Kaltura Expands AI-Driven Video Platform Amid Modest Revenue Growth and Sharpened Focus on Enterprise Adoption

Kaltura’s API-first Digital Experience Platform blends video, AI, and conversational tools targeting enterprises while navigating margin and liquidity pressures.

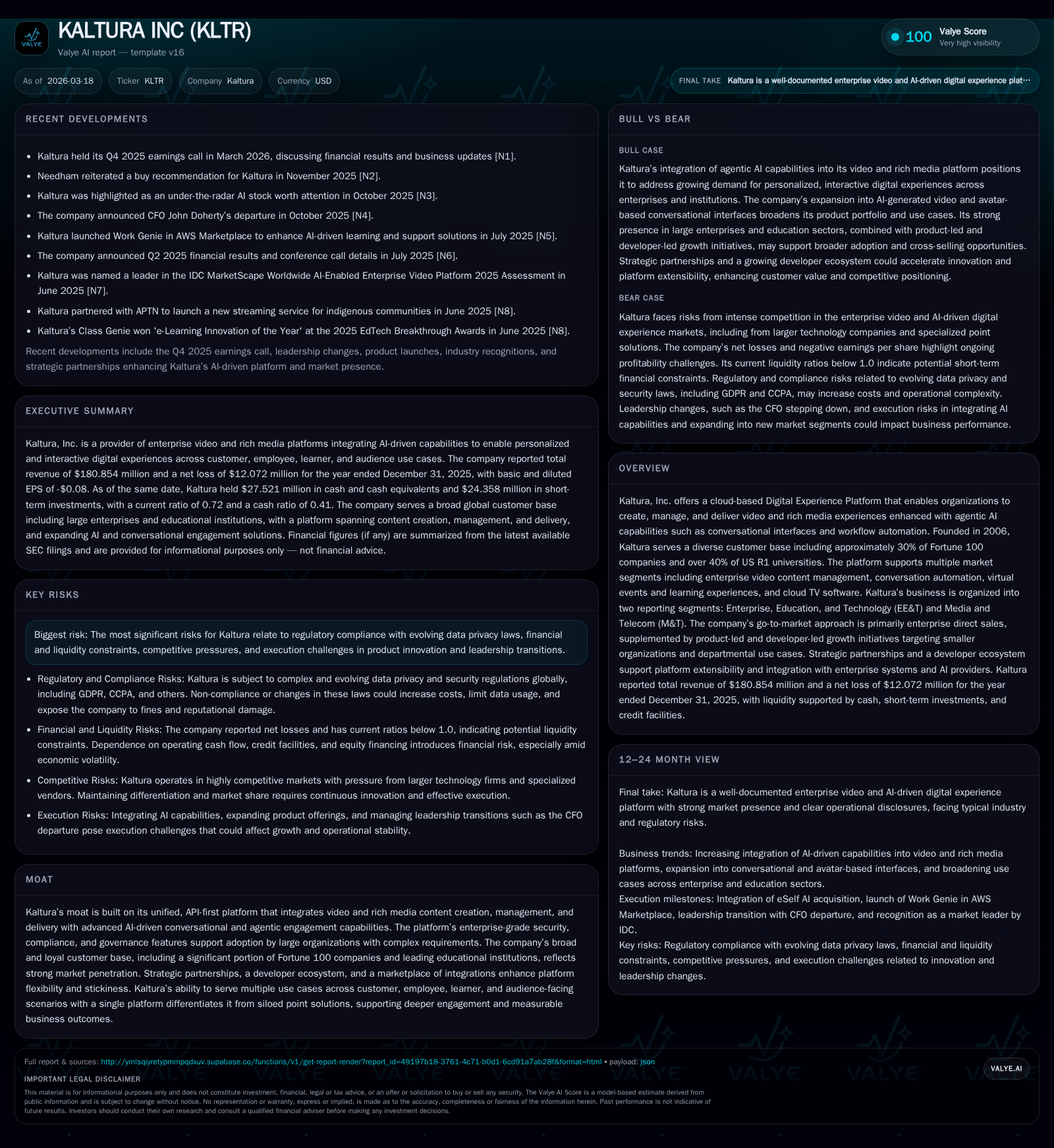

Kaltura, Inc. reported $180.9 million in revenue for fiscal 2025, reflecting a modest 1% growth over 2024, driven primarily by broad enterprise adoption and expansion in education and technology segments. The company maintains a unified platform integrating video content management with agentic AI features such as conversational interfaces to support diverse use cases across industries. Despite ongoing operating losses and negative net income, cash flow from operations remains positive, supporting ongoing investments and share repurchases aimed at strategic capital allocation. Kaltura faces key challenges including evolving regulatory compliance, competitive pressures, and the need to diversify growth beyond its core large enterprise base using product-led and developer-led initiatives.

Company Overview

Kaltura, Inc., founded in 2006, operates a cloud-native Digital Experience Platform that centrally features video and rich media content creation, management, and delivery enabled with advanced agentic artificial intelligence (AI) capabilities such as conversational interfaces and workflow automation [S1][S4]. The platform supports diverse organizational journeys including customer engagement, employee communication, learning environments, virtual events, and cloud TV services spanning multiple industries.

The company segments its business into two main reporting units: Enterprise, Education & Technology (EE&T), which accounted for approximately $134.4 million in revenue in FY2025; and Media & Telecom (M&T), generating around $46.4 million [S16]. Kaltura's core competitive advantage lies in its unified API-first architecture enabling modular integrations across workflows coupled with enterprise-grade security and compliance features attractive to complex organizations [S21].

Historical Financial Performance

Kaltura's revenue was $180.9 million for FY2025, marking a slight 1% increase compared to $178.7 million in FY2024 [F1]. This modest topline growth is consistent with a period of increased macroeconomic volatility leading to longer sales cycles and more price-driven competition as noted by management [S1].

The company has improved profitability metrics year-over-year with operating losses narrowing significantly from -$24.1 million in FY2024 to about -$5.0 million in FY2025 and net losses improving from -$31.3 million to -$12.1 million [F1]. These results indicate progress in containing costs despite investments in new product development.[F1]

Operating cash flows turned positive at $14.5 million in FY2025 compared with $12.2 million the prior year reflecting better operational efficiency, while capital expenditures remained modest at approximately $0.66 million [F1]. Free cash flow was estimated around $13.9 million demonstrating ongoing cash generation capacity supportive of reinvestment strategies [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -12 | 15 | -5 | 1 | +61.4% |

| 2024 | -31 | 12 | -24 | 1 | |

| 2022 | -46 | -8 | -39 | 3 | +21.9% |

| 2021 | -59 | -22 | -33 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 26 | 14 | -190.7 |

| 2024 | 3 | 12 | -128.4 |

| 2022 | -11 | -152.9 | |

| 2021 | -24 | -69.6 |

Source: SEC companyfacts cache [F1].

Note: Operating income YoY improved by ~79%, Net income loss severity reduced by ~61%, Operating cash flow increased by ~19%.

Revenue Drivers & Segment Dynamics

Enterprise customers remain the backbone of Kaltura’s recurring revenue streams representing the substantial majority of subscription income [S4]. These clients typically deploy across multiple use cases—such as internal communications, learning platforms or marketing—and span several organizational functions requiring complex integration, scalability, compliance, governance [S7][S13]. Approximately 30% of Fortune 100 companies and over 40% of US R1 universities use Kaltura's solutions illustrating penetration into market-leading accounts [N1].

The EE&T segment showed healthy growth increasing revenues from $128.7 million in FY2024 to $134.4 million in FY2025 [S16]. Conversely, revenues from Media & Telecom declined slightly (from about $50 million down to $46.4 million), affected by longer implementation cycles typical for TV offerings that involve higher upfront professional service efforts impacting gross margins negatively relative to EE&T products [S16][S9].

The licensed offerings' diversity—ranging from cloud-based SaaS products for digital experiences to private cloud or on-premise deployments—adds complexity but also flexibility for different vertical markets.

Future Growth Prospects

Looking ahead, Kaltura aims to leverage its expanding portfolio of AI-assisted content creation tools and conversational rich media agents that enable targeted departmental adoption alongside its large enterprise deals [S19]. Embracing product-led growth (PLG) models complemented by developer-led growth (DLG) through SDKs such as Agentic Avatar SDKs is central to broadening reach especially within smaller organizations or specialized teams inside larger enterprises [S7][S20].

The company's go-to-market strategy still centers on direct enterprise sales but increasingly incorporates self-service adoption paths and channel partnerships including VARs, OEMs, system integrators, and cloud marketplace operators—to accelerate customer acquisition cost efficiencies while expanding addressable markets globally [S20].

However, management signals caution regarding macroeconomic headwinds affecting customer budgets which could constrain demand or renewal rates near term [S1]. The ability to continually enhance AI capabilities amidst evolving regulations will also be critical.

Operational Expectations & Milestones

Explicit financial guidance for subsequent periods has not been provided; however management commentary highlights intentions to:

- Continue expanding AI-driven functionalities integrated within its digital experience platform.

- Accelerate cross-sell opportunities within existing enterprise accounts leveraging broad platform scope.

- Scale product-led initiatives designed for faster onboarding via modular offerings reducing deployment friction.

- Maintain disciplined cost control balancing R&D investment against improving operating leverage. Ongoing monitoring should focus on net dollar retention trends beyond the recent stable mark of roughly 100%, further margin improvement trajectories particularly for M&T segment through operational efficiencies, plus any material changes in capital structure or liquidity positions announced via quarterly updates or credit agreement amendments [N1][S8][S18].

Returns & Capital Allocation

Kaltura has yet to achieve profitability with a negative approximate return on equity of -191%, derived from FY2025 net losses against shareholders’ equity of roughly $6.33 million at year-end [F1]. However positive operational cash flow indicates underlying business health improving operational operations.

Capital allocation reflects an aggressive share repurchase program totaling approximately $26.2 million executed during FY2025—a marked increase over prior years intended to optimize capital structure under amended credit facility covenants allowing defined levels of restricted payments including buybacks [F1][S10][S23][S25]. No dividends have been declared nor are expected given reinvestment priorities.

Industry Positioning & Competition

Kaltura faces competition from vendors targeting isolated video content delivery or conferencing solutions but differentiates itself via an integrated platform approach combining creation, management and experiential layers along with advanced AI-enabled conversational interfaces enhancing engagement metrics [S21]. Its focus on highly regulated global enterprises with demanding security requirements further distinguishes it from smaller SaaS niche players.

Competitors often possess larger scale or singular product focus; however Kaltura’s modular APIs/SDKs support embedding into partner ecosystems amplifying distribution reach while sustaining stickiness through extensibility features like marketplace plugins developed collectively with ISVs and partners [S20]. The converging trend towards personalized agentic digital experiences strengthens demand for platforms like Kaltura’s that blend multi-media richness with AI orchestration.

Risks & Challenges

Primary risks highlighted revolve around compliance uncertainty amid fast-evolving data privacy laws globally plus nascent AI regulation regimes—where novel legal liabilities or restrictive operational limits could emerge impacting product development cycles or functionality deployment prohibiting certain features usage in jurisdiction-sensitive contexts [S24]. Financially manageable debt levels exist but continued access to capital markets may be challenged by geopolitical factors including regional conflicts affecting operations especially given company presence in Israel [S25]. Competitive intensity is expected to persist requiring sustained innovation investment.

Operational execution risks include scaling new sales motions effectively without cannibalizing traditional large-account pursuits; managing longer sales cycle durations notably within media telecom deployments; maintaining high renewal rates under budget-constrained clients; retaining skilled technical personnel amidst sector-wide talent competition.

Conclusion

Kaltura stands at an inflection point where incremental revenue growth belies substantial underlying shifts towards richer AI-integrated video experiences that span broad enterprise workflows beyond conventional streaming use cases. Its strategic emphasis on unifying content creation/management/delivery via an API-centric platform supplemented with conversational agent technologies underscores its vision of enabling outcome-oriented digital journeys at scale. Liquidity conditions appear solid providing fuel for acquisitions or organic investment amid measured share repurchase activity supporting capital returns even as operating profitability remains elusive. Watch points include evolving regulatory adherence around data privacy/AI ethics frameworks which have direct implications on product feature sets; traction gains within newer PLG/DLG initiatives that seek volume-driven adoption lifts; plus gross margin improvements particularly within Media & Telecom vertical where professional services complexity currently weighs results. Overall, Kaltura’s foundation leverages decades-long domain experience serving some of the most demanding global enterprises—positioning it well if execution risks are mitigated successfully amidst fast-moving technological adoption waves in digital media engagement.

This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding Kaltura Inc.’s securities nor any other financial instruments or strategies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments