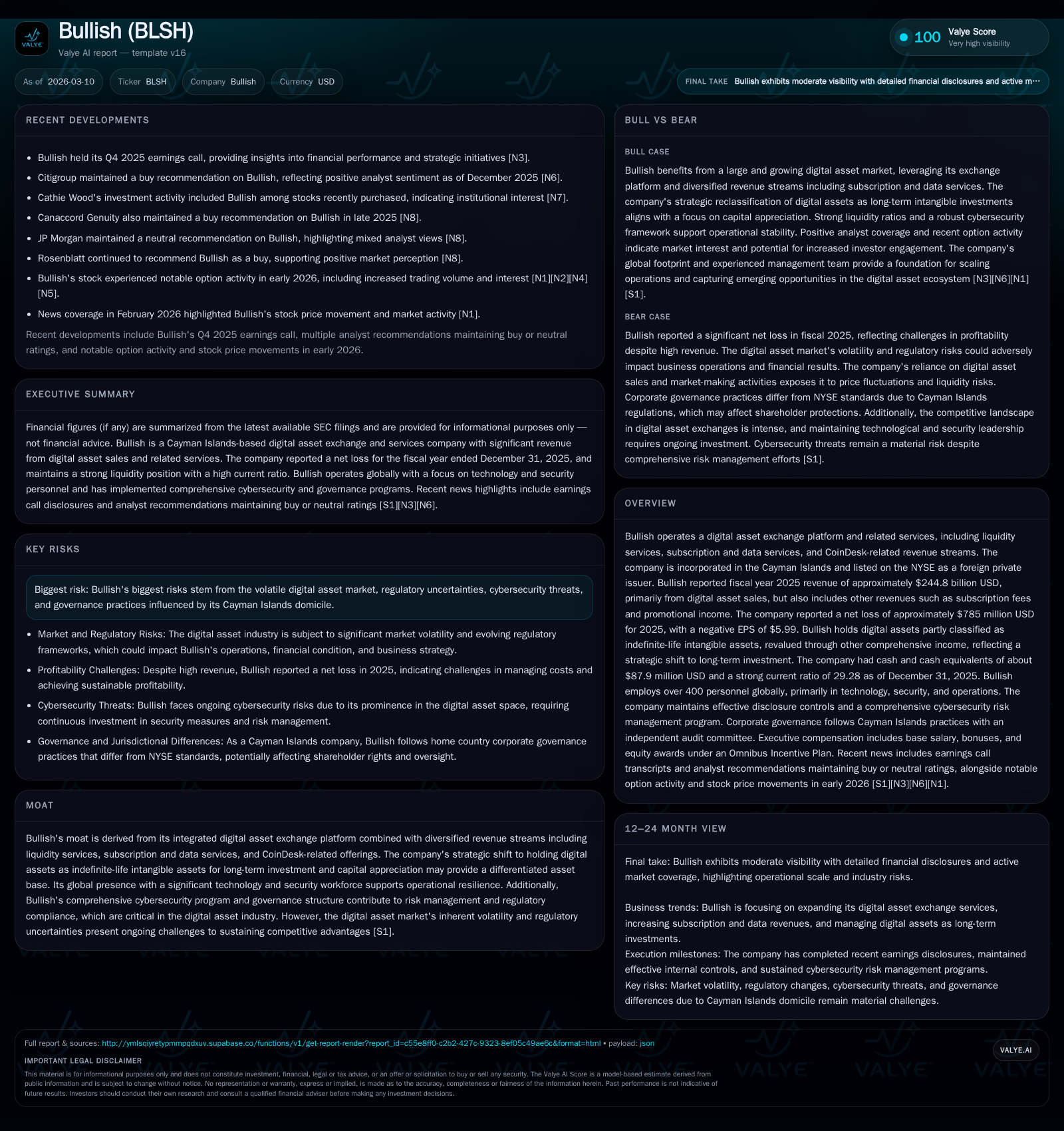

Bullish's Volatile Ride: From Massive Growth to Strategic Repositioning in Digital Assets

Bullish experienced exceptional revenue growth by nearly doubling digital asset sales from 2023 to 2025, yet faced a substantial net loss driven by strategic shifts and cost pressures.

Bullish delivered an extraordinary top line of $244.8 billion in fiscal 2025, reflecting robust transaction volumes amid digital asset market cycles. Despite this scale, the company recorded a sharp net loss of $785 million, stemming largely from its move to classify key digital assets as indefinite-life intangible assets and increased finance costs. Bullish’s liquidity profile remains strong with a current ratio above 29, supported by modest cash reserves relative to its ballooning revenues. However, rising administrative expenses and debt servicing costs indicate structural challenges. Its governance model centered in the Cayman Islands, combined with extensive cybersecurity efforts, reflects the complex regulatory environment it navigates. Near-term operational metrics and management commentary hint at cautious optimism but underscore persistent risks tied to sector volatility and evolving compliance demands.

Extraordinary Revenue Growth Amid Market Volatility

Bullish demonstrated remarkable revenue expansion from fiscal year 2023 through 2025. Starting with digital asset sales amounting to approximately $116.5 billion in 2023, the company achieved sales nearing $244.8 billion in 2025 [F1]. This near doubling traces closely with favorable digital asset market cycle dynamics and intensified transaction volume on Bullish’s proprietary exchange platform. The bulk of revenue arises from on-exchange digital asset sales that leverage Bullish’s Automated Market Making Inventory (AMMI) system designed to enhance liquidity provision efficiency.

Other revenue streams—including subscription fees associated with CoinDesk services, advertising, indices offerings, and promotional income—have grown modestly but contribute meaningfully to recurring cash flows [S1][F1]. However, cost of goods sold tracked proportionally alongside sales volumes, underscoring thin net spreads typical within high-frequency and high-volume digital asset exchanges [S17].

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Table: Fiscal Year Financial Summary for Bullish (figures rounded) [F1]

Financial Volatility and Shift to Long-Term Digital Asset Investment

A pivotal transformation influencing Bullish’s financial profile stems from its accounting policy revision effective January 1, 2024. The company reclassified certain digital assets not actively used for market-making purposes as indefinite-life intangible assets subject to revaluation through Other Comprehensive Income (OCI) per IAS 38 standards [S1][S4][S13].

This shift marks a clear strategic repositioning away from purely transactional trading profits toward long-term capital appreciation on select digital assets held within the balance sheet rather than trading inventories. By recognizing fair value gains or losses through OCI instead of earnings volatility, Bullish tempers income statement swings albeit at the cost of increased balance sheet complexity.

Consequently, the reported net loss of $785 million in fiscal year 2025 strongly reflects unrealized valuation declines amid sector price weakness rather than immediate cash impairments or operational failures [F1][S26]. This nuanced accounting approach fortifies investor understanding that earnings fluctuations are partly driven by macroeconomic digital asset price movements rather than purely operational results.

Additionally, a portion of these intangible digital assets supports liquidity provisioning strategies aimed at decentralized finance protocols generating yield returns recognized within OCI [S1]. This layered model aligns Bullish with emerging hybrid exchange-investment operators in the cryptocurrency ecosystem.

Operating Costs and Expense Dynamics Highlight Structural Challenges

Despite surging revenues, Bullish’s operating expense composition reveals mounting pressures that constrict net profitability outcomes.

Administrative expenses escalated from $104 million in 2023 to approximately $182 million in fiscal year 2025—a compound annual growth rate (CAGR) near +19%. This rise is attributable principally to increased headcount concentrated in technology development and cyber-security functions exceeding two hundred personnel worldwide [S1][S20]. Given industry imperatives around safeguarding client funds and compliance infrastructures, such cost intensification embodies necessary operational leverage rather than inefficiencies.

Finance expense surged markedly too—from below $3 million in 2023 up to roughly $52 million in the latest period—as borrowing facilities expanded substantially following related-party loans drawn down since late-2023 [S12][S16]. These debt increments underpin both working capital necessities and investments into intangible asset acquisitions.

Non-administrative other expenses also rose steeply reflecting impairments and derivative adjustments filling out comprehensive cost structures faced by high-growth fintech platforms navigating nascent markets.

These trends collectively underscore the dual challenge of managing narrow transaction margin economics coupled with heavy fixed overhead commitments vital for stability and growth within volatile crypto markets.

Liquidity Position and Capital Structure Analysis

Bullish displayed robust short-term liquidity metrics at December 31, 2025 with cash plus equivalents totaling approximately $87.9 million yet maintaining an outsized current ratio of nearly 29x given very modest current liabilities near $130 million relative to current assets over $3.8 billion [F1][S4][S11].

This anomaly primarily derives from classification effects including restricted cash components and sizeable digital asset holdings under intangible classifications constituting parts of current or near-current assets.

While the large current ratio signals ample buffer against liquidity shocks typical for exchanges holding customer deposits segregated from operational funds [S7], it also masks reliance on non-traditional cash equivalents such as stablecoins critical for instantaneous settlement demands.

The capital structure incorporates convertible preference shares alongside debt instruments largely sourced from affiliated parties [S6], exposing Bullish to refinancing risks but mitigating dilution via selective equity issuance strategies conducted during recent financing rounds.

Overall, liquidity provisions appear sufficient for near-term operating needs despite industry-wide concerns regarding credit access tightening amid heightened regulatory scrutiny.

Capital Allocation Focus: Modest Cash Reserves Amid Growth Investments

Bullish does not currently pay dividends nor has it engaged materially in share repurchases since listing—the company is prioritizing reinvestment into scalable infrastructure presumably involving technology stacks enhancements and security upgrades essential for sustaining competitive advantage [S9][S10].

Capital expenditures accelerated sharply to approximately $8 million in fiscal year 2025 from a mere $400 thousand just two years prior—reflecting intensified commitment to physical hardware acquisition alongside leasehold improvements supporting global office expansions across key fintech hubs [S4][S5].

Management disclosures reveal emphasis on measured capital deployment balancing innovation funding against cash conservation prudence given ongoing regulatory uncertainties enveloping digital asset operators.

Regulatory Backdrop and Governance in a High-Risk Industry

Operating as a Cayman Islands-incorporated entity exposes Bullish governance practices to home country corporate law which diverges somewhat from U.S. normative standards—particularly around shareholder meeting frequency, proxy solicitation requirements, and director nomination processes [S19].

However, the Board has established independent audit and compensation committees staffed with directors possessing financial expertise according to NYSE standards providing oversight aligned with investor protections expected within regulated exchanges [S18][S22].

Bullish's robust cybersecurity framework complements these governance structures mitigating material cyber risk which remains among the most significant threats faced by cryptocurrency exchanges worldwide [S1]. Regulatory ambiguity persists as an overarching headwind affecting licensing regimes, capital mandates, and operational compliance costs exacerbated by multinational footprints.

Short-Term Indicators and Monthly Metrics to Monitor

Recent monthly metrics releases for January and February 2026 depict fluctuating trading volumes that serve as leading indicators for quarterly performance assessments beyond full-year audited results [N1][N2][N3][N4]. Monitoring order book depth variations against prevailing digital asset price swings will yield insights into underlying client demand elasticity versus competitive positioning within fragmented exchange landscapes.

Subscription revenue growth velocity coupled with liquidity service fees may provide early signals regarding monetization effectiveness amid product mix shifts mentioned during recent earnings calls [N1]. Close observation of hedging derivatives fair value changes will also help contextualize P&L noise related partly to volatile underlying crypto prices.

Strategic Outlook: Opportunities and Constraints on Future Growth

Management commentary emphasizes a balanced view acknowledging macroeconomic uncertainty while highlighting strategic initiatives focused on broadening product lines beyond spot trading towards institutional custody solutions, data analytics services via CoinDesk integration, and enhanced DeFi protocols participation yielding diversified revenue streams [N1][S1].

Nonetheless, growth impediments persist rooted chiefly in evolving regulatory frameworks mandating expanded capital buffers alongside possible constraints on leverage usage inherent in credit risk mitigation strategies specifically relevant for crypto-centric lending exposures.

Achieving deeper market liquidity while controlling escalating finance costs remains an inflection point determining future margin restoration prospects amidst cyclical price volatility characteristic of cryptocurrencies globally.

This analysis is based solely on publicly available data including SEC filings [F1], official company reports [S#], and recent news sources [N#] as cited. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments