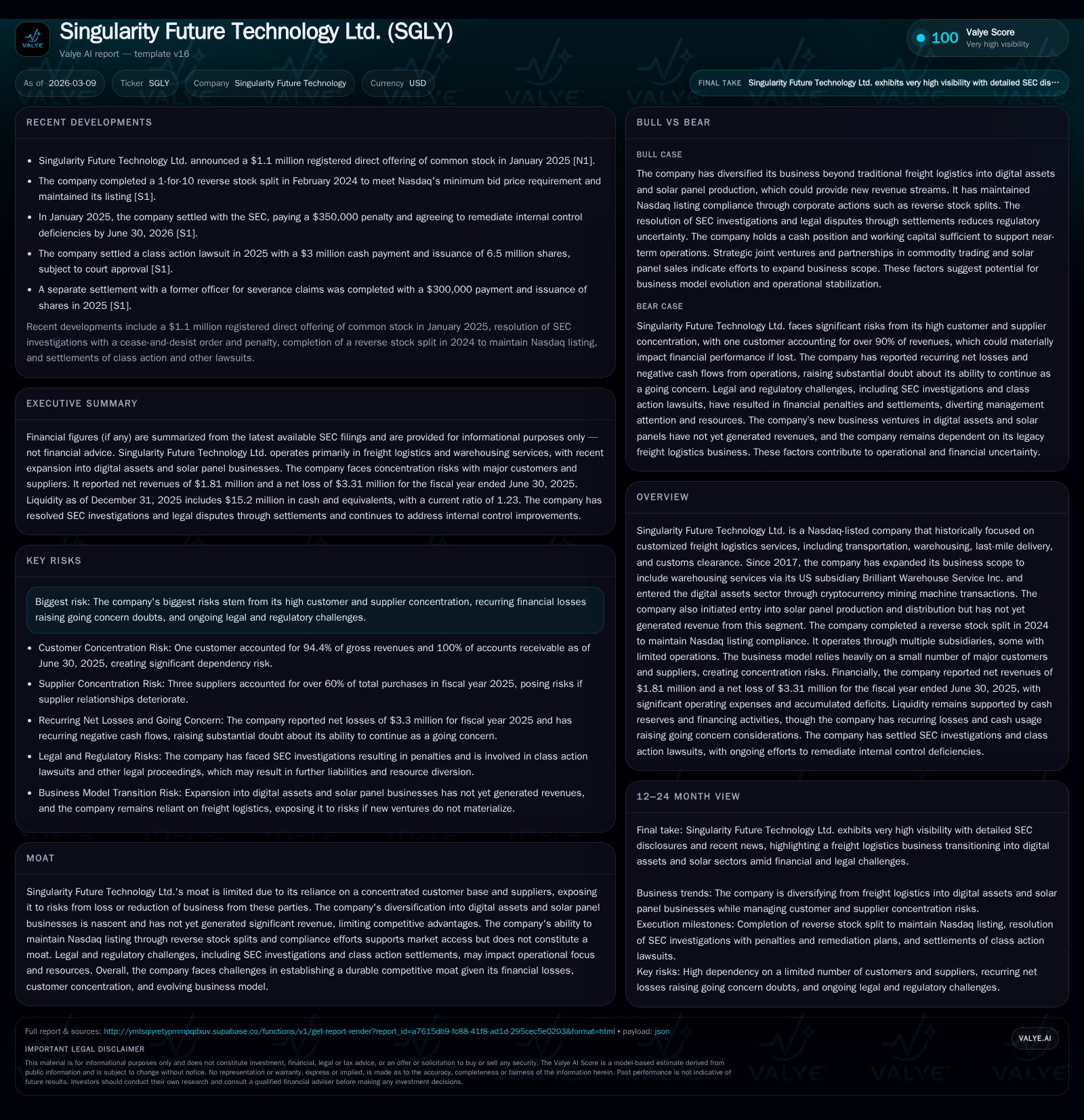

Singularity Future Technology's Shifting Revenue Base and Regulatory Pressures

Singularity’s transition from freight logistics to digital assets and solar panel ventures marks a turbulent revenue decline compounded by concentrated customer risks and ongoing legal challenges.

Singularity Future Technology Ltd., originally centered on freight logistics, has witnessed a sharp contraction in revenue, from $5.15 million in FY2021 to roughly $1.8 million in FY2025, driven primarily by reduced freight operations and tariff-induced volume declines. The company's strategic diversification into cryptocurrency mining equipment trading and solar panel production remains nascent with no reported revenues, exposing it to uncertain growth prospects. High customer and supplier concentration, liquidity challenges underscored by a reverse stock split for Nasdaq compliance, alongside substantial legal exposures including securities class action settlements, weigh heavily on its operational stability and financial outlook.

Revenue Trajectory and Core Business Dynamics Since 2021

Singularity Future Technology Ltd.'s financial history reveals a pronounced decline in top-line performance over the past several fiscal years. Revenue peaked at approximately $5.15 million in FY2021, anchored primarily by its customized freight logistics operations comprising transportation, warehousing, last-mile delivery, and customs clearance services across various geographies [F1]. However, this figure slumped precipitously to about $1.81 million by FY2025 — a decline exceeding 60% CAGR when viewed over four years [F1].

This contraction reflects sector pressures manifesting as gross margin erosion and dwindling operating leverage benefits within freight logistics segments. Notably, the company's U.S.-based subsidiary Brilliant Warehouse Service Inc. shuttered operations in fiscal 2024 reducing both shipping revenues and associated costs materially [S27]. Concurrently, tariff disputes adversely impacted volumes from Chinese subsidiaries contributing to an overall shrinkage in revenue generation capacity [S27]. Despite cost reductions leading to a narrower operating loss, the company recorded an operating deficit of roughly $2.7 million for FY2025, compared with deeper losses exceeding $22 million as recently as FY2022 [F1].

The gross margin compression—dropping from a positive albeit slim margin to a negative corridor during peak loss periods—highlights systemic challenges faced in maintaining profitable freight forwarding amid intensifying competition and geopolitical trade disruptions [S27]. This backdrop frames the company’s evolving core business dynamics wherein scale erosion confronts fixed cost burdens inherent to freight service models.

The Diversification Bet: Digital Assets and Solar Panel Production

Since pivoting efforts commenced around 2017 under its renamed corporate identity (effective January 2022), Singularity expanded into nascent technology-adjacent fields such as digital assets via cryptocurrency mining machine transactions through U.S. subsidiaries and initiated a solar panel production/distribution segment [S1][S6]. However, these ventures remain embryonic; the company admitted zero revenue realization from solar panel activities as of the latest filings [S6], emphasizing these as strategic experiments rather than established profit centers.

The crypto mining machine commerce leverages technical equipment trade but faces significant headwinds ranging from volatile digital asset markets to regulatory scrutiny affecting profitability visibility. These sectors inherently require considerable capital outlays and swift innovation cycles, neither of which has translated into concrete earnings for Singularity thus far [F1][S6].

This diversification potentially offers long-term runway if execution risks are mitigated; however, lack of explicit revenue milestones or guided forecasts leaves current impact marginal while compounding uncertainty surrounding capital efficiency . The continuation into solar products through joint ventures with market participants signals intent yet remains premature for valuation or operational integration assessment [S16].

Customer and Supplier Concentration Risks Burdening Growth Prospects

A defining characteristic of Singularity’s operational risk profile is its extreme exposure to a narrow client base coupled with few key suppliers capable of exercising undue influence [S3][S5][S8][S19]. For FY2025, one customer accounted for approximately 94.4% of gross revenues while this same entity represented virtually all accounts receivable balances [S13], illustrating acute counterparty dependency vulnerabilities.

Such concentration fosters potential revenue volatility should contract renegotiation fail or client attrition occur—a scenario that could severely curtail cash flow generation critical to funding operations absent fresh capital inflows. Similarly, vendor dependence is substantial; three suppliers composed more than 34%, 16%, and 10% of procurement spend respectively last year raising concerns about supply chain resilience [S19].

These dependencies underscore substantial counterparty risk where unfavorable shifts could cascade through working capital cycles. Management acknowledges that efforts to broaden relationships with additional solar partners and other third parties aim at mitigating these exposures but admit these initiatives are progressing slower than desired thus far [S19]. Liquidity planning must incorporate worst-case scenarios given this backdrop.

Liquidity Position and Capital Structure Under Regulatory Scrutiny

Singularity’s liquidity position evidences both operational strain and attempts at shoring balance sheet integrity amidst external pressures. As of FY2025 end-date (June 30), current assets stood near $21.56 million against liabilities around $17.56 million reflecting a current ratio near 1.23—a modest buffer against short-term obligations but down from prior year ratios signaling tighter coverage [F1][S26]. Cash holdings were solidly maintained above $15 million at calendar end December 2024 though operating cash flow remained negative ($2.69 million CFO for FY2025) indicating persistent funding reliance on financing sources [F1][S9][S10].

Equity declined markedly from over $54 million at FY2021 due to cumulative losses falling below $12.5 million at mid-FY2025 indicating significant net asset erosion impacting corporate leverage metrics [F1]. Capital structure transformations included a crucial reverse stock split undertaken on February 9, 2024—a one-for-ten consolidation enacted explicitly to meet Nasdaq minimum bid price requirements ensuring continued listing eligibility [S6]. This measure underscores elevated listing compliance risk alongside investor confidence challenges.

Within debt management parameters detailed in filings, no major maturity hazards emerged imminently but growth constraints remain given limited credit access relative to working capital draws [S4][S7][S9]. Overall, tightened liquidity underscores prioritization towards operational sustainability amidst regulatory oversight.

Legal Proceedings and Their Financial Implications

Ongoing legal challenges constitute material headwinds shaping Singularity’s resource deployment landscape. The company faces securities litigation stemming primarily from alleged false or misleading disclosures related to fraudulent transactions involving former executives as detailed in class action suits initiated since late 2022 [S11][S14][S22][S24]. Notably, a settlement finalized July 13, 2025 requires payment comprising $3 million cash plus issuance of 6.5 million shares pending court approval—significant charges detracting from financial flexibility while imposing reputational damage risks [S24].

Other lawsuits include derivative claims by ex-board members settled confidentially after payment of legal fees amounting to $150,000 illustrating recurring governance-related disputes [S16]. These proceedings absorb management focus via high external counsel expenses alongside administrative costs such as arbitration fees which cumulatively burden results absent direct income offsetting.

Regulatory investigations alleging law violations entail potential fines or consent decrees threatening business continuity adjustments though outcomes remain uncertain requiring continued reserve estimation diligence per management disclosures [S11][S25]. The enduring nature of these legal matters implicates sustained vigilance over contingent liabilities.

Capital Allocation Approach: Absence of Dividends and Minimal Capex

Singularity maintains a conservative capital stewardship posture evidenced by absence of dividend payments historically or projected given retained earnings priorities geared toward operational needs rather than shareholder returns [S6][S12][S17][F1]. Investment activity sharply contracted with capital expenditures plunging nearly 98% year-over-year concluding below $600 in FY2025—symbolizing scaled-back physical asset deployment reflecting retrenchment from earlier growth strategies reliant on warehouse or technology infrastructure expansion [F1].

This capex retrenchment contrasts starkly against prior multi-hundred-thousand dollar investment phases suggesting strategic recalibration emphasizing liquidity preservation over expansion tappable only with improved top-line traction or funding availability.

Key Metrics Snapshot: Revenue, Losses, Cash Flow, and Equity Trends

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -4 | -3 | -3 | ||

| 2023 | 5 | -23 | -34 | -15 | +13.8% | +20.5% |

| 2022 | 4 | -29 | 6 | -23 | -22.6% | -327.1% |

| 2021 | 5 | -7 | -4 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -31.4 |

| 2023 | -34 | -205.7 |

| 2022 | 5 | -80.5 |

| 2021 | -6 | -12.5 |

Source: SEC companyfacts cache [F1].

The table illustrates decisive revenue retrenchment coincident with reducing operating losses albeit still deeply negative net income persistency leading to marked ROE deterioration nearing -31.4% for latest annual metrics highlighting diminished shareholder value creation ability despite some loss improvements [F1].

Operating cash flow remains negative reflecting ongoing burn making external liquidity essential while capex minimization embodies survival mode investment behavior consistent with tightened financial constraints.

Outlook Signals: Market Access, Nasdaq Listing Compliance, and What to Monitor

Looking forward without explicit formal guidance available publicly for fiscal periods beyond mid-2025 requires observer vigilance focusing on several vectors: successful maintenance of Nasdaq listing post-reverse split remains paramount for public market access underpinning secondary financing avenues; evolution in customer base composition will be critical given outsized revenue concentration posed threats; progress or setbacks within digital assets and solar segments offer potential upside variability but with high execution risk; further regulatory developments or litigation resolutions may materially affect resource allocation frameworks; lastly liquidity trends warrant continuous tracking balancing operational cash flows versus accrued liabilities earmarked for settlements or capital commitments [S6][S18].

Given the confluence of pressures from legacy business contraction juxtaposed against unproven new lines amid significant legal entanglements renders Singularity’s near-to-medium term stability fragile warranting cautious monitoring.

This analysis is based exclusively on disclosed public filings and verified data points without speculative projections or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments