TWFG Inc.'s Agency Model Sparks Strong Growth but Faces Profitability Challenges

TWFG leverages a unique independent agency platform that drives premium volume growth yet contends with squeezed net income and measured capital returns.

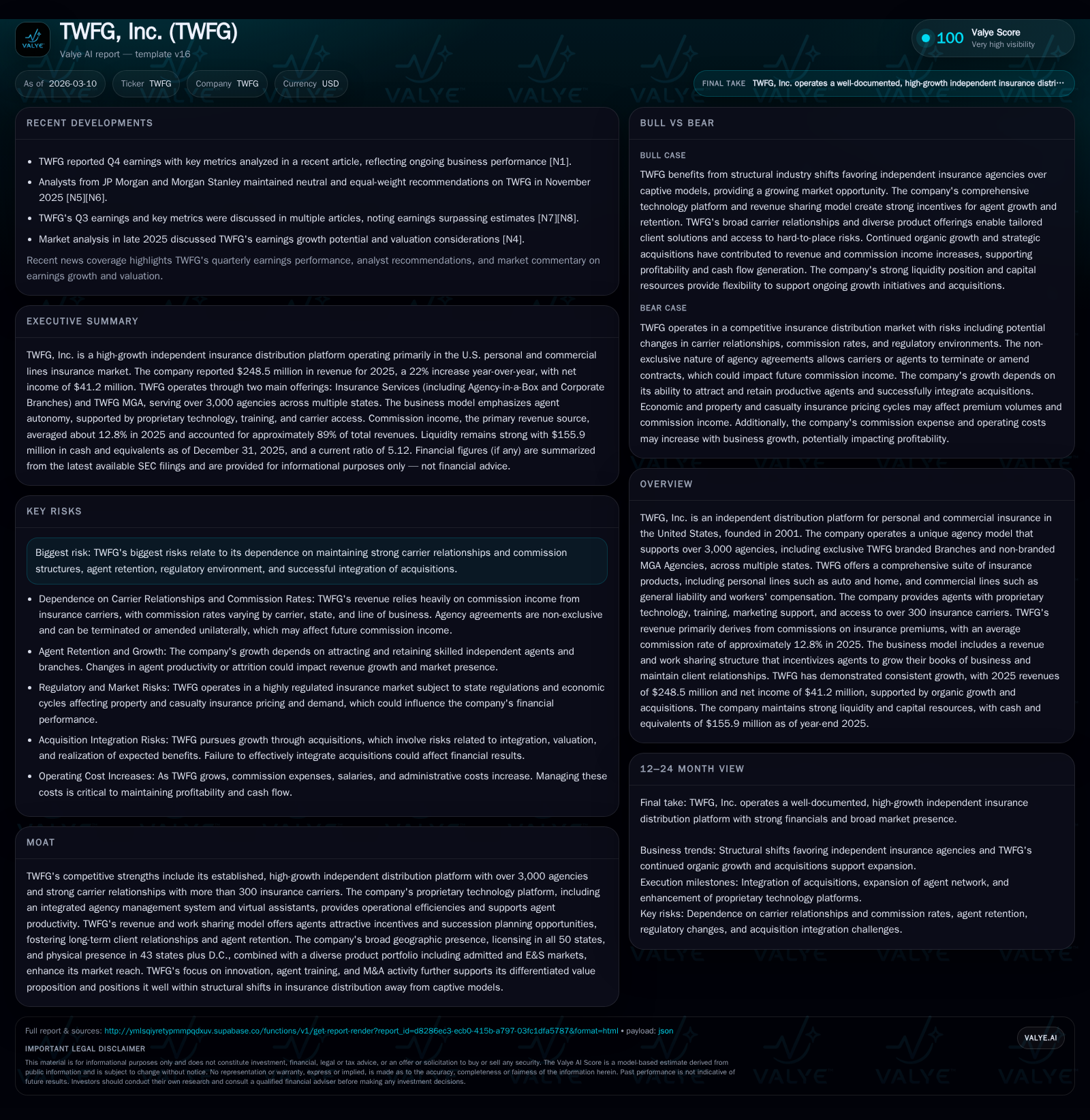

TWFG, Inc. has demonstrated robust growth through its innovative agency distribution model, expanding to over 3,000 agencies and exceeding $1.7 billion in Total Written Premium in 2025. This expansion fueled a 32.4% year-over-year increase in operating income, reflecting operational leverage despite economic headwinds. However, net income contracted by 66.3%, highlighting pressures from non-operating costs and commissions expense sharing. TWFG’s proprietary technology and agent incentive programs underpin its competitive moat, but future growth may be constrained by carrier relationship dependencies and regulatory factors. Cash flow generation remains healthy with strong free cash flow, though low return on equity signals capital allocation challenges amid selective reinvestment.

Track Record of High-Growth Independent Agency Expansion

TWFG has built its business over more than two decades into a premier independent distribution platform for personal and commercial insurance in the U.S., founded on a flexible agency model that consistently delivers high growth under varying market conditions [S1][S4][S29]. As of December 31, 2025, the company’s platform supported over 3,000 agencies—comprising approximately 550 exclusive TWFG branded Branches operating across 34 states plus D.C., alongside more than 2,750 non-branded MGA Agencies licensed in 43 states [S4][S16]. This hybrid agency structure facilitates broad geographic reach and product diversification.

Total Written Premium placed through TWFG exceeded $1.7 billion in calendar year 2025—a tangible testament to execution on scaling independent agents via multiple contract options including Branch contracts (exclusive branding) and MGA agreements offering extended carrier access [S4][S16]. The company's Agency-in-a-Box turnkey solution empowers new Branches with administrative support that accelerates growth without burdening agent autonomy [S21]. TWFG's thoughtful balance between owned Corporate Branches and independent Branch principals averaging nearly two decades of industry experience creates localized client engagement strengthened by community ties [S13].

This robust platform expansion correlates strongly with a notable operating income increase of 32.4% year-over-year to $36.99 million by FY2025 [F1], showing leveraged scalability even as the company invests selectively for sustainable agency recruitment and retention.

Commission Structures and Revenue Drivers: The Core of TWFG’s Model

Central to TWFG’s revenue generation is its commission-based business model deriving income chiefly from facilitating insurance contracts between clients and carriers [S2][S4]. The company negotiates agency agreements that establish commission rates typically spanning from 7% to as high as 30%, averaging about 12% company-wide for recent periods [S2][F1]. Commission income depends on premium volumes but also includes contingent commissions tied to underwriting results reported by insurers—introducing variability reflective of carrier performance cycles [S2]. Further revenue diversification arises from fee income streams encompassing policy fees, licensing charges and third-party administration fees contributed primarily through branch-related administrative activities [S2].

The non-exclusive nature of TWFG’s agency agreements permits either party unilateral termination or renegotiation, introducing renewal risk but simultaneously encouraging agents’ entrepreneurial efforts given the flexible contract design [S2][S29]. Profitability is thus sensitive to agent retention dynamics as well as sustained carrier approval.

Strategically grouping agents into TWFG Agencies (inclusive of exclusive Branches) versus MGA Agencies (non-branded independents with broad but less exclusive access) allows balanced premium write-ups across admitted and surplus lines markets—key given varying state regulations and insurance availability nuances [S16][S19]. This balanced portfolio supports stable premium volume growth despite pricing or underwriting turbulence.

Operating Profit Acceleration vs. Net Income Contraction: Delineating the Disparity

While operating income advanced sharply by 32.4% year-over-year to nearly $37 million at FY2025 compared to roughly $27.9 million in FY2024 [F1], net income trends diverged markedly—in fact contracting substantially by about two-thirds to just $2.75 million from $8.15 million recorded a year earlier [F1]. This notable net income compression amidst operating profit strength points toward elevated commission expenses paid out to agents under revenue sharing arrangements plus potential non-operating costs such as interest expense or tax impacts detailed minimally in filings.

The revenue-sharing model compensates Branch principals partly based on productivity incentivization schemes designed for growth, but it also raises commission expense line items proportionally limiting headline profitability margins [S19]. Additional factors potentially include amortization from M&A-related intangibles or discrete charges related to acquisitions which are not explicitly quantified in publicly available data sets here.

This disparity underscores the importance for stakeholders differentiating operating leverage—which reflects scalable core business momentum—from bottom-line earnings volatile enough to influence valuation conversations fundamentally around margin sustainability.

TWFG’s Technology and Agent Incentives as Growth Enablers

An integral element of TWFG's moat derives from its proprietary technology platform comprising an integrated agency management system that centralizes client data management, policy administration workflows, commission processing capabilities, plus advanced virtual assistant tools deployed via web and mobile applications [S4][S29]. These features materially reduce manual overhead at the agency level while enabling improved client servicing responsiveness.

Moreover, TWFG's work-sharing compensation models reward agents for growing their books of business alongside comprehensive training programs aimed at boosting agent productivity and retention [S29]. Agents benefit from both autonomy—uncharacteristic for captive channel peers—and operational support easing administrative burdens typical in small independent agencies.

Succession planning opportunities via M&A initiatives administered through the platform provide entrepreneurial agents clearer pathways for value realization at exit or transition stages—a critical factor underpinning long-term agent motivators within a highly fragmented P&C distribution environment [S4][S21].

Collectively these proprietary tools supplement carriers’ affinity for TWFG as an efficient distribution partner while structurally reinforcing barriers against potential shifts back toward captive models or direct-to-consumer alternatives.

Market and Regulatory Constraints Impacting Future Growth Trajectory

Despite positive trajectory drivers, TWFG faces external headwinds rooted primarily in macroeconomic fluctuations impacting P&C insurance demand—among them persistent inflation elevating claims severity; rising interest rates affecting financing dynamics; housing market slowdowns curbing personal lines policy creation; as well as geopolitical uncertainties contributing to client cautiousness [S1][S20].

Carrier underwriting volatility represents a systemic risk influencing contingent commission streams that historically have created episodic revenue swings for intermediaries reliant on these incentives [S20]. Additionally, the non-exclusive nature of agency contracts entails ongoing risk around carrier contract renewals or alterations driven by consolidation waves within the insurance carrier sector potentially narrowing distribution options.

On the regulatory front, expanding privacy laws exemplified by California’s evolving statutes impose new compliance costs alongside jurisdictional licensing requirements governing commission payments that could necessitate payment structure changes if regulators reinterpret licensing frameworks unfavorably toward intermediaries like TWFG [S20]. Moreover, product restrictions or compensation caps could dampen revenue potential in key states should legislation evolve adversely.

Competition within the independent agency space is intensifying with national agencies scaling via acquisitions plus fintech entrants harnessing alternate digital channels—TWFG must continue innovating its value proposition or risk margin compression extending beyond cyclical economic cycles.

Capital Allocation: Healthy Cash Flows Meet Low ROE and Selective Capex

The company's financial stewardship reveals robust free cash flow generation underpinned by strong operating cash flows that grew by roughly 32.2% year-over-year to $53.5 million during FY2025 compared with $40.48 million previously [F1]. Capital expenditures remain modest at approximately $0.36 million last fiscal year—a near nine-fold decline against prior period spend ($3.20 million)—reflecting selective reinvestment focused likely on maintenance capex rather than aggressive technology outlays or physical expansion [F1].

Balance sheet liquidity is solid evidenced by a current ratio exceeding five times as of year-end (current assets at $225 million versus current liabilities around $44 million), providing ample working capital flexibility devoid of material short-term debt pressures [F1][S7][S8]. The revolving credit facility capacity remains undrawn as per latest filings enabling potential acquisition funding if strategic opportunities arise without immediate liquidity strain [S8][S23].

Nevertheless, return on equity approximates a modest ~3.3% (net income relative to shareholder equity), indicating challenges translating substantial top-line growth into attractive shareholder returns at this stage—a function intertwined with net income margin compression alongside capital-heavy acquisition integration efforts possibly restraining near-term ROE expansion [F1].

No dividends or buybacks were referenced explicitly within recent reports suggesting capital recycling priorities skew toward organic growth facilitation plus bolt-on acquisitions rather than direct shareholder distributions currently.

Key Milestones Ahead and What Investors Should Monitor

While explicit forward guidance remains limited within disclosed materials [N1][S3], market participants should track several key indicators including:

- Continued expansion pace of both exclusive Branch networks and MGA Agencies across additional states,

- Stability or improvement in average commission rates amid shifting carrier negotiation landscapes,

- Successful technology platform enhancements improving agent retention metrics,

- Integration outcomes from recent acquisitions such as controlling interests in Florida MGA entities,

- Trends in contingent commission receipts reflective of underlying underwriting performance trajectories,

- Regulatory developments impacting commission structures or licensing compliance frameworks. These milestones will collectively signal whether TWFG can sustain its strong premium written momentum while addressing profitability constraints inherent within its revenue-sharing model.

Risks from Carrier Dependence and Competitive Pressures

TWFG's dependence on maintaining solid relationships with over 300 insurance carriers anchors much of its operational viability; disruptions here could materially impair premium placements or alter commission parameters unfavorably [S20]. Contingent commissions’ variability exposes earnings unpredictability tied directly to external carrier underwriting successes or losses undermining recurring revenue assumptions.

Agent retention poses another risk vector since high agent turnover could erode customer relationships foundational to renewal rates; competition from other large aggregators aggressively acquiring small agencies raises these stakes further.

Regulatory risks include increased compliance burdens associated with evolving privacy laws such as CCPA/CPRA expansions along with heightened scrutiny concerning unlicensed payments potentially triggering retroactive adjustments necessitating structural compensation redesigns detrimental to margins [S20].

Litigation risks remain moderate currently but any adverse rulings could lead to reputational harm limiting agent recruitment or consumer trust.

Overall competitive pressures require continuous innovation investment lest TWFG cede ground to digitally native peers leveraging AI-enabled quoting engines or fully integrated omnichannel platforms presenting alternatives more attractive to modern buyers.

Annual Historical Performance Summary Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 3 | 54 | 37 | 0 | -66.3% |

| 2024 | 8 | 40 | 28 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 53 | 3.3 |

| 2024 | 37 | 11.0 |

Source: SEC companyfacts cache [F1]. Total Written Premium data for 2025 is sourced directly from SEC narrative disclosures; prior years' premiums are not explicitly quantified[S4]. Operating income (OpInc), net income (NetInc), operating cash flow (CFO), capex figures are extracted from F1.

This analysis has been prepared solely for informational purposes based on publicly reported SEC filings dated as of March 10, 2026 ([F1],[S#]) and corroborating news reports ([N#]), integrating domain expertise without offering investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments