CSLM Digital Asset Acquisition: Building a Bridge to Frontier Market Blockchain Ventures

Analyzing CSLM Digital Asset Acquisition Corp III’s SPAC formation, capital deployment, and strategic focus on digital assets in frontier markets.

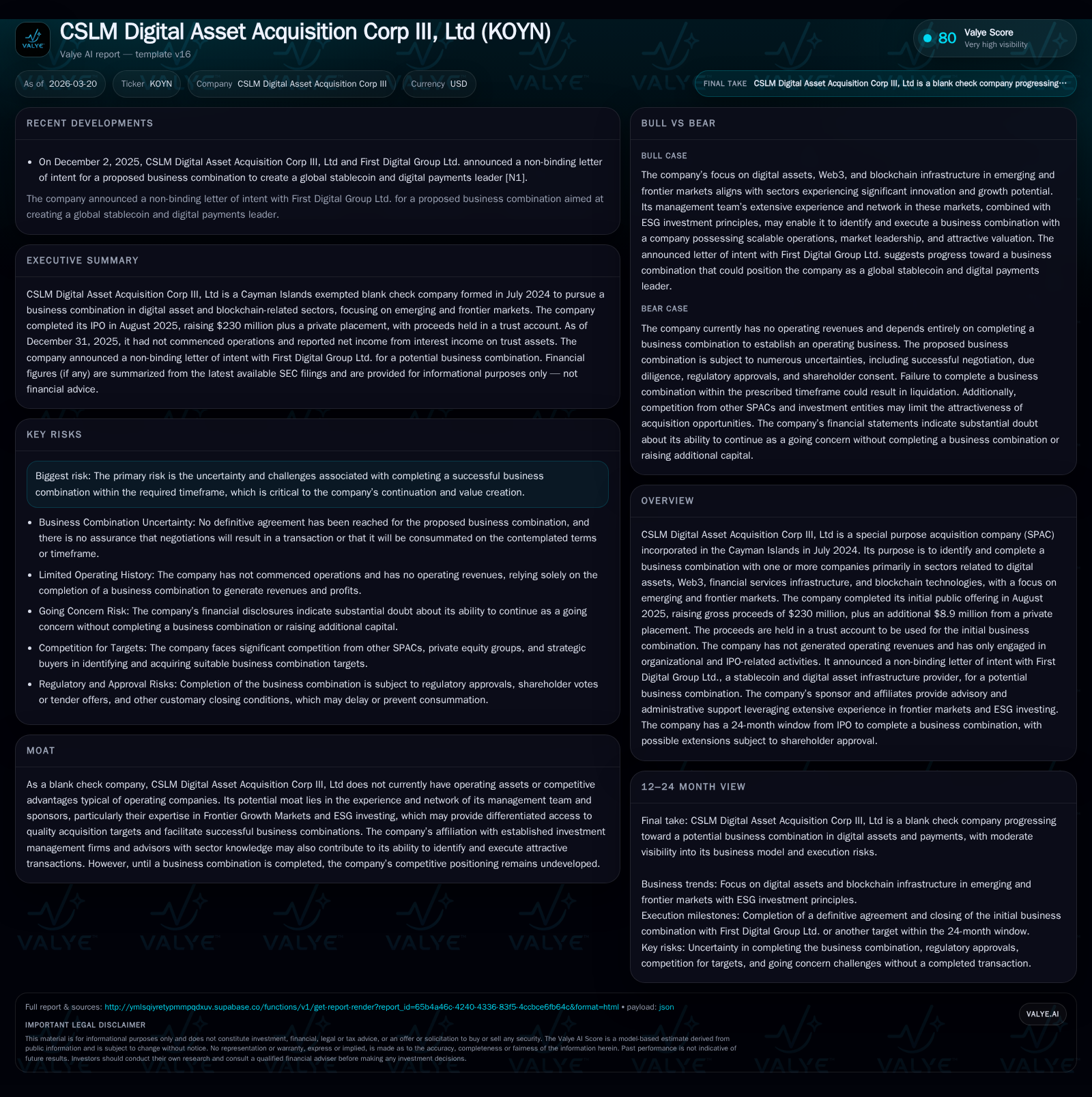

CSLM Digital Asset Acquisition Corp III, Ltd (KOYN) is a Cayman Islands-incorporated blank check company formed in July 2024 targeting digital asset infrastructure and blockchain-related businesses primarily in emerging and frontier markets. It raised gross proceeds of $230 million in its August 2025 IPO plus an additional $8.9 million via private placement, with funds held in trust for a future business combination. The company has no operating revenues to date but recorded net income driven by trust account interest; operational expenses reflect typical organizational costs. Success hinges on completing a quality initial business combination within the mandated timeframe, leveraging management's experience and network to access underpenetrated markets characterized by scalable platforms and ESG-focused companies. Capital allocation remains conservative pre-combination with no dividends or buybacks planned, while governance structures provide sponsor alignment but potential dilution risks persist. Market watchers should monitor deal announcements and shareholder voting events as catalysts.

Foundation and IPO Outcome: Establishing Capital for a New Frontier Play

CSLM Digital Asset Acquisition Corp III, Ltd was formed as a Cayman Islands exempted company in late July 2024 specifically as a Special Purpose Acquisition Company (SPAC). Its mandate centers on effecting an initial business combination with companies primarily engaged in digital assets, Web3 technologies, financial services infrastructure, or blockchain-driven business models particularly within emerging and frontier markets [S1]. In August 2025, KOYN completed its IPO raising $230 million through issuance of 23 million units priced at $10 each, including full exercise of overallotment options [S1]. Alongside this public offering, a private placement sold approximately 891,250 units for $8.9 million to the sponsor and Cohen & Company Capital Markets (CCM), who also acted as underwriter [S1].

Each unit consists of one Class A ordinary share coupled with half of one redeemable warrant exercisable at $11.50 per share subject to adjustments [S1]. Notably, net proceeds—after accounting for underwriting fees including deferred commissions—were deposited into a newly established Trust Account dedicated to preserving capital for acquiring target(s) [S1][S8]. This trust structure preserves investor funds securely pending consummation of a qualifying business combination.

The SPAC model inherently brings an upfront dilution layer due to warrants issued and founder shares held by sponsors under lockup provisions that prevent transfers until after completion of the initial combination [S1]. Moreover, additional equity or preferred stock offerings may be required alongside debt instruments in financing any future merger or acquisition activity [S1]. These factors highlight potential shareholder dilution risks inherent to SPACs like KOYN.

Historical Financial Snapshot: Organizational Costs Without Operating Revenues

Through its inaugural full fiscal year ending December 31, 2025, KOYN did not engage in revenue-generating operations consistent with its blank check status; all activity related mainly to organizational setup, IPO preparation, search for acquisition targets, and due diligence efforts [F1][S8].

Operating income was negative approximately $861k as operational expenses—including administrative costs ($799k), insurance ($26k), listing fees ($35k), share-based compensation ($559k), amongst others—offset interest income generated from the Trust Account (~$3.25 million) and short-term investments [F1][S8][S14]. This resulted in positive net income just under $1.85 million reflecting the unique accounting effect of non-operating revenues exceeding expenses during this phase [F1].

Liquidity-wise, cash and equivalents stood around $3.1 million at year-end 2025 compared to zero prior year-end when initial funding had not yet closed [F1][S5]. Including treasury securities held within the Trust Account valued over $233 million toward acquisition capital demonstrates robust available resources [F1][S13]. Current assets totaled roughly $3.18 million against current liabilities near $210k delivering an exceptionally high current ratio exceeding 15x indicative of strong short-term solvency at this nascent stage [F1].

Return on equity registered negative circa -29.9% reflecting losses from operations before any post-IPO growth activity can ramp up—a common profile among early-stage SPACs where capital preservation rather than immediate profitability is prioritized [F1].

Strategic Focus on Frontier Markets and Web3 Infrastructure

CSLM Digital Asset Acquisition intends to capitalize on growth opportunities within underpenetrated frontier markets characterized by sizable total addressable markets (TAM) fueled by favorable demographic trends such as expanding middle classes across geographically extensive regions [S6]. The SPAC targets businesses possessing scalable platforms that facilitate geographic expansion and synergies through acquisitions [S6]. Essential investment criteria emphasize sector-leading KPIs—metrics that gauge sustainable unit economics crucial to driving profitability and free cash flow generation post-combination [S6].

Leadership quality also features prominently; prospective partners must exhibit competent management capable of navigating public market transitions alongside disciplined corporate governance frameworks expected by U.S.-listed entities [S6]. Market leadership defined by strong product capabilities or technology differentiation yielding sustainable competitive moats anchors candidate selection [S6].

In addition, KOYN underscores environmental, social and governance (ESG) considerations aligning with global responsible investing momentum which could enhance valuation trajectories within frontier ecosystem firms otherwise discounted relative to developed peers [S6][S18]. Target companies embedded with positive ESG impacts would likely resonate better with international investors wary of geopolitical or regulatory uncertainties prevalent in developing markets.

Catalysts and Barriers to Successful Initial Business Combination

The company faces stringent temporal constraints mandating consummation of its initial business combination within 24 months of IPO closing or earlier if shortened via shareholder-approved extension amendments [S1][S27]. Failure to meet these deadlines obligates liquidation distributions back to public shareholders from the Trust Account—typically executed at about $10 per share less costs—in effect returning invested capital minus certain fees rather than creating upside value from merged operations [S1][S27].

Business combination deals may issue additional equity classes (preference shares) or debt securities incorporating senior rights vis-à-vis ordinary shares potentially diluting existing investors’ ownership percentages or weighting control dynamics unfavorably without pre-emptive rights protections present for public participants [S1]. Covenants attached to any such indebtedness may restrict further financing flexibility while amplifying default risk if post-merger cash flows fail expectations—a material consideration given the instability common among target firms at early stages [S1][S4][S7].

SPAC closing processes frequently encounter negotiation challenges stemming from price disputes, due diligence findings prompting delays or deal re-writes, regulatory approval hurdles especially considering frontier jurisdictions’ evolving compliance standards plus potential shareholder vote controversies involving redemption rights exercises affecting deal viability [S2][S4][S12]. The Sponsor’s influence on voting outcomes coupled with possible lock-up waivers introduces additional complexity.

Capital Structure, Liquidity Profile, and Going Concern Considerations

As detailed above, KOYN’s capital base resides largely within its Trust Account ($233 million) reserved exclusively for acquisition transactions alongside a smaller operational cash pool ($3.1 million) utilized for corporate expenses such as administration fees paid monthly ($30k contract per month) under agreements with the Sponsor’s affiliates [F1][S5][S15][S22]. Founder’s Class B ordinary shares issued prior to IPO convert one-for-one into Class A shares post-combination subject to adjustments reflecting overall equity issuances ensuring Sponsors retain an approximate quarter ownership on the fully diluted basis excluding redemptions—a standard structuring technique aligning incentives while formally underpinning dilution buffers that protect public shareholders’ stakes [S9][S23].

KOYN carries no long-term debt but does note substantial deferred underwriting commission liabilities totaling nearly $9.2 million recognized as non-current liabilities impacting comprehensive capital allocation statements absent any dividends or share buybacks initiated at this preliminary phase where conservation of capital takes precedence pending merger success [F1][S13][S27].

Management disclosed going concern uncertainties explicitly citing dependence on timely execution of a qualifying business combination or alternative capital injections via Working Capital Loans from Sponsor-linked parties; absence of such outcomes would jeopardize operational continuity beyond the trust fund lifecycle given zero operating cash flow historically recorded thus far—which typifies typical blank check company risk profiles albeit partially mitigated here by sizeable trust reserves designated strictly for acquisition use barring expenses incurred outside such Fund [S5][S11][S14].

Forward-Looking Insights: Market Opportunities and Monitoring Milestones

Digital asset infrastructure globally is undergoing accelerating adoption especially across underbanked emerging economies where blockchain technologies promise cost efficiencies fueling transactional scalability absent legacy intermediaries. This secular tailwind bolsters CSLM Digital Asset Acquisition’s rationale centering investments upon companies poised at the nexus of technological innovation tied closely with vital geographical expansion potential enabled by local partnerships—as explored through their letter of intent with First Digital Group Ltd., a stablecoin infrastructure provider engaged during Q4 2025 signaling strategic intent though formal agreement remains unclosed as of latest filings ⸺ highlighting evolving deal dynamics still subject to customary contingencies such as further due diligence review board approvals licensing compliance plus market conditions layered atop regulatory evolutions impacting digital currencies worldwide [S10].

Corporate watchers would do well tracking press releases announcing binding term sheets or definitive agreements alongside scheduled shareholder meetings convened either for voting on definitive merger plans or tender offer disclosures generally filed roughly four weeks prior giving shareholders redemption opportunities coupled with concurrent proxy materials illuminating financial metrics expected post-merger including pro forma capitalization structures yet foregoing numeric financial forecasts due lack of guidance presently furnished by management limiting forward quantification beyond qualitative strategic parameters outlined herein.

Governance, Sponsor Influence, and the Importance of Network Effects

Governance adopts industry-standard provisions including independent director majorities conformant with Nasdaq regulations featuring five independent directors offering oversight complementing sponsor vested interests aligned principally through ownership stakes via private unit acquisitions accompanied by associated registration rights granting liquidity windows safeguarding minority investor exit capabilities under various scenarios preventing sponsor entrenchment unchecked empowerment typical critiques leveraged against some blank check entities absent such safeguards [S19][S20][S26].

Sponsor CSLM Acquisition Sponsor II Ltd managed internally via entities controlled predominantly by founders Charles T Cassel III and Vikas Mittal leverages complementary sector know-how particularly focused telegraphs selective deployment into venture arenas favoring Frontier Growth Markets thereby banking on network effects whereby access exclusivity intensifies deal pipelines enhancing probability weighted value accretion during hunt phases thereby de-risking valuation complexities intrinsic within nascent ecosystems relative broader mainstream sectors [S21]. Their consulting arrangements embed periodic fees incentivizing active participation while deferring payoff linking ultimate returns tightly aligned with successful combinations [S16]. Such structural mechanisms cumulatively underpin KOYN’s credible positioning amid competitive SPAC cohorts.

Financial Performance Summary

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

This table illustrates CSLM Digital Asset Acquisition's nascent financial footprint marked by non-revenue generation typical of early-phase SPACs poised for transformational business combinations.

This analysis is provided solely for informational purposes without investment recommendations. Readers should conduct their own due diligence before making any decisions involving securities issued by CSLM Digital Asset Acquisition Corp III or related entities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments