investing in manufacturing capabilities and ERP upgrades to support global scale, while facing risks from supply chain dependencies and regulatory complexity across geographies. Capital allocation emphasizes share repurchases with no dividends paid recently, supporting shareholder returns amidst evolving macroeconomic challenges. Future growth hinges on innovation, integration of acquisitions, and navigating geopolitical and regulatory environments.

Company Overview

The Cooper Companies, Inc. is a global medical device firm comprising two synergistic business segments: CooperVision specializing in contact lens manufacture and sales, and CooperSurgical offering a portfolio of surgical devices along with fertility-related products [N2][S1]. Its manufacturing footprint is geographically diverse—facilities in North America (U.S., Puerto Rico), Europe (Hungary, U.K.), Latin America (Costa Rica), and smaller international sites underpin approximately half its net sales generated outside the U.S. [S1][S6].

This distribution supports resilience against localized disruptions but introduces complexity in managing regulatory compliance across multiple jurisdictions.

Historical Financial Performance

Financially, CooperCompanies experienced top-line expansion with solid increases in operating income through FY2023 before confronting minor contraction by FY2025. Specifically, operating income peaked at $705.7 million in FY2024 before declining 3.2% to $682.9 million in FY2025 [F1]. Net income followed a similar pattern—rising notably from $294.2 million in FY2023 to $392.3 million in FY2024 then retreating to $374.9 million in FY2025 (-4.4% YoY) [F1].

Operating cash flows displayed robust growth (12.2% YoY) to $796.1 million in FY2025 despite pressures on margins [F1]. Capital expenditure outlays moderated by 14% to $362.4 million reflecting a maturation phase of heavy investments in manufacturing capacity expansion and technology upgrades [F1]. Equity has grown steadily corresponding with retained earnings and operational performance.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 375 | 796 | 683 | 362 | -4.4% |

| 2024 | 392 | 709 | 706 | 421 | +33.3% |

| 2023 | 294 | 608 | 533 | 393 | -23.7% |

| 2022 | 386 | 692 | 508 | 242 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 0 | 290 | 434 |

| 2024 | 0 | 0 | 288 |

| 2023 | 3 | 0 | 215 |

| 2022 | 3 | 79 | 450 |

Source: SEC companyfacts cache [F1].

Table: Key Financial Metrics for Cooper Companies (USD millions). Operating Income YoY reflects percentage changes where data permits.

Two noteworthy shifts stand out: the jump in operating income between FY2023-24 driven by productivity gains post large-scale ERP investments; and renewed share repurchase activity amounting to $290 million executed in FY2025 after no buyback spend during prior two years [F1][S28]. No dividends were distributed post FY2023 indicating a capital return strategy favoring stock repurchases.

Operational Drivers of Growth

CooperVision's competitive advantage derives from proprietary silicone hydrogel contact lens technology coupled with efficient global manufacturing footprint stretching over multiple continents [S9][S26]. This product line remains subject to price competition but benefits from differentiated product features.

CooperSurgical focuses on surgical instruments and fertility care innovations supported by a network of U.S.-centered manufacturing sites alongside some European operations [S21]. The segment capitalizes on growing fertility treatment demand globally though it faces complex regulatory landscapes for new medical devices approvals especially within the EU Medical Devices Regulation (MDR) regime and analogous frameworks abroad.

Acquisitions remain integral to growth strategy as the company seeks complementary technologies and expanded addressable markets [S7]. Integration risks are managed but remain material due to complexities involving IT systems synchronization (including ERP environment upgrades), personnel harmonization, regulatory compliance alignment, and intellectual property protections [S7][S17].

Risks Constraining Growth Potential

Pricing Pressure: Both divisions operate within competitive landscapes where customers increasingly consolidate buying power—large healthcare providers negotiate aggressively on pricing which compresses margins [S6][S9]. New pricing schemes include capitated contracts designed to control overall health system costs that may limit ability to increase list prices even amid inflationary cost rises.

Supply Chain Vulnerabilities: Sole-source supplies for critical materials used especially for silicone hydrogel lenses expose production continuity risks [S9][S26]. Additionally acute labor shortages at certain plants amplify capacity management challenges.

Geopolitical & Regulatory Complexity: Approximately half revenue originating outside the U.S implies exposure to foreign currency fluctuations, tariffs escalation risk, import-export restrictions including sanctions regimes compliance responsibilities [S15][S16]. Regulatory approval delays or failures impose direct revenue impact while ongoing compliance demands consume resources [S14][S18], particularly environmental regulations (EU REACH etc.) as well as evolving ESG disclosure requirements recognized across jurisdictions [S22]. Privacy regulations governing personally identifiable information (PII), including protected health information related to fertility services also add layers of operational risk [S19][S21].

Cybersecurity is another growing concern as heightened attack sophistication could disrupt IT systems critical for manufacturing and customer management [S21]. Failure or breaches could cause costly remediation expenses alongside reputational damage.

Customer Concentration Risks: Consolidation among healthcare customers concentrates revenue streams creating potential vulnerability should major account relationships deteriorate unexpectedly or contract terms worsen abruptly [S6].[N1]

Outlook / What to Watch For (Analysis)

Explicit forward financial guidance was not detailed within the referenced quarterly filings or earnings calls but management raised fiscal year outlooks post Q1 beat suggesting confidence given order trends and pipeline execution despite cautious macro backdrop [N1][N2]. Investment focus persists on factory automation enhancements along with continued rollout of enterprise resource planning platform modules intended to optimize cross-segment data integration efficiencies.

Market watchers should observe:

- Progress on regulatory clearances particularly within European markets affected by MDR/IVDR updates.

- Supply chain resiliency progress including supplier diversification efforts.

- Pricing contract dynamics involving large hospital networks.

- Impact of inflationary cost trends versus price pass-through capability.

- Acquisition cadence balanced against integration effectiveness.

- Cybersecurity program maturity given increasing threat environment.

Capital Allocation Profile

CooperCompanies demonstrates disciplined free cash flow generation underpinning capital return policies focused on stock repurchase programs rather than dividends presently [F1][S28]. Nearly $291 million was repurchased during FY2025 building upon no buybacks prior years except a small allocation in FY2022 [$78M] [F1]. Dividends have been nominal or nil since FY2023 indicating prioritization of buybacks as preferred means of returning capital.

ROE based on FY2025 net income ($374.9M) over equity reported ($8.24B) approximates a modest ~4.6%, reflective partly of considerable intangible assets from acquisitions diluting returns measure while leveraging solid cash flow translates into shareholder-friendly capital deployment.[F1]

Conclusion

The Cooper Companies stands as a diversified medical device player with broad product portfolios fortified by proprietary technology leadership especially within contact lenses alongside a growing surgical/fertility platform supported by targeted acquisitions. The geographic diversity provides growth opportunities offset by concomitant risks from supplier dependence, regulatory environments spanning multiple jurisdictions, escalating pricing pressures from consolidated customers, inflationary cost headwinds, cyber threats, plus geopolitical uncertainties affecting trade flows.

Financially the company has demonstrated capability to grow operating cash flow even amid earnings volatility while favoring share repurchases over dividends as a method for capital returns demonstrating management confidence about long-term value creation pathways contingent on continued innovation execution coupled with prudent cost control.

Investors should monitor integration progress post-acquisitions along with external macro-financial conditions influencing healthcare procurement behavior worldwide as key factors shaping performance trajectory longer term.

This report is prepared solely for informational purposes reflecting data available through early March 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments