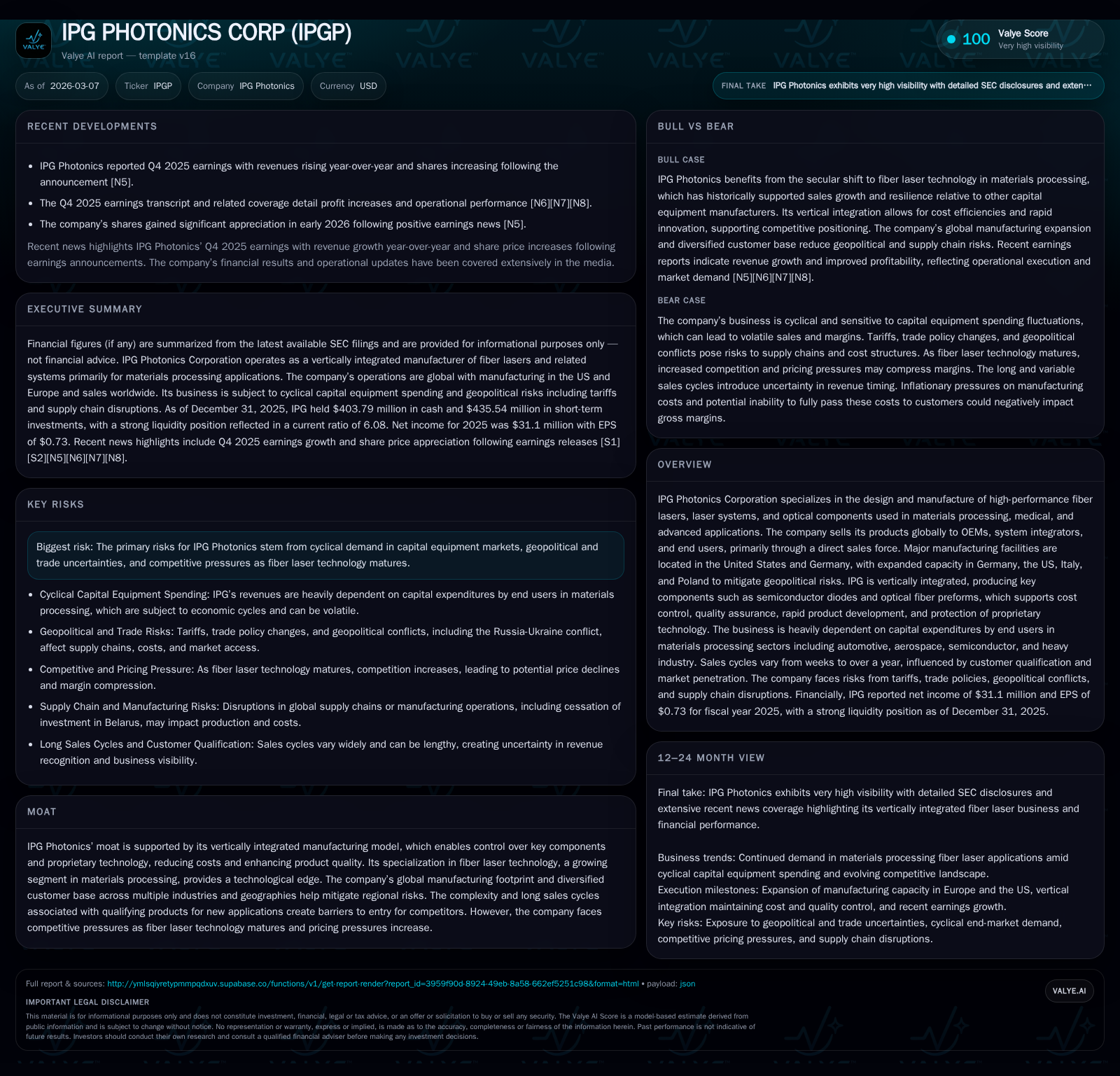

IPG Photonics Rebounds: Revenue Growth and Operational Recovery Fuel Prospects

IPG Photonics achieved a robust financial turnaround in 2025, driven by growth in fiber laser demand and strategic manufacturing expansion.

In 2025, IPG Photonics posted a significant recovery from prior-year losses with a 28.9% revenue increase and over 100% operating income growth, reflecting rebound demand in its fiber laser systems. The company’s vertical integration and diversified manufacturing footprint underpin resilience amid competitive pressures and trade uncertainties. Despite lower free cash flow and moderated capital returns, IPG's operational leverage and expanding global capacity position it for sustained competitiveness in maturing industrial laser markets.

From Negative to Positive: IPG Photonics’ Recent Financial Turnaround

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 31 | 75 | 13 | 79 | +117.1% |

| 2024 | -182 | 248 | -208 | 99 | -182.9% |

| 2023 | 219 | 296 | 232 | 110 | +99.1% |

| 2022 | 110 | 213 | 170 | 110 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 53 | -3 | 1.5 |

| 2024 | 344 | 149 | -9.0 |

| 2023 | 223 | 186 | 9.1 |

| 2022 | 500 | 103 | 4.6 |

Source: SEC companyfacts cache [F1].

IPG Photonics navigated a stark reversal from heavy losses in fiscal 2024 to a positive earnings stance in 2025. The company reported revenues of approximately $361 million for the year ended December 31, 2025, an increase of about 28.9% compared to the previous year’s downturn [F1]. This top-line surge signals reacceleration in demand for its fiber lasers across key materials processing end markets.

More notable is the operating income swing—from a substantial loss of nearly $208 million in FY24 to an operating profit of $13.1 million in FY25—equating to an over-100% improvement year-over-year [F1]. Net income followed the same resurgence pattern, moving from a material deficit of $181.5 million to a positive net of $31.1 million (117.1% increase) [F1]. These gains reflect not only cyclical recovery inherent in capital equipment industries but also structural resilience underpinned by IPG’s vertically integrated model.

Quarterly earnings trends confirmed this trajectory with recent quarters beating consensus on both revenue and operational metrics [N4][N5], reinforcing confidence in the core business momentum.

Drivers of Revenue Expansion and Margin Dynamics in Fiber Laser Products

The revenue expansion ties closely to growing adoption of fiber laser technology within materials processing sectors such as automotive, aerospace, semiconductors, and heavy industry—accounting for roughly 86-88% of total sales volumes according to management commentary [S18].

IPG’s unit economics hinge on nuanced pricing strategies that blend volume discounting for large OEM orders with tiered pricing based on product complexity and power levels [S4][S6][S7]. Higher power devices requiring more optical components benefit from superior fixed overhead absorption—driving economies of scale—and typically command elevated margins owing to technical differentiation.

Yet these strengths are offset by persistent inflationary pressures on raw materials including electronic components and metal parts, compressing gross margin if price increases cannot be fully passed on [S4][S7]. Additionally, pricing erosion is observed as products mature within increasingly contested markets where competitive intensity accelerates [S7][S9].

Margins for systems—which incorporate lasers and complementary optical sub-systems—often run below standalone laser devices due to configuration complexity and volume considerations [S4]. Managing production scale carefully relative to forecast sales remains crucial; overexpansion risks diluting fixed cost absorption if throughput does not keep pace [S13]. The interplay among product mix shifts, volume discounts, inflationary input costs, and residual trade tariffs shape margin volatility.

Geopolitical Risk Management: Diversifying Manufacturing Footprint

As detailed in company disclosures, IPG has proactively diversified its manufacturing across major sites in the United States, Germany, Italy, and Poland—a direct strategic response to geopolitical risk factors including ongoing Russia-Ukraine conflict repercussions impacting Belarus operations [S23][S25].

This capacious network supports vertical integration — producing key components internally from semiconductor diodes through optical fiber preforms — affording control over quality, costs, product development speed, and protection against external supply chain disruptions.

By outsourcing former Belarusian mechanical component supply chains to qualified third parties while expanding alternate capacities elsewhere, IPG mitigates sanction-related vulnerabilities and tariff-induced friction points prevalent in global trade recently [S25]. Such flexibility enhances production scheduling agility—a core moat element preserving operational continuity amid volatile international environments.

Capital Allocation Approach Amid Cash Flow Variability and Returns

Despite improved profitability and operating stability in FY25, capital allocation exhibited caution reflective of underlying cash flow challenges.

Operating cash flow contracted nearly 70%, falling from about $248 million in FY24 down to roughly $75 million FY25; this sharp decrease underscores influences such as working capital build or ongoing R&D spend affecting cash conversion cycles unfavorably despite earnings recovery [F1]. Concurrently capital expenditures were pared by approximately one-fifth YoY—from about $98.5 million down to close to $79 million—consistent with measured capacity investment aligned with market demand visibility [F1].

Free cash flow registered slightly negative territory (~$-3.45 million), constrained by the gap between cash inflows from operations versus outflows invested back into property plant & equipment [F1]. Meanwhile share repurchases dropped substantially—from over $344 million in FY24 down to ca. $53 million—signaling prudence amidst liquidity variability despite earlier aggressive buyback programs aimed at capital return optimization [F1][S5].

Return on equity approximated a modest ~1.5%, tied both to incremental earnings gains juxtaposed against stable equity base enlargement plus working capital absorption dynamics restraining efficiency ratios at present [F1].

This measured capital deployment stance balances sustaining operational scale with preserving financial flexibility amid cyclicality inherent in capital equipment sectors.

Competitive Landscape and Technology Maturity Impacting Growth Trajectory

The fiber laser market dynamics IPG faces reflect sector maturation marked by intensifying price competition as incumbent technologies become standard offerings rather than disruptive innovations [S7][S18].

While entry barriers remain enforced by complex qualifying cycles needed for OEM/system integrator acceptance—which can extend months or longer—end-market capex sensitivity introduces volatility into order pipelines influencing periodic sales fluctuations [S18].

The trend toward commoditization exerts downward pressure on average selling prices requiring evolving pricing tactics balancing market penetration objectives against margin preservation.

However, sustained expertise enabled by vertical integration combined with continuous product innovation preserves differentiation versus challengers relying solely on outsourced components or less integrated models.

What Investors Should Monitor: Product Innovation and Market Penetration Milestones

Key upcoming milestones include verification cycles for new product certifications particularly targeting higher-growth adjacent applications such as medical device integration or semiconductor wafer processing lasers—areas expected to broaden addressable markets beyond traditional industrial materials processing segments [N3][N4][S3].

Additionally noteworthy is ongoing patent litigation related to intellectual property protection upheld recently via Unified Patent Court rulings in Germany; outcomes here may influence competitive positioning or necessitate operational adjustments depending on enforcement scales [S3].

R&D investments remain pivotal catalysts for pipeline expansion; metrics around commercialization success rates relative to spend will illuminate future growth capacity amid mature tech trends.

Finally, evolution of global pricing strategy implementation—particularly regarding unit volume concessions balanced against inflation-driven cost upticks—and management’s effectiveness at navigating geopolitical risks through factory footprint adjustments deserve continuous scrutiny given their direct impact on margin profiles.

This analysis is based solely on publicly available information as of early March 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments