Rapport Therapeutics Strengthens Pipeline and Commercial Reach with RAP-219 Expansion

Clinical-stage biopharma Rapport accelerates development of RAP-219 backed by a strategic China partnership and substantial liquidity amid rising operating losses.

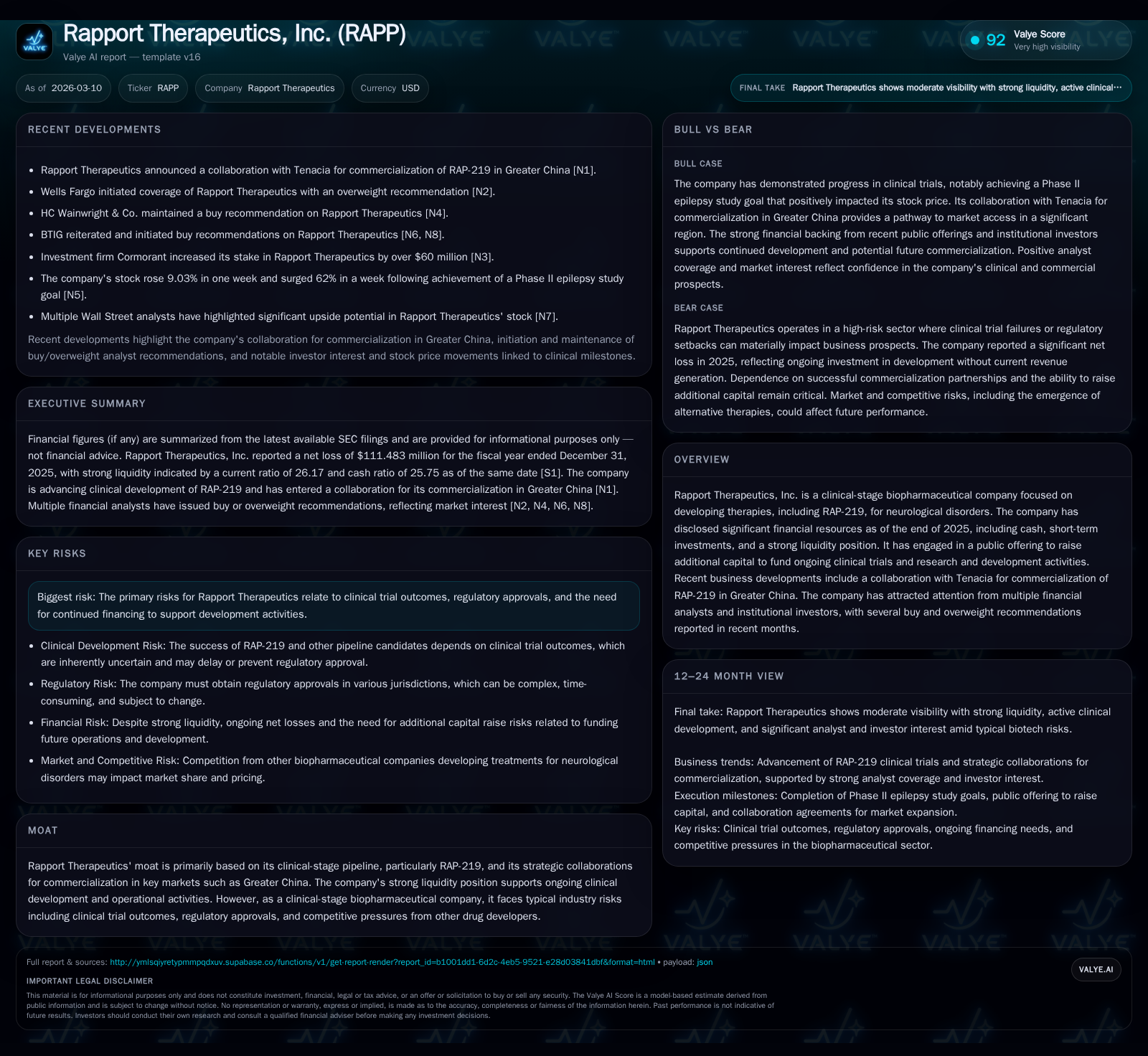

Rapport Therapeutics has intensified its focus on RAP-219, its lead clinical-stage candidate targeting neurological disorders, by securing a commercialization collaboration with Tenacia in Greater China. This expansion complements the company’s strong cash position and liquidity, enabling sustained R&D investment despite widening operating losses and negative cash flows. Investor optimism is reflected in recent analyst overweight ratings, though risks remain tied to clinical outcomes and regulatory approvals.

Financial Performance Trends Highlight Rising Operating Burdens

Rapport Therapeutics’ financials for FY2024 and FY2025 reveal an increasingly pronounced cost structure consistent with a clinical-stage biopharmaceutical company advancing late-phase development. Operating income deteriorated by over 50% year-over-year from -$83.1 million to -$125.1 million as R&D spend escalated to support RAP-219 trials [F1]. This steep rise in operating loss was mirrored by net income falling from -$78.3 million to -$111.5 million (a drop of approximately 42%) signaling growing expenses outpacing any offsetting revenue streams, typical for companies still pre-commercialization.

Operating cash flow (CFO) similarly showed significant pressure, plunging nearly 35% from -$64.8 million in FY2024 to -$87.5 million in FY2025, emphasizing an expanding cash burn rate driven primarily by increased trial activity and associated general & administrative costs [F1]. Capital expenditures reduced markedly by over 70%, indicative of minimal investment in fixed assets or infrastructure, consistent with a focus on drug development rather than physical expansion.

Robust liquidity stands out as a notable strength with a current ratio above 26 as of year-end 2025 reflecting $498.6 million in current assets versus only $19 million in current liabilities [F1]. Cash and equivalents totaled $52.6 million providing immediate operational runway coupled with substantial short-term investments disclosed elsewhere . Equity growth of roughly 58.7% to $484.7 million suggests successful capital raises that have fortified the balance sheet amid heavy spending.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -111 | -87 | -125 | 1 | -42.4% |

| 2024 | -78 | -65 | -83 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1000 | -88 | -23.0 |

| 2024 | 4000 | -67 | -25.6 |

Source: SEC companyfacts cache [F1].

Note: Cash & Equivalents data not available for FY2024.

RAP-219: The Core Driver Behind Strategic Collaborations and Future Prospects

At the heart of Rapport Therapeutics’ pipeline is RAP-219, a candidate focused on treating complex neurological disorders — an area marked by high unmet need but substantial clinical development risk . The company’s recent agreement with Tenacia for commercialization rights in Greater China represents a strategic out-licensing move designed to leverage local expertise for regulatory approval pathways and regional market penetration [N1].

Such partnerships are standard practice among emerging biotechs seeking to mitigate geographical market entry costs and accelerate patient access without fully internalizing commercialization overheads. Particularly in Asia’s heterogeneous regulatory environments, collaborations like this can materially expand potential revenue streams if clinical programs yield positive data.

RAP-219’s trajectory will be critical to future top-line growth given that no other late-stage assets currently anchor the portfolio . The firm remains reliant on successful trial results and eventual regulatory approvals to translate its R&D investments into commercial success.

Capital Allocation Priorities Support Clinical Advancement Amid Losses

The company’s capital allocation clearly prioritizes supporting its operating burn linked to accelerating trial phases over tangible asset investments or shareholder distributions. Capital expenditures dropped sharply from $2.4 million in FY2024 to just $616 thousand in FY2025 [F1], reinforcing that spending is predominantly channeled into clinical R&D rather than infrastructure.

Meanwhile, reported stock buybacks are virtually non-existent ($1 thousand) reflecting a stance focused on preserving liquidity for near-term operational needs rather than returning capital [F1]. Approximately negative 23% return on equity calculated from FY2025 net loss over shareholder equity reflects an investment phase profile typical for pre-revenue biopharma entities absorbing upfront costs without corresponding earnings [F1].

The sizable cash position alongside record equity infusions supports an extended runway facilitating ongoing trial efforts including planned advancements for RAP-219 . The public offerings referenced provided necessary funding buffers amid the negative free cash flow environment.

Evaluating Near-Term Milestones and Market Expectations for RAP-219

Explicit numeric guidance or definitive development milestones have not been disclosed publicly; however, analyst coverage signals expectations for material forward catalysts linked to clinical progress [N2]. Industry-standard benchmarks would include pivotal trial data releases or regulatory feedback from agencies governing neurological indications.

Wells Fargo’s recent initiation of coverage with an overweight recommendation underscores institutional confidence that near-term inflection points may justify valuation uplift despite current losses [N2]. Investors should monitor updates regarding RAP-219’s clinical endpoints achievement timelines as well as any extension of commercial agreements replicating the Greater China model across other territories.

Risk Factors Tied to Clinical Development and Regulatory Approvals

As outlined comprehensively in SEC filings [S1][S2], Rapport faces headwinds inherent to clinical-stage biopharmaceuticals: unpredictability of trial outcomes that govern progression or termination decisions; stringent regulatory review processes with variable timing; competition from larger players targeting similar neurological segments; and the necessity for recurrent capital raises until commercial revenues emerge.

These risk vectors underscore the volatile nature of early drug development ventures where scientific promise does not always translate into commercial viability . Additionally, dependence on external partners such as Tenacia to execute commercialization increases reliance on counterparties' performance aligned with corporate strategy.

Investor Sentiment Reflected in Recent Analyst Coverage and Equity Activity

Despite challenging financial metrics highlighted by deepening losses (-50.6% operating income decline year-over-year) and expanding negative cash flows (~35%), capital markets demonstrate constructive receptivity toward Rapport's narrative centered around RAP-219’s promise [F1][N2].

The overweight initiation by Wells Fargo illustrates that key institutional investors weigh pipeline strength and strategic collaborations heavily enough to offset near-term financial drag [N2]. The company's ability to raise equity capital successfully also signals investor willingness to fund ongoing development rather than penalize short-term profitability challenges.

In synthesis, Rapport Therapeutics exemplifies a biotech entity navigating the high stakes balance between investment-heavy drug development phases and cultivating long-term value through targeted partnerships for international commercialization amid persistent operational losses.

This analysis is based solely on information provided from company disclosures and publicly available news articles as of March 10, 2026. It does not constitute investment advice or recommendations but aims to present an integrated view combining quantitative financial details with qualitative strategic insights relevant to stakeholders evaluating Rapport Therapeutics’ business trajectory.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments