Goliath Film & Media Holdings Struggles With Financial Sustainability Despite Niche Focus

Goliath Film & Media Holdings maintains a specialized approach targeting underserved niche content but faces persistent financial challenges and liquidity constraints.

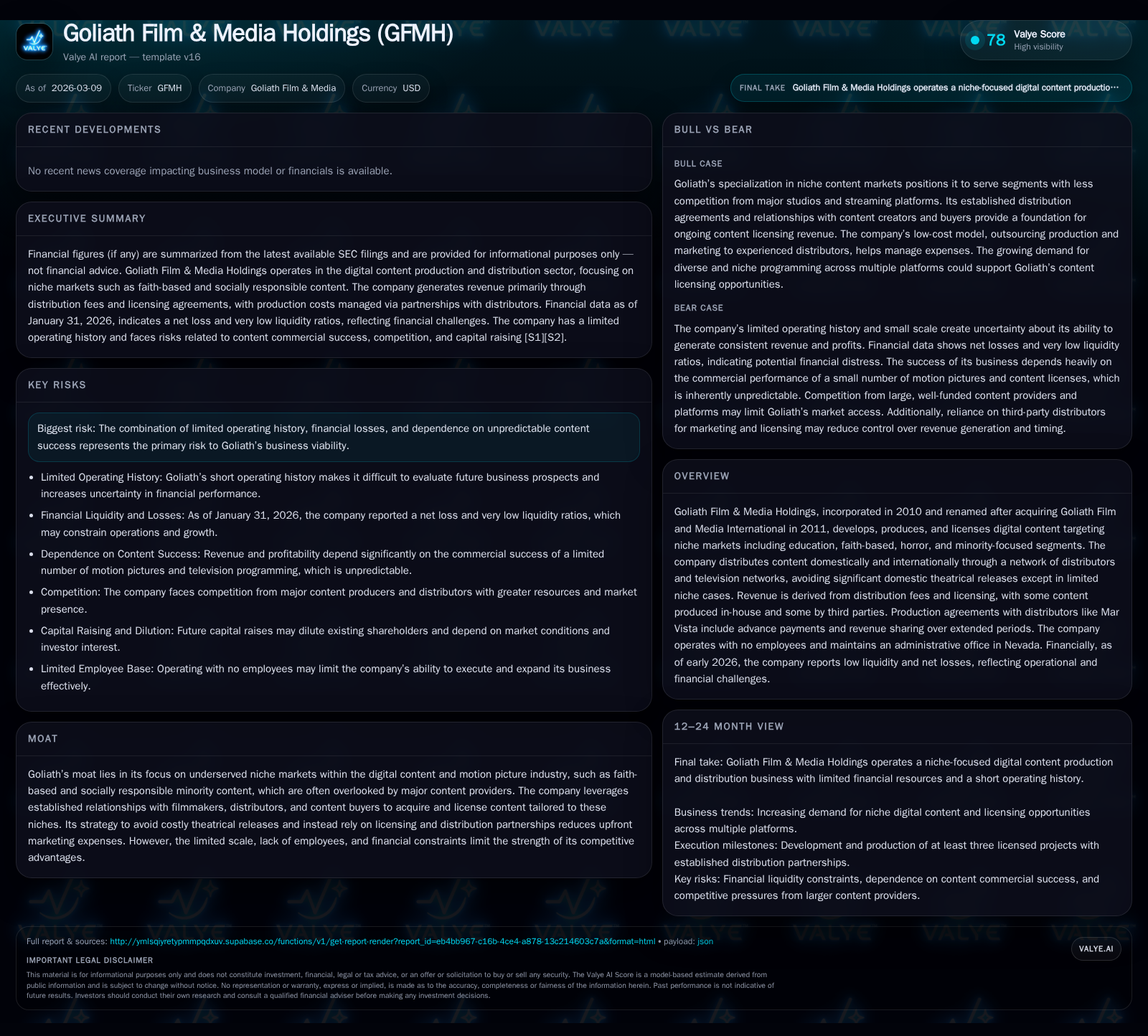

Goliath Film & Media Holdings centers its strategy on producing and licensing niche digital content, including faith-based, horror, and minority-focused films. While this approach fills gaps overlooked by major studios, the company has experienced flat revenues around $250K since 2017 and volatile net income patterns, swinging between losses and occasional profits but overall operating cash flow deficits. Its capital structure exhibits acute stresses with scant liquidity and negative equity. Management plans to develop several new projects leveraging distribution partnerships, yet operational risks from an employee-light model and unpredictable content success continue to limit growth prospects. Monitoring future licensing achievements and improvements in financial footing will be key to assessing Goliath's viability.

Historical Performance: Revenue Plateau and Earnings Volatility

Goliath Film & Media Holdings has demonstrated a long-standing stagnation in top-line revenue, maintaining roughly $250,000 annually since FY2017 (fiscal year ending April) as per consolidated reporting [F1]. Earlier revenue was lower at $175,000 in FY2016 before settling into this plateau. The company's operating income mirrors this static revenue with significant volatility; while there was a substantial operating profit of approximately $76,569 in FY2023, this was flanked by net losses including -$95,579 in FY2022 and -$37,332 in FY2025 [F1]. Net income closely tracks operating income due to limited non-operating factors.

Operating cash flows consistently remain negative throughout these years, highlighting cash burn despite nominal revenue levels — from -$22,821 in FY2022 to about -$16,831 in FY2025 [F1]. This pattern suggests that Goliath's recurring costs and investment activities exceed cash inflows generated by licensing fees and distribution revenue. Such earnings volatility reflects the inherent unpredictability tied to content performance within motion picture licensing streams.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -37332 | -16831 | -37332 | -9327.3% |

| 2024 | -396 | -4977 | -396 | -100.5% |

| 2023 | 76569 | -4962 | 76569 | +180.1% |

| 2022 | -95579 | -22821 | -95579 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 27.1 |

| 2024 | 0.4 |

| 2023 | -76.4 |

| 2022 | 54.1 |

Source: SEC companyfacts cache [F1].

Note: Operating Income YoY % compares latest FY versus prior year using absolute changes when possible. Revenue stable since FY2017.

Niche Markets and Business Model Mechanics

The cornerstone of GFMH’s corporate strategy is its strict focus on underserved niche segments of the digital content industry: specifically education-oriented programming; faith-based films targeting largely Bible Belt or “flyover country” audiences; horror genre features; and socially conscious minority-targeted productions [S1][S6][S7][S8]. This segmentation responds to market gaps ignored by major studios that typically concentrate on mass-market tentpole releases.

Unlike typical domestic theatrical launches which incur prohibitive marketing expenses and four-wall release logistics—where theaters are rented outright for screenings—Goliath explicitly avoids wide theatrical distribution except for rare cases framed as limited events geared toward targeted audiences [S7]. Instead, it relies on distribution agreements that emphasize licensing rights sales domestically and internationally through established third-party distributors like Mar Vista Entertainment.

Such partnerships provide upfront advance payments generally around $125K-$175K per project while obligating Goliath to share approximately 30%-35% of gross proceeds from distribution for periods extending up to 25 years [S7][S8]. Marketing fees are almost entirely borne by distributors rather than the company itself. Production costs for projects hover near $150K each [S6], representing substantial investment relative to the subdued top line. By outsourcing marketing responsibilities and leveraging third-party fee structures for licensing agreements and gross proceeds sharing arrangements rather than front-loading advertising spend internally, GFMH reduces upfront risk exposure but also limits immediate upside participation.

Current Financial Health: Liquidity Concerns and Leverage

As of January 31, 2026—the latest balance sheet date—the company reported current assets amounting to only around $1,477 versus bleak current liabilities tallying approximately $165,954 [F1][S3][S4]. This produces an extraordinarily low current ratio of about 0.01 underscoring dire liquidity constraints. In practical terms, short-term obligations outstrip available liquid resources more than one hundredfold.

Such a balance sheet imbalance points toward acute financial distress and foreshadows potential solvency challenges unless addressed rapidly through capital infusions or restructuring. Management acknowledges the need for future equity or debt offerings which may dilute existing shareholders substantially or burden the capital structure further with expensive liabilities [S4][S9]. The company currently holds negative equity nearing -$137K indicative of accumulated losses exceeding contributed capital [F1].

Since GFMH trades on OTC Bulletin Board with limited liquidity itself [S9], attracting favorable financing terms remains uncertain amid pressing working capital needs. The tightness of its financial position hampers operational flexibility as well as potential investments into new content pipelines or marketing expansion that might spur growth.

Capital Allocation: Cash Flow Challenges and Equity Deficits

From a returns perspective—while nominal net income occasionally swings positive—the fundamental weakness manifests starkly in ongoing negative operating cash flow figures extending multiple years [F1]. There have been no recorded dividend payments or share repurchases historically nor does management indicate plans for such capital returns given persistent resource constraints [S9].

A superficially positive return on equity metric approaching ~27% calculated via trailing twelve-month net income divided by negative equity is misleading; it primarily reflects a balance sheet distortion rather than sustainable profitability or effective capital deployment [F1]. Without cash flow generation sufficient to finance ongoing operations or reduce liabilities organically, equity capital restoration relies almost exclusively on external financing events which carry inherent dilution risks

Free cash flow similarly fails to show meaningful positive conversion after accounting for capex adjustments referenced in SEC disclosures emphasizing modest per-project investments capped near $150K each [F1][S6]. This inability to self-fund growth initiatives constrains agility within shifting market dynamics.

Future Growth Opportunities Within Underserved Segments

Looking ahead, management articulates intentions to develop at least three new content projects over the next twelve months utilizing existing distributor relationships for licensing monetization [S6][S7][S13]. By continuing to outsource production—thus capping fixed costs—and relying on advance payouts coupled with gross proceeds sharing agreements structured with entities like Mar Vista Entertainment, Goliath aims to incrementally build its catalog aligned with niche audience demand.

Industry trends underscore increasing segmentation within home entertainment platforms where dozens of cable/satellite specialty channels coexist alongside proliferating streaming services hungry for diverse programmatic content . The company's positioning as a supplier focused on neglected niches—such as immigrant cultural groups beyond Spanish-speaking communities—is intended to capitalize on growing fragmentation absent from mainstream Hollywood pipelines [S13].

Nevertheless,the success of these growth plans will depend heavily on securing advantageous licensing deals swiftly post-production completion (which can take six-to-nine months), achieving meaningful scale across multiple releases without escalating fixed cost burdens beyond limited internal headcount capabilities [S6][S7].

Constraints on Expansion: Operational and Market Risks

Inherent operational challenges compound GFMH's financial fragility. The company operates without employees directly onboard managing day-to-day activities; its administrative functions are minimalistic based out of Nevada office facilities [S17]. This lean structure limits scalability and rapid responsiveness compared to competitors with dedicated in-house production or marketing teams capable of agile content development cycles.

Market risks stemming from unpredictable consumer reception further exacerbate uncertainty. As highlighted extensively in risk disclosures [S1][S5][S20], the commercial performance of any individual film can decisively impact periodic earnings given limited diversification across catalogs and reliance on variable licensing revenues.

Compliance overheads tied to public reporting—including adherence to Sarbanes-Oxley internal control mandates despite lack of attestation requirements for smaller reporting companies—increase administrative strain draining management resources away from strategic priorities [S4][S20]. Economic volatility globally introduces additional uncertainty affecting discretionary consumer spending on entertainment content consumption.

What to Watch: Milestones and Strategic Inflection Points

Given the absence of explicit company-issued earnings forecasts or milestone timelines beyond vague production plans noted in disclosures [S6][S7], investors should monitor the following indicators as barometers of GFMH’s trajectory:

- Successful acquisition of licensing agreements for upcoming projects within stipulated timelines post-production completion (next 6-12 months).

- Improvement in liquidity ratios driven by advance payments or external financing reducing working capital deficits.

- Restoration or stabilization of shareholder equity through future capital raises ideally at favorable terms minimizing excessive dilution.

- Development or announcement of additional strategic partnerships expanding distribution networks beyond core collaborators like Mar Vista.

- Regulatory changes affecting niche content distribution economics or competitive responses from larger streaming platforms targeting similar audiences.

These factors will signal whether Goliath can materially leverage its niche positioning toward sustainable growth despite pervasive sector headwinds and historic financial instability.

This analysis synthesizes all referenced SEC filings and financial data specific to Goliath Film & Media Holdings without speculation beyond documented evidence. It does not constitute investment advice nor endorsement but aims to provide a thorough understanding of operational mechanics juxtaposed against prevailing financial challenges confronting the company within its specialized digital content domain.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments