Lotus Technology Accelerates EV Innovation but Faces Liquidity Headwinds

Recent delivery growth and product innovation underpin Lotus Technology’s expansion, while liquidity stresses and operational weaknesses temper near-term prospects.

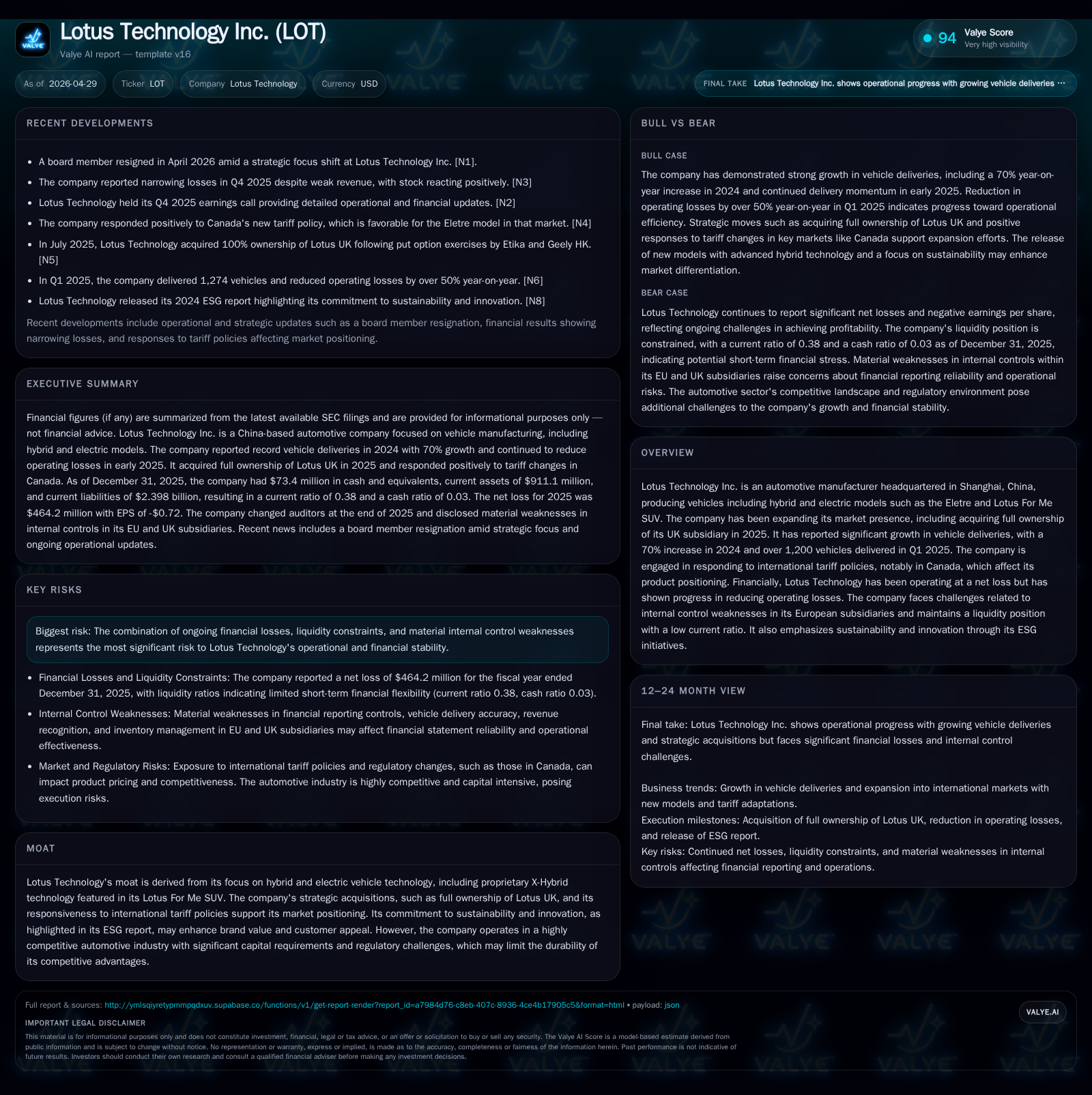

Lotus Technology’s latest quarterly filing reveals significant vehicle delivery growth and narrowing operating losses driven by new hybrid electric models and increased UK market control. Its business model leverages proprietary X-Hybrid technology and a mix of lifestyle EVs alongside luxury sports cars from its UK subsidiary. However, persistent liquidity constraints reflected in a current ratio below 0.4 and high leverage, combined with material internal control deficiencies in European operations, pose operational challenges. Growth hinges on successful scaling of new product lines and expanding geographic reach amid tariff policy complexities. Key near-term milestones include margin improvement efforts, resolution of control issues, and continued shipment volume gains.

Latest Quarterly Update and What It Signals

Lotus Technology’s April 10, 2026 6-K filing discloses notable progress in vehicle deliveries alongside continuing operational challenges that frame its near-term outlook [S2]. The company reported over 1,200 vehicles delivered in Q1 2025, reflecting robust expansion following a reported 70% year-over-year increase across full year 2024 [S2][N1][N2]. Despite this volume surge, total revenues decreased relative to peaks in prior periods as pricing pressures, tariff impacts, and channel adjustments offset some revenue gains [S2]. However, operating losses narrowed compared to previous quarters, signalling improving cost efficiencies amid scaling production.

The filing flagged ongoing internal control weaknesses within its European subsidiaries affecting key financial reporting processes such as revenue recognition accuracy and inventory reconciliation compliance [S25]. These issues underscore ongoing governance sensitivities that could impair timely financial transparency or operational reliability outside China.

Enhanced responsiveness to international tariff policies — particularly Canadian adjustments — is reshaping export strategies and product placements to mitigate adverse margin impacts. Overall, the quarter reinforced the dual narrative of accelerating market traction through product launches versus exposed governance and liquidity vulnerabilities constraining crisp execution.

Business Model Overview and Product Differentiators

Lotus Technology operates principally as an automotive manufacturer specializing in advanced electric and hybrid vehicles combining luxury appeal with technical innovation [S1]. Revenue primarily derives from sales of:

- Self-developed EV lifestyle models including the recently launched Lotus For Me SUV equipped with proprietary X-Hybrid technology,

- Luxury sports cars produced under full ownership of Lotus UK,

- Auto parts and peripheral products supporting vehicle ecosystems,

- Automotive design/development services for OEM clients,

- Intelligent driving solutions,

- Logistics facilitation services tied to order processing.

The company employs a vertically integrated R&D approach reflected by over half its global workforce focusing on research functions—underscoring technology leadership as a core moat element [S1]. Proprietary hybrid powertrain tech positions these lifestyle vehicles distinctively amid competitive EV offerings that often lean fully electrical or conventional combustion hybrids without integrated intelligent systems.

High-R&D intensity drives innovation cadence but also elevates cost bases impacting near-term profitability. Service revenues add diversification but remain modest relative to goods sales. The mix between volume-driven production sales and value-added services offers some resilience but requires precise execution for margin recovery.

Competitive Landscape and Lotus's Moat

Within the global automotive marketplace increasingly dominated by legacy incumbents pivoting toward electrification (e.g., Tesla, BYD) and emerging pure EV challengers (e.g., NIO), Lotus carves a niche leveraging hybrid innovation blended with luxury branding acquired through its UK subsidiary integration [S1].

Its proprietary X-Hybrid tech offers differentiated performance versatility absent in many competitors' portfolios that tend either toward battery-electric or mild hybrids. Consolidation under Lotus UK enhances brand prestige alongside broadens product mix—from ultra-luxury sports cars to practical lifestyle SUVs—enabling cross-segment coverage uncommon among pure EV startups.

However, like many automotive manufacturers moving into electrification, Lotus contends with capital-intensive production scale-up demands amid complex global supply chains stressed by commodity inflation. Tariff volatility adds another layer of commercial risk constraining pricing power sustainability.

Operationally weak internal controls hamper investor confidence while liquidity constraints limit agility for rapid capacity expansions or marketing spend intensification—both vital for maintaining competitive stance in this aggressive segment [S25][F1]. Consequently, Lotus’s moat appears moderated: strong on technology differentiation but pressured by financial and operational execution risks.

Growth Drivers Rooted in Innovation and Market Expansion

Lotus’s growth strategy revolves around several pillars supported by its recent filings:

- Hybrid/Electric Vehicle Production Scale: The increased delivery volumes validated by Q1’s >1,200 units exhibit more than tactical demand; they indicate capacity ramping with efficiency gains expected from stabilized assembly lines [S2][N1].

- Product Portfolio Expansion: Launching the Lotus For Me SUV featuring X-Hybrid tech broadens addressable market segments beyond traditional sports car buyers into luxury lifestyle crossover customers seeking sustainability without performance compromise [S3][S1].

- Geographic Penetration: Full ownership consolidation of Lotus UK enables deeper marketing synergy across Western Europe while facilitating better navigation of tariff regimes affecting North American exports specially articulated for Canada exposure [S1].

- Service Line Development: Ancillary businesses providing design consulting and logistics facilitation augment steady revenue streams enhancing client stickiness and cross-selling potential [S1].

These growth drivers depend critically on smooth operational scaling free from supply bottlenecks or managerial distractions arising from governance lapses. Their success will manifest measurably in booking growth rates, product cycle times (SKU cadence), geographic sales mix shifts, as well as service contract volume uptick.

Operational and Financial Risks to Monitor

Despite encouraging delivery data and narrowing losses, material risks persist:

- Internal Control Weaknesses: Identified deficiencies in EU/UK subsidiaries related to journal entries approval processes, inventory counts accuracy, revenue recognition controls reflect systemic challenges that could delay financial close cycles or invite restatements implicating reputational damage [S25].

- Liquidity Constraints: With cash reserves standing at $73.4 million against total debt nearing $129 million (yielding net debt approx. $55.4 million) plus a current ratio of only 0.38 at fiscal year-end 2025—working capital pressures threaten day-to-day operational fluidity without fresh capital infusion or cash flow improvement from operations [F1].

- Tariff Exposure: Fluctuating trade policies necessitate constant adjustment costs with potential margin erosions especially on targeted export markets like Canada where tariff changes have driven responsive repositioning strategies influencing product price-mix decisions.

- Governance Transitions: Recent board member resignation indicates potential strategic reassessments that may delay decision cycles or unsettle stakeholder confidence pending clarity on long-term capital allocation priorities [N3].

- Capital Intensity: Continuous R&D spending (~51% workforce focus) demands sustained financing which may exacerbate dilution risks if equity or debt markets tighten further per disclosed risk factors [S1].

Together these factors impose hurdles that could slow down turnaround efforts or cause volatility around profitability milestones.

Key Milestones and Forward-Looking Indicators

Stakeholders should closely track these developments as bellwethers for progress:

- Post-Q1 vehicle delivery trajectory confirming sustained ramp beyond early 2025 levels;

- Quarterly margin improvements signaling operational leverage realization;

- Resolution progress on internal control remediation plans signaled through audit commentary updates;

- New product announcements or regional facility expansions corroborating growth strategy execution capacity;

- Updates on tariff implications particularly after trade negotiations or regulatory announcements impacting export economics;

- Board composition changes reflecting eventual strategic clarity.

Monitoring these KPIs regularly via subsequent filings will illuminate the viability of Lotus Technology’s growth transition phases.

Current Financial Snapshot and Liquidity Assessment

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $73mm | |

| 2025-12-31 | ||

| Total debt | $129mm | |

| 2025-12-31 | ||

| Net debt | $55mm | |

| 2025-12-31 | ||

| Current assets | $911mm | |

| 2025-12-31 | ||

| Current liabilities | $2.4bn | |

| 2025-12-31 | ||

| Current ratio | 0.38x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD million) | Period End |

|---|---|---|

| Cash & Equivalents | 73.4 | |

| 2025-12-31 | ||

| Total Debt | 128.9 | |

| 2025-12-31 | ||

| Net Debt | 55.4 | |

| 2025-12-31 | ||

| Current Assets | 911.1 | |

| 2025-12-31 | ||

| Current Liabilities | 2398.1 | |

| 2025-12-31 | ||

| Current Ratio | 0.38 | |

| 2025-12-31 |

This analysis synthesizes recent SEC filings alongside publicly available news disclosures to assess Lotus Technology Inc.’s position at the intersection of rapid electric vehicle market growth challenges compounded by financial structuring stresses. The company exhibits promising technological differentiation powered by hybrid innovations yet must contend with palpable operational governance weaknesses and liquidity demands limiting near-term flexibility.

Disclaimer: This analysis does not constitute investment advice or recommendations but is intended solely for informational purposes grounded on disclosed regulatory filings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments