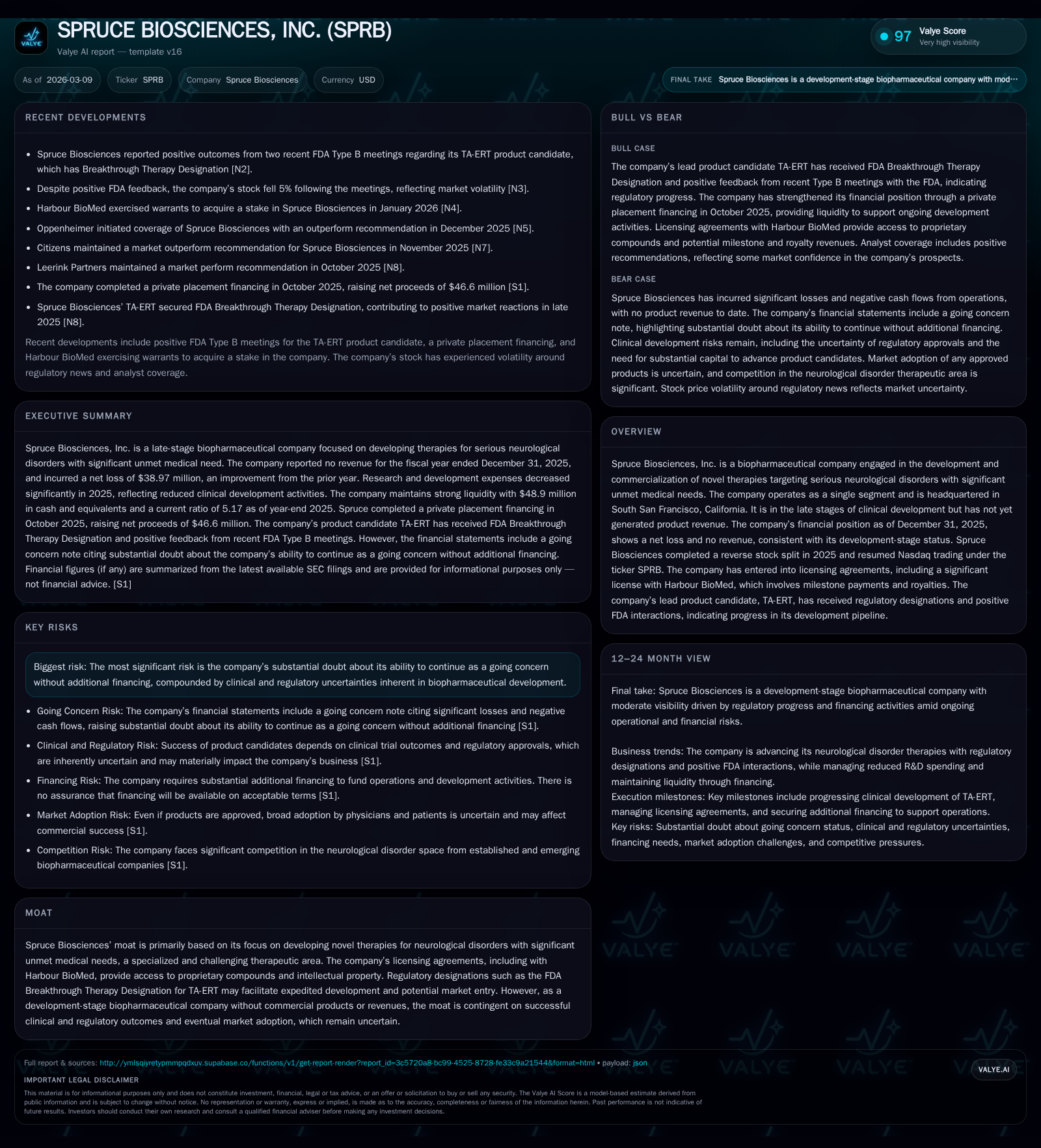

Spruce Biosciences Faces Revenue Collapse and Intensifying Cash Constraints Amid Late-Stage Neurological Therapy Development

The company’s 2025 financials reveal zero revenue, substantial losses, and pressing liquidity challenges as it advances TA-ERT toward regulatory approval.

Spruce Biosciences, a late-stage biopharmaceutical firm focused on novel neurological treatments, saw its revenue vanish in 2025 following earlier collaborative income in prior years. Operating losses narrowed compared to 2024 but remain substantial, accompanied by significant negative cash flow from operations. Despite positive regulatory engagement for its lead candidate TA-ERT, the company’s future hinges on access to new financing to sustain operations beyond the next year. Licensing agreements and regulatory designations provide strategic assets but also embed milestone-related financial obligations with uncertain timing.

Historical Financial Performance

Spruce Biosciences has operated as a development-stage biopharmaceutical company focused exclusively on therapies targeting severe neurological disorders with unmet medical needs. The company has not yet commercialized any products and correspondingly reported no revenues for the full-year period ending December 31, 2025.

In detail, revenue collapsed completely from $4.9 million in fiscal year (FY) 2024 to zero in FY2025, reflecting the cessation or conclusion of prior collaboration payments typical of companies transitioning fully into late-stage clinical development [F1]. Despite this top-line contraction, operating losses narrowed significantly by about 35%, from nearly -$56.2 million to -$36.5 million [F1]. This was driven primarily by cutbacks in clinical development spending as well as workforce reductions executed during early 2025.

Net losses followed a similar pattern improving from -$53 million in FY2024 to close to -$39 million for FY2025 [F1]. The company’s operating cash flow usage demonstrates better cash conservation—with cash burn declining from -$56 million in FY2024 to approximately -$33 million for FY2025—this improvement reflects operational efficiencies but remains a material outflow given lack of product-generated cash inflow [F1][S1]. Capital expenditures were nil in FY2025 following minimal outlays historically.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -39 | -33 | -37 | -100.0% | +26.5% |

| 2024 | 5 | -53 | -56 | -56 | -51.3% | -10.7% |

| 2023 | 10 | -48 | -33 | -52 | -3.8% | |

| 2022 | -46 | -42 | -47 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -91.7 | |

| 2024 | -56 | -184.0 |

| 2023 | -33 | -62.6 |

| 2022 | -42 | -67.4 |

Source: SEC companyfacts cache [F1].

Financials shown in USD thousands; data sourced from SEC filings and company facts [F1]

Future Growth Prospects

Spruce’s pipeline is notably anchored on TA-ERT (tralesinidase alfa enzyme replacement therapy) targeting Sanfilippo Syndrome Type B (MPS IIIB), a rare lysosomal storage disorder lacking approved therapies. The compound benefits from FDA Breakthrough Therapy Designation which may expedite clinical development and review processes—a key differentiator given the challenging regulatory environment for neurological orphan diseases [N2][N3]. Positive FDA Type B meetings documented suggest constructive regulatory dialogue around clinical plans and data requirements.

The company also holds licensing agreements such as with Harbour BioMed providing access to investigational assets coupled with milestone obligations that could fuel future pipeline expansion if successful but also represent contingent liabilities on financial flexibility [S1]. Previous collaborations with firms like Eli Lilly contribute foundational IP rights but also embed deferred milestone payments subject to development success.

The principal growth drivers will be successful enrollment completion of pivotal trials for TA-ERT and securing regulatory approvals leading to first-time product commercialization. Secondary factors include potential out-licensing deals or partnerships leveraging their licensed technologies.

Risks include the inherent clinical trial uncertainties common across biotech—especially rare diseases with small patient numbers—and financial constraints that may limit trial scale or speed without fresh capital influxes [S23][N2]. Patent litigations present additional uncertainty especially regarding European intellectual property protections critical for commercial strategy abroad [S15][S20].

Forecasts and Milestones

While detailed forward guidance is limited due to standard clinical-stage operational opacity and unpredictability of regulatory decisions, observable near-term milestones include:

- Achievement of key regulatory milestones attached to debt tranches under Avenue Capital facility dependent on progress with TA-ERT’s IND/clinical phases completion [S10].

- Continuation of pivotal Phase III or late-stage studies aiming for new drug application (NDA) submission timelines influenced partly by FDA guidance outcomes experienced positively recently [N2][N3].

- Monitoring patent proceedings outcomes notably against Neurocrine Biosciences impacting freedom-to-operate particularly in European markets is critical ahead of commercial launch preparations [S15][S20].

Returns and Capital Allocation

ROE is deeply negative at approximately -92%, unsurprisingly reflecting negative net income against modest equity accumulated primarily through financings rather than earnings retention (Net Income / Equity: -38.97M / $42.52M = ~ -91.7%) [F1]. The firm remains unprofitable given its stage.

Cash flow usage remains focused on R&D advancement with no dividends or stock buybacks owing to tight liquidity requirements and developmental priorities. Recent capital raises have been material: a $50 million private placement closed October 2025 substantially replenished capital along with a $15 million term loan funded January 2026 under strict financial covenants requiring regular milestone achievements [S25][S10]. These funds are necessary but still insufficient for long-term self-sufficiency per management commentary expressing substantial doubt about continuing as a going concern absent further financing within the next year [S5][S25].

Employee stock purchase plans and equity incentive plans remain active tools for talent retention amid workforce reduction completed mid-2025; no share repurchase programs or dividends are authorized or contemplated currently [S12][S19].

Operational and Strategic Highlights

Spruce underwent significant restructuring including a workforce reduction of approximately 55% in April-May 2025 aimed at reallocating resources toward accelerating TA-ERT development efforts—a sign of targeted prioritization amidst cost containment pressures outweighing broader pipeline breadth expansion ambitions [S25]. The reverse stock split (1-for-75) executed during mid-2025 was necessary due to Nasdaq non-compliance with minimum bid prices and was essential for regaining exchange listing status under ticker SPRB with enhanced institutional investor access potentials [S8].

Legal proceedings relating to patent disputes introduced uncertainty and accrued liabilities nearing $2 million signal potential capital drainage risk if unfavorable outcomes emerge; ongoing monitoring is recommended given litigation complexities taking place both at United Kingdom Patent Court level and Unified Patent Court jurisdictional domains [S15][S29].

The company maintains a single reporting segment focusing solely on development/commercialization of its neurological disorder therapies with concentrated R&D expenditure patterns predominantly devoted to clinical trial advancement costs captured within operating expenses—these represent pass-through fees paid to CROs plus manufacturing expenses per contract accrual procedures familiar among biopharma peers focusing on orphan disease indications with complex trial logistics constraints [S21][S23].

Industry Context Analysis (Non Company-Specific)

Neurological orphan diseases such as Sanfilippo Syndrome suffer decades-long treatment voids due to scientific challenges crossing blood-brain barriers compounded by limited patient pools hindering traditional large-scale trials—thus FDA's breakthrough therapy designations are crucial facilitators encouraging risk-tolerant investments despite inherent commercial scale limitations. Commercial pathways increasingly depend on expedited regulatory reviews coupled with robust pricing scenarios often involving payers’ complex evidence demands given ultra-orphan status nature.

Successful entry into this domain commands not just clinical efficacy but intellectual property fortification managing global patent portfolios strategically since European markets involve fragmented patent court structures as evidenced here with Neurocrine litigation impacts posing tangible barriers alongside ongoing R&D innovation imperatives.

What To Watch

Given absent explicit forward financial guidance outside milestone triggers tied mostly to debt tranches noted around regulatory endpoints (e.g., Tranche #2 & #3 financing dependent on MPS IIIB study results) investors and analysts should monitor:

- Clinical trial enrollment trends and principal investigator feedback centered on TA-ERT efficacy/safety signals,

- Upcoming FDA communications or advisory panel scheduling related to orphan drug marketing authorizations,

- Regulatory developments concerning patent challenges especially any European rulings,

- Quarterly cash burn rates alongside utilization reports from recent financings,

- Updates on collaboration arrangements renegotiations or new licensing deals which could improve runway or dilute equity base.

These factors collectively drive Spruce’s near-to-medium term viability trajectory.

Disclaimer: This analysis is based solely on publicly disclosed information as of March 9, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments