Q32 Bio Advances Biologics Pipeline with Bempikibart Fast Track, Posts Turnaround Profit in 2025

Clinical-stage biotech Q32 Bio registers its first profitable year driven by product divestiture and progresses lead candidate towards commercialization.

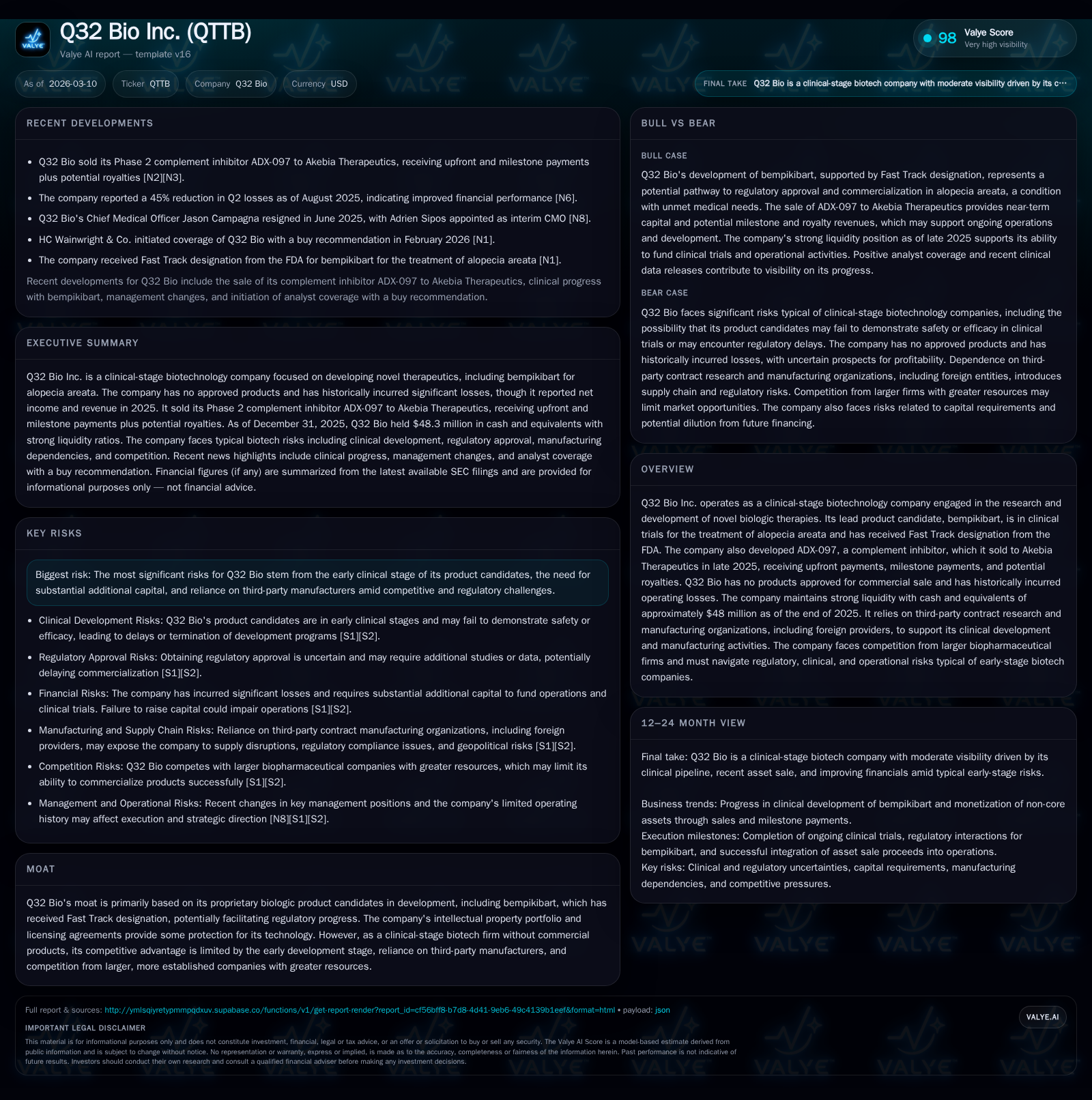

Q32 Bio Inc., a clinical-stage biotechnology company, achieved a significant financial turnaround in 2025 with positive operating and net income following years of losses. This shift was primarily driven by upfront and milestone payments from the sale of its complement inhibitor asset ADX-097 to Akebia Therapeutics. The company’s lead biologic candidate, bempikibart, focused on alopecia areata, attained FDA Fast Track designation, underlining regulatory momentum. Despite these advances, Q32 Bio faces typical clinical-stage risks, including reliance on third-party manufacturers, regulatory uncertainties, and substantial ongoing cash burn. Monitoring upcoming clinical milestones for bempikibart and potential new collaborations will be key to its growth trajectory.

Overview

Q32 Bio Inc., operating as a clinical-stage biotechnology company, has anchored its strategic focus on developing novel biologic therapies targeting autoimmune indications. Its flagship product candidate is bempikibart, an investigational biologic therapy designed for alopecia areata (AA), a distressing autoimmune condition characterized by non-scarring hair loss. The U.S. Food and Drug Administration (FDA) has granted this agent Fast Track designation as of April 2025, signaling an intent to expedite development and review processes for serious conditions addressing unmet medical needs [S25].

Significantly, Q32 Bio divested another experimental drug candidate—ADX-097, a complement system inhibitor—soon before the end of 2025. This transfer to Akebia Therapeutics provided the company with upfront payments upon closing and potential milestone payments plus royalties contingent on future commercial success [N1], [S1]. Currently, Q32 Bio holds no approved drugs on the market and stands firmly focused on clinical advancements.

Historical Performance and Financial Turnaround

From a financial perspective, Q32 Bio demonstrated a notable transformation in fiscal year (FY) 2025 compared with prior years steeped in heavy net losses largely tied to ongoing R&D expenditures without revenue generation.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 54 | 30 | -34 | 17 | +162.5% |

| 2024 | 0 | -48 | -68 | -66 | +57.7% |

| 2023 | -113 | -96 | -101 | -2157.0% | |

| 2022 | -5 | -114 | -133 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -34 | 71.0 |

| 2024 | -68 | -841.1 |

| 2023 | -96 | -154.8 |

| 2022 | -115 | -2.8 |

Source: SEC companyfacts cache [F1].

Q32 Bio's financial shift is remarkable as revenue surged from zero in FY2024 to $53.7 million in FY2025 primarily reflecting payments related to the divestiture of ADX-097 [F1].

Operating income swung dramatically into profitability at $16.9 million in FY2025 compared with steep losses exceeding $66 million the year prior; net income followed suit with positive earnings of nearly $30 million despite persistent negative cash flows from operations reflecting continued high R&D expenditures underlying pipeline development [F1]. Capital expenditures remain negligible suggesting focus on leveraging third-party manufacturing rather than infrastructure buildup [F1].

Equity rose from approximately $5.7 million at end-2024 to $42 million at end-2025 resulting in a calculated trailing return on equity of roughly 71% based on net income vs equity—a meaningful recovery metric in biotech turnaround context [F1]. Liquidity remains robust with about $48 million cash and equivalents posting a current ratio around 4.85 supporting resilience amidst ongoing investments [F1].

Drivers Behind Past Growth

The principal catalyst behind Q32 Bio’s recent financial improvement stems from its deal to outlicense ADX-097 late in the year preceding December 31, 2025 [S3], [N1]. This transaction injected upfront funds plus contractual milestones, effectively introducing tangible revenue streams replacing earlier periods dominated by grant financing or capital raises.

On the clinical front, Q32 Bio’s bempikibart program progressed well enough through initial studies to secure FDA Fast Track status early in the year—an important marker from regulators enhancing development speed prospects for therapies addressing sizeable unmet medical needs such as alopecia areata [S25].

The company's operational model relies heavily on partnerships with third-party contract research organizations (CROs) and contract manufacturing organizations (CMOs), including overseas service providers—a common approach among lean biotechnology firms that reduces fixed assets but elevates risk sensitivity around vendor performance and supply chain integrity [S10], [S21].

Growth Prospects and Industry Context

Looking ahead, Q32 Bio’s main growth driver remains successful development and eventual approval of bempikibart across multiple geographic markets including the U.S., Europe, and potentially Asia-Pacific regions if pursued [S26]. Alopecia areata presents a substantial addressable market segment given limited therapeutic options currently available; success here could unlock significant commercial opportunity assuming regulatory clearance and reimbursement acceptance.

Nonetheless, there are clear caps on near-term growth posed by several factors:

- The company currently has no marketed products or direct commercial infrastructure requiring it either to partner or build go-to-market capabilities post-approval—both expensive endeavors fraught with execution risk.

- Intense competition exists from large biopharma companies engaged in autoimmunity research who possess deeper resources for late-stage trials and commercialization efforts.

- Regulatory frameworks continue evolving notably around pricing controls especially outside the U.S., potentially suppressing achievable sales revenues even post approval [S6], [S24], [S25].

- Bempikibart remains investigational meaning significant trial advancement hurdles remain before any approval or launch is possible.

Additional pipeline diversification beyond bempikibart would be vital for sustainability; however post-divestment of ADX-097 that aspect appears limited today until new candidate selections materialize [N1], [S1].

Forecasts, Milestones & Expectations

While explicit forward guidance is not reported publicly within the provided documents for FY2026 or beyond [N1], key milestones to watch include:

- Completion of ongoing or planned pivotal trials evaluating bempikibart’s safety/efficacy profile in alopecia areata patients.

- Regulatory filings anticipated following successful trial outcomes which would transition the company closer to commercialization rights exercise.

- Potential announcements regarding new licensing partnerships or collaborations leveraging their biologic platform.

Liquidity levels support runway into continued clinical efforts but further financing may be required pending trial progress or strategic decisions involving business model evolution [S17], [F1]. Close observation will be required around quarterly updates regarding timing of trial readouts plus capital raises.

Returns & Capital Allocation Dynamics

Unlike many pre-revenue biotech peers historically incurring losses from prolonged R&D spends without offsetting revenues, Q32 Bio's positive net income for FY2025 yields an uncommon return profile (approximately 71% ROE based on net income over equity) indicative mostly due to one-time transactional inflows rather than sustainable operating profits derived from commercial sales activities [F1].

Operating cash flow remains negative $33.5 million while capital expenditure is negligible highlighting ongoing funding consumption intensiveness despite profitable accounting results driven by licensing fees realized upfront rather than recurrent customer revenue streams [F1]. The gap between positive net income yet negative cash flow denotes non-cash gains likely associated with accounting treatment of asset sales or milestone revenue recognition timing.

No dividends or stock buyback programs were announced nor expected at this stage given the company's investment back into clinical programs—the standard paradigm for early-stage biotechs reliant primarily on reinvestment rather than shareholder distributions [F1], [S17].

Risks & Operational Challenges Summary

Per disclosures within SEC filings:

- Developmental risk: Late-stage clinical failures or safety issues remain material threats that could derail bempikibart approval hopes.

- Manufacturing risk: Heavy dependence on third-party contract manufacturing organizations introduces supply consistency exposure along with geopolitical and regulatory hurdles especially given ongoing tensions impacting international supply chains.

- Competitive risk: Established pharma players could release competing therapies or biosimilars potentially eroding market share.

- Regulatory & pricing risk: Compliance burdens across global jurisdictions add complexity; price caps especially outside U.S., impact margins adversely.

- Financial risk: Although liquidity sits soundly today, sustained cash burn necessitates either future capital raises or partnership monetization strategies.

In addition to operational risks typical across early-stage biotech space, Q32 Bio must navigate intellectual property challenges pertaining to patent coverage breadth and enforceability as well as potential infringement disputes common within competitive biologics domains [S18], [S31–37]. Compliance costs related to healthcare laws are high due to intricate regulations governing pharmaceutical marketing activities across various territories including anti-kickback statutes and data privacy laws impacting clinical trial data management and promotional conduct [S24], [S9].

Conclusion

Q32 Bio embodies the dynamic profile of a clinical-stage biopharmaceutical enterprise executing a transition from developmental losses into profitability territory bolstered by strategic asset monetization combined with targeted pipeline prioritization centered on bempikibart for alopecia areata—the firm’s most advanced candidate garnering Fast Track designation from the FDA.

This pivot demonstrates how early biotech innovators leverage licensing deals coupled with focused clinical programs as dual levers toward sustainability ahead of product approvals/commercial launches.

Future value creation depends critically upon navigating clinical development risks successfully while preparing operational frameworks either through partnerships or own buildout for eventual commercialization steps amid stiff competition and evolving regulatory/pricing environments globally. Monitoring progress against bempikibart clinical milestones alongside management’s strategy toward broader pipeline expansion or additional transactions will be essential indicators shaping Q32 Bio’s medium-term outlook.

This analysis is prepared solely for informational purposes based on publicly available corporate reports filed with the U.S. Securities and Exchange Commission (SEC) and third-party news sources as referenced herein up to March 10, 2026, without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments