Knowles Corporation's Q1 Spurs Momentum in High-Performance Component Markets

Knowles’ latest quarterly results reflect strong organic growth driven by its custom Precision Devices and MedTech & Specialty Audio segments amidst rising defense and hearing health demand.

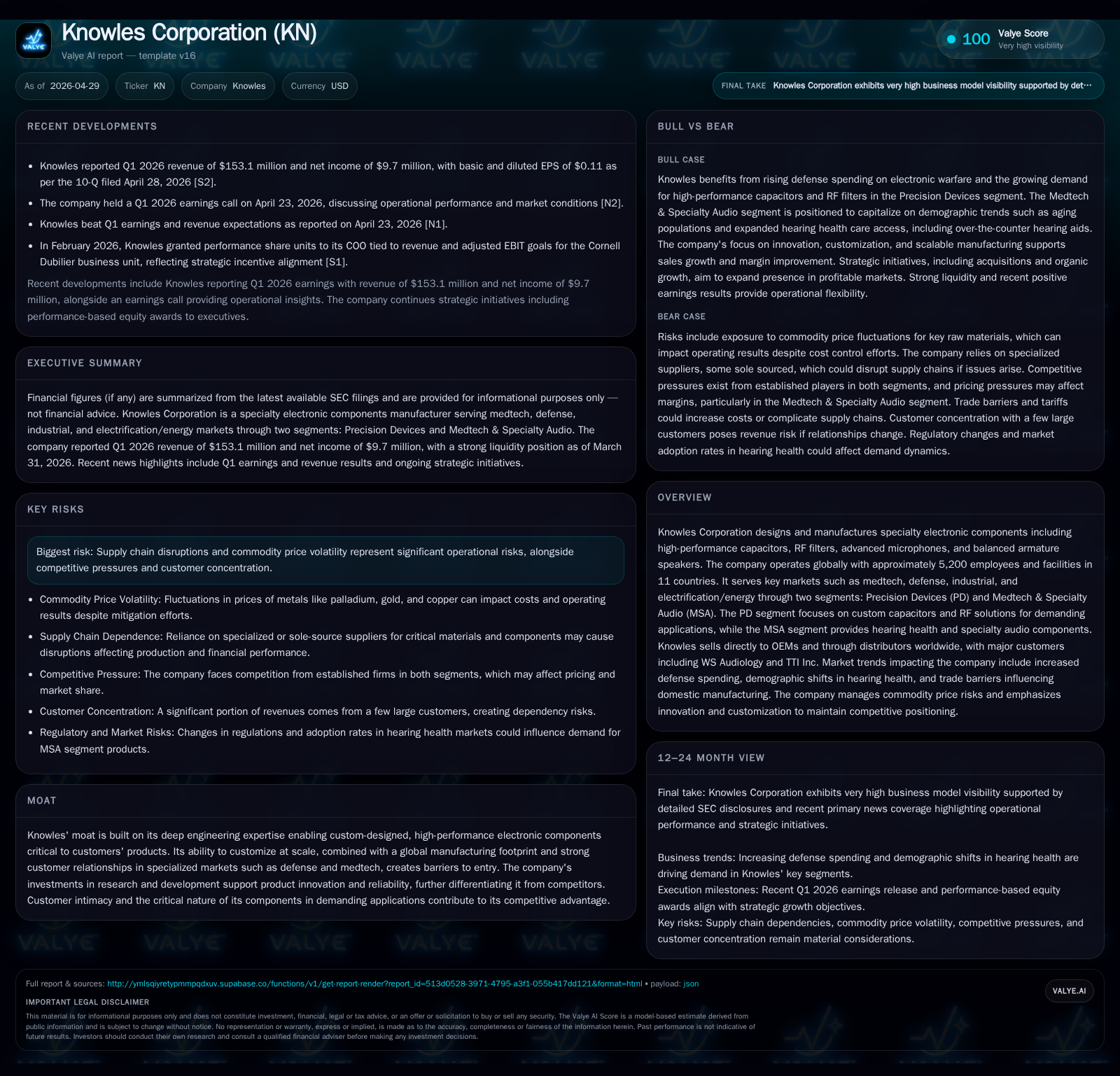

Knowles Corporation reported a robust start to 2026 with solid revenue growth and margin improvements across its key segments, reinforcing the strength of its specialized electronic components portfolio. The company’s focus on customized, high-performance capacitors, RF filters, microphones, and balanced armature speakers continues to position it well in growing defense electronics and expanding hearing health markets. Persistent supply chain risks and customer concentration remain watchpoints, but ongoing innovation and favorable market trends support a positive medium-term outlook.

Q1 2026 Operating Results and Implications

Knowles Corporation's first quarter ending March 31, 2026 demonstrated meaningful operational momentum confirmed by its April 28th 10-Q filing and recent earnings release on April 23rd [S2][S3][N1]. The firm reported organic growth driven by both primary business segments: Precision Devices (PD) and MedTech & Specialty Audio (MSA).

Supporting this was management commentary emphasizing continued strength in defense-related RF filters and capacitors fueled by increased global defense budgets and supply chain localization trends. Similarly, the MSA segment leveraged expanding hearing aid adoption globally, aided by favorable U.S. regulatory changes allowing over-the-counter access which opens new patient demographics [N2].

This quarterly uplift is particularly significant given prevailing macro uncertainties. Execution confirms Knowles' ability to capture structural demand drivers while navigating logistical challenges. Sustained margins improvements were aided by operational efficiencies despite commodity cost fluctuations.

Business Model: Custom Engineered Components for Demanding End Markets

Knowles operates through two distinct segments aligned with specialized customer needs [S1]:

Precision Devices (PD): Focused on high-performance capacitors and radio frequency filters tailored for defense, industrial applications, medtech instruments, and electrification/energy sectors. Products often require customization for elevated voltage tolerance, temperature resistance, or ultrahigh reliability. This necessitates close technical integration with OEMs and drives high switching costs.

MedTech & Specialty Audio (MSA): Provides advanced balanced armature speakers and microphones primarily serving hearing health manufacturers (such as WS Audiology) alongside specialty audio devices. The segment prioritizes miniaturization, broad frequency response, low power consumption, and acoustic module customization.

Revenue flows predominantly from OEM direct sales supported by a global distribution network including specialized sales reps and distributors. Knowles’ value proposition hinges on engineering-driven customization at scale coupled with rigorous quality standards enabling mission-critical applications.

Industry Position: Competitive Advantages and Customer Dynamics

Knowles’ moat centers on engineering depth that enables unique component designs difficult for competitors to replicate at scale without sacrificing reliability [S1]. The company buttresses this through a geographically diverse manufacturing footprint spanning North America, Europe, and Asia—which is particularly strategic in servicing the defense sector's increasing preference for domestic sourcing due to geopolitical considerations [S17].

Key customers like WS Audiology represent significant revenue portions (~11% in 2025) while TTI Inc serves as principal distributor making up about 10%. This concentration underscores dependency risk but also affirms strong customer trust in Knowles’ technology solutions [S11].

Competitively, PD faces fragmented rivals across specialty capacitor suppliers but maintains pricing leverage in defense due to product complexity. In MSA, Knowles leads in innovation particularly against competitors focused solely on commodity audio components by investing heavily in R&D for superior acoustic performance [S15].

Supply chain remains a consideration given sole-source relationships for certain inputs; however, no current disruption materially impacted profitability per latest disclosures.

Growth Drivers: Defense Spending, Hearing Health Trends, and Innovation

Three clear structural drivers underpin Knowles’ growth:

Defense Electronics Expansion: Rising global geopolitical tensions have expanded defense budgets focusing on electronic warfare technologies reliant on precision RF filtering solutions. Domestic manufacturing requirements further favor vendors like Knowles who provide secure supply chains within allied borders [S1].

Hearing Health Demographics: Global aging trends increase hearing loss prevalence while newly expanded regulatory regimes (e.g., U.S. over-the-counter hearing aids) reduce barriers for adoption. These factors create volume tailwinds for MSA components designed into hearing aids [S17][N2].

Product Pipeline Innovation: Continuous R&D investment enables Knowles to refresh product portfolios with newer capacitors meeting higher voltage or temperature specs as well as smaller form-factor microphones featuring broader frequency response. This innovation mitigates price erosion through differentiation [S15][N2].

Management signals ongoing margin improvement programs tied to productivity gains which should sustain profitability as volumes grow.

Risks and Constraints: Supply Chain, Customer Concentration, and Pricing

While operating prospects appear sound, Knowles faces persistent risks:

Raw Material Volatility: Metals like palladium and gold used in capacitors are subject to price swings impacting input costs. Fixed-price supplier contracts only partially hedge these exposures [S11][S18].

Supplier Dependencies: Some critical materials or subassemblies rely on sole-source suppliers potentially vulnerable to disruptions or capacity constraints.

Customer Concentration: Reliance on a limited number of large customers (~21% combined revenue from top two) concentrates payment risk though contractual relationships mitigate immediate impact [S11].

Competitive Pressures: Especially in the MSA segment where commoditization threatens pricing. Knowles addresses this through cost reductions but must continuously innovate.

Geopolitical Trade Barriers: These complicate global supply chains but also offer opportunities for localized manufacturing investments amid shifting trade policies [S17].

Latest filings confirm no material changes in risk profile since prior annual reports [S8].

Looking Ahead: Guidance and Key Execution Milestones

The company’s recent disclosures do not provide explicit updated numeric guidance but emphasize priorities such as maintaining double-digit growth trajectories in target markets via enhanced domestic manufacturing capabilities for PD products [S3][N2].

Investors should monitor:

- Q2 bookings trends as early indicators of sustained commercial traction,

- Progress against margin improvement initiatives,

- Deployment of new product lines approved for high-security defense applications,

- Outcomes of ongoing efforts to broaden customer base beyond current concentration.

Investor materials suggest upcoming presentations may shed light on near-term capital allocation strategies including potential acquisitions supporting inorganic growth.

Latest Financial Snapshot and Balance Sheet Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $41mm | |

| 2026-03-31 | ||

| Current assets | $297mm | |

| 2026-03-31 | ||

| Current liabilities | $91mm | |

| 2026-03-31 | ||

| Current ratio | 3.27x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of the quarter ended March 31, 2026 [F1], liquidity metrics reflect a solid financial foundation supportive of operational flexibility:

| Metric | Amount (USD million) |

|---|---|

| Cash & Equivalents | 41.0 |

| Current Assets | 297.4 |

| Current Liabilities | 90.9 |

| Current Ratio | 3.27 |

The current ratio above 3 indicates strong short-term coverage of liabilities. Total debt figures from earlier periods approximate $430 million with net debt around $389 million considering cash holdings; no recent statements indicate altering leverage ratios significantly [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments