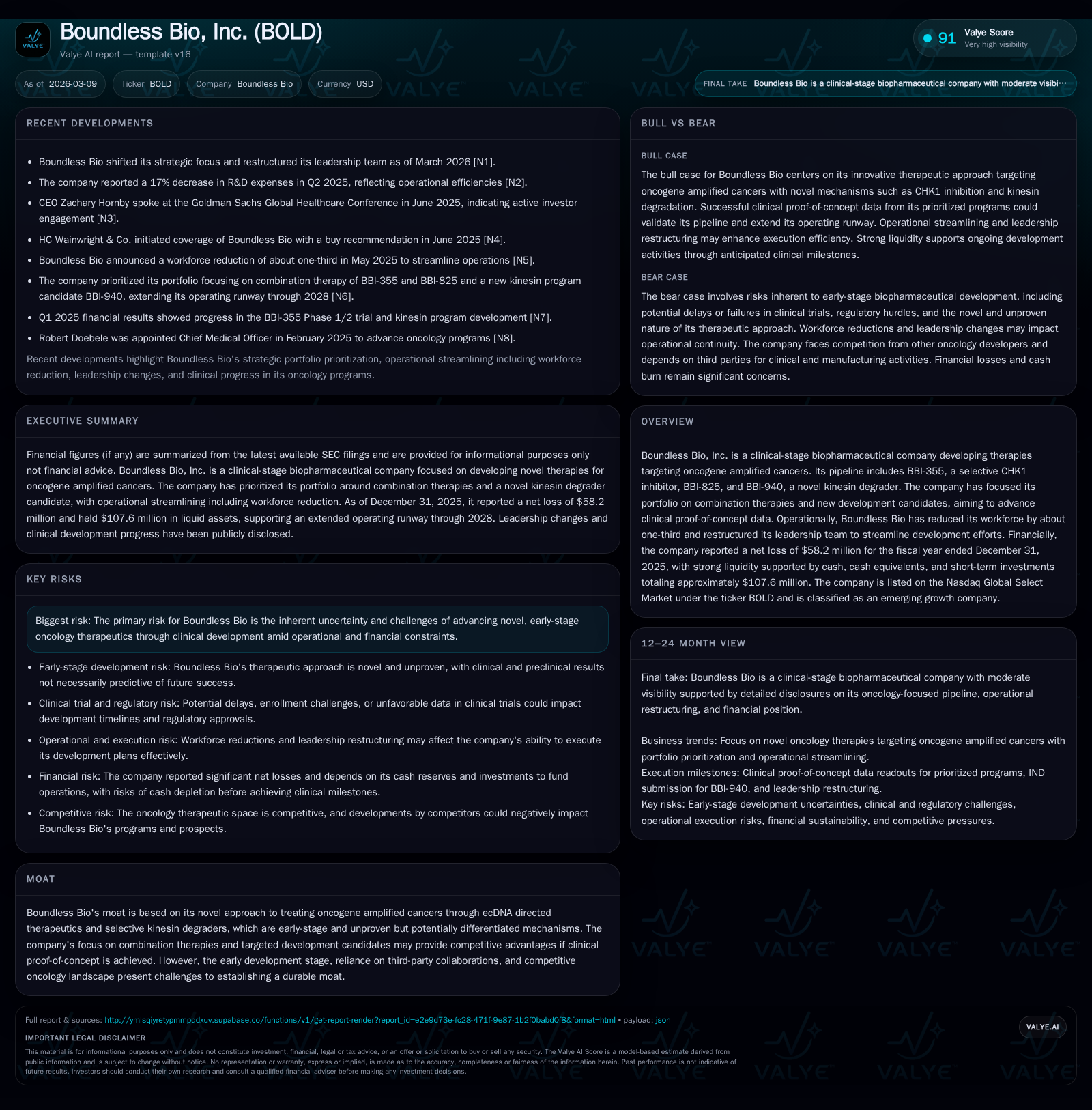

Boundless Bio’s Transition: Refining Oncology Focus with Novel Therapeutics and Leaner Operations

Boundless Bio recalibrates its clinical-stage oncology development through selective pipeline prioritization, operational streamlining, and capital preservation.

In 2025, Boundless Bio advanced its strategy focusing on innovative therapies targeting oncogene amplified cancers, particularly through its selective CHK1 inhibitor BBI-355 and kinesin degrader BBI-940. The company undertook significant workforce reductions and leadership restructuring to sharpen its focus on combination therapies. Financially, while operating and net losses narrowed year-over-year, the company sustains strong liquidity positioned to fund clinical proof-of-concept milestones anticipated in the near term. Key risks persist from early-stage development challenges and competitive dynamics in oncology.

Historical Performance and Key Financial Trends Underpinning BOLD’s Evolution

Boundless Bio's financial trajectory throughout FY2024 and FY2025 exhibits incremental progress typical for clinical-stage biotech companies striving to manage burn while advancing novel therapeutics. Operating income losses contracted by 13.3% year-over-year from a $73.3 million deficit in FY2024 to $63.6 million in FY2025 [F1]. Similarly, net income losses narrowed by approximately 11%, registering a net loss of $58.2 million in FY2025 compared to $65.4 million the prior year [F1]. This favorable trend reflects management’s execution on portfolio prioritization designed to reduce low-conviction programs and concentrate resources.

Operating cash flow outflows also saw a significant reduction of 23.3% YoY ($60.8M down to $46.7M), signaling an improved efficiency in cash deployment relative to progress made clinically [F1]. Capex dropped steeply by 78.5%, from $2.54 million down to just $0.55 million, illustrating capital discipline consistent with a tactical shift away from resource-intensive exploratory activities toward targeted late-preclinical or early clinical-stage development [F1]. The net effect is a clearer alignment between spending and near-term proof-of-concept goals.

Despite the ongoing losses, the company's balance sheet strength remains notable, underpinned by robust liquidity metrics — current assets totaled approximately $109.6 million versus only $12.5 million in current liabilities yielding a current ratio of 8.74 as of December 31, 2025 [F1]. Equity declined proportionally following accumulated net losses; however, it stood near $98.7 million at year-end [F1]. Consequently, ROE remains negative around -59%, which aligns with industry norms for pre-revenue oncology biotechs heavily investing in R&D ahead of commercial opportunities [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -58 | -47 | -64 | 1 | +11.0% |

| 2024 | -65 | -61 | -73 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -47 | -59.0 |

| 2024 | -63 | -43.4 |

Source: SEC companyfacts cache [F1].

This progression illustrates Boundless Bio’s strategic refocus balancing innovation risk with financial stewardship.

Pipeline Advances Centered on Selective CHK1 Inhibition and Kinesin Degradation

The company’s core scientific proposition revolves around developing targeted therapeutics against oncogene amplified cancers leveraging two pioneering mechanisms: selective CHK1 inhibition via BBI-355 and targeted kinesin degradation exemplified by BBI-940.

BBI-355 is undergoing Phase 1/2 evaluation in the POTENTIATE trial as a selective checkpoint kinase 1 (CHK1) inhibitor aiming to exploit replication stress vulnerabilities prevalent in oncogene-amplified tumor contexts [S14][N1]. However, continuous every-other-day (Q2D) dosing exposed a narrow therapeutic index due primarily to hematological toxicity observed near clinically active dose levels — a limiting factor that led the company to discontinue further single-agent development under this regimen [S14][S20].

Recognizing these constraints, Boundless Bio pivoted toward combining BBI-355 with BBI-825 — a ribonucleotide reductase (RNR) inhibitor previously shelved following unfavorable pharmacokinetics when dosed alone [S20]. Preclinical data suggest synergistic cytotoxicity emerges from this novel/novel combination leveraging intermittent dosing schedules that may mitigate overlapping toxicities allowing sustained anti-tumor activity [S14][S20]. Initiation of clinical development for this combination took place during 2025 with initial proof-of-concept data expected within the company’s cash runway horizon [N1][S14].

Separately, the kinesin program addresses an undrugged target involving DNA segregation including extrachromosomal DNA (ecDNA) propagation during mitosis—a mechanism integral to oncogene amplification maintenance [S16]. Oral selective degraders such as BBI-940 have demonstrated robust activity in preclinical tumor models leading Boundless Bio to select it as lead candidate ahead of an Investigational New Drug (IND) filing intended in H1 2026 [N1][S16]. Clinical proof-of-concept readouts for BBI-940 are viewed as key inflection points that could validate this novel approach if safety and efficacy signals align favorably [N1][S16].

Together these molecules illustrate the company's emphasis on mechanistically differentiated modalities within combination frameworks tailored for genetically defined cancer cohorts.

Operational Restructuring: Workforce Reduction and Leadership Streamlining

In parallel with clinical and pipeline recalibrations, Boundless Bio implemented organizational changes aimed at enhancing operational agility and conserving capital [N1][S15]. A decisive workforce reduction eliminated about one-third of employees primarily during Q2 2025, accompanied by leadership team reshuffles effective March 2026 [N1][S15].

Though incurring one-time severance-related expenses approximating $1.2 million primarily recorded in Q2 2025 [S15], these measures align workforce capacity more closely with core therapeutic priorities — namely advancing BBI-355/BBI-825 combinations alongside BBI-940 [N1]. The company acknowledges potential retention risks but underscores that this leaner structure should accelerate decision-making processes while optimizing resource allocation [N1].

This operational streamlining reflects a common biotech lifecycle transition where scale is moderated post-discovery phase toward efficient clinical execution.

Clinical Proof-of-Concept: What Upcoming Milestones Reveal About Future Growth

Boundless Bio has articulated several upcoming milestones that serve as pivotal catalysts underpinning future growth narratives [N1][S14][S16]. First among these is the anticipated IND submission for BBI-940 during the first half of calendar year 2026 [S16], marking entry into clinical testing of their kinesin degrader platform.

Concurrently, efforts to generate initial proof-of-concept data from the BBI-355/BBI-825 combination trial remain focal [N1][S14]. This data generation window is tightly linked to regulatory feedback responsiveness from FDA regarding trial designs and enrollment pacing amidst efforts to optimize therapeutic index parameters [S14].

Given the early clinical stage positioning combined with prior challenges encountered around dose-limiting hematological toxicity [S20], investors should monitor not only safety/efficacy signals but also operational execution such as trial enrollment rates and regulatory communications which could significantly affect pace and ultimate viability [N1][S14].

These milestones collectively frame a cautiously optimistic outlook hinging on validating novel mechanisms within difficult-to-drug oncogene amplified targets.

Capital Allocation Review: Cash Position, Burn Rate, and Return Metrics

As of December 31, 2025, Boundless Bio reported cash & equivalents totaling approximately $17.9 million with overall current assets at approximately $109.6 million against current liabilities of roughly $12.5 million — yielding a solid current ratio of about 8.74 indicating ample short-term liquidity cushions [F1][S10].

The company disclosed total liquidity including cash equivalents and short-term investments of approximately $138.3 million as of March 31, 2025 earlier in filings reflecting runway expectations extending into the first half of 2028 aligned with anticipated critical clinical readouts [N1][S16].

Capital expenditures were minimized sharply (-78.5%) reflecting tactical deferral of non-essential fixed asset investments amid portfolio focus tightening [F1]. Operating losses moderated but remained elevated given ongoing heavy investment in R&D (-$63.6M operating loss for FY2025), which translates into negative approximate return on equity at -59% due to accumulated deficits offsetting shareholder capital base [F1][S10].

No dividends or share repurchases have been undertaken; given clinical-stage status these remain consistent with sector norms whereby capital is prioritized toward sustaining innovation pipelines rather than returning cash flow prematurely [S23], reinforcing prudent capital stewardship through patient value creation lenses.

Risk Profile in a Competitive Oncology Landscape

Boundless Bio confronts multiple layers of risk inherent both to its scientific approach and operational environment [S4][S6][N1].

The novelty of its ecDNA-directed therapies—particularly kinesin degraders—introduces uncertainties around translational biology validity and clinical predictability uncommon among more established targets [S14][S20]. This platform immaturity coupled with narrow therapeutic indices evident in early CHK1 inhibitor trials exposes vulnerability to unexpected toxicities or inadequate efficacy outcomes that could stall advancement or necessitate costly reformulations [S7].

Furthermore,the reliance on third-party collaborators for manufacturing and trial execution adds logistical complexity susceptible to external disruptions impacting timelines [S14]. Regulatory hurdles loom large given FDA scrutiny especially because combination regimens incorporating investigational agents often encounter intricate approval pathways requiring comprehensive safety datasets [S4].

Additionally,the competitive oncology sector features multiple players developing cell cycle inhibitors or degraders along various mechanisms raising potential commoditization risks or rapid scientific obsolescence if rival platforms demonstrate superior performance before Boundless Bio's assets achieve de-risked status [N1].

Operational transformations also introduce retention uncertainty for key scientific talents mitigating experiential continuity essential for complex drug development processes [N1][S15].

These risks collectively underscore the challenging pathway typical for emerging growth biopharmaceutical firms embarking on novel therapeutic frontiers.

Analyst Perspectives Following Recent Buy Ratings

Despite outlined challenges,Broker reports published February 13th have upgraded Boundless Bio shares based principally on perceived differentiation inherent to the company’s scientific strategy vis-à-vis mainstream approaches[N2]. Analysts cite confidence that successful demonstration of safety/tolerability improvement via novel dosing schemas as well as induction of ecDNA kinetochore disruption will validate high-value niche targeting unaddressed by competitors[N2].

However,buy recommendations remain tethered tightly to execution milestones —clinical data timelines key—and tempered continuously by financial runway adequacy considerations alongside sector-level risk awareness[N2]. Thus,the positive analyst consensus appears balanced between enthusiasm for groundbreaking science coupled prudently with cognizance of typical early stage biotech investment volatility[N2].

This analysis synthesizes publicly available SEC filings and market disclosures without providing investment advice or price guidance. The unique challenges surrounding early-stage oncology drug development warrant cautious appraisal beyond quantitative metrics alone while acknowledging upside potential tied closely to near-term data inflections.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments