SunCar Technology Builds Growth Momentum on Auto eInsurance and AI Integration

SunCar’s recent surge in EV auto insurance premiums combined with advances in AI-enhanced technology platforms underscores its expanding ecosystem and operational scalability in China’s auto insurance sector.

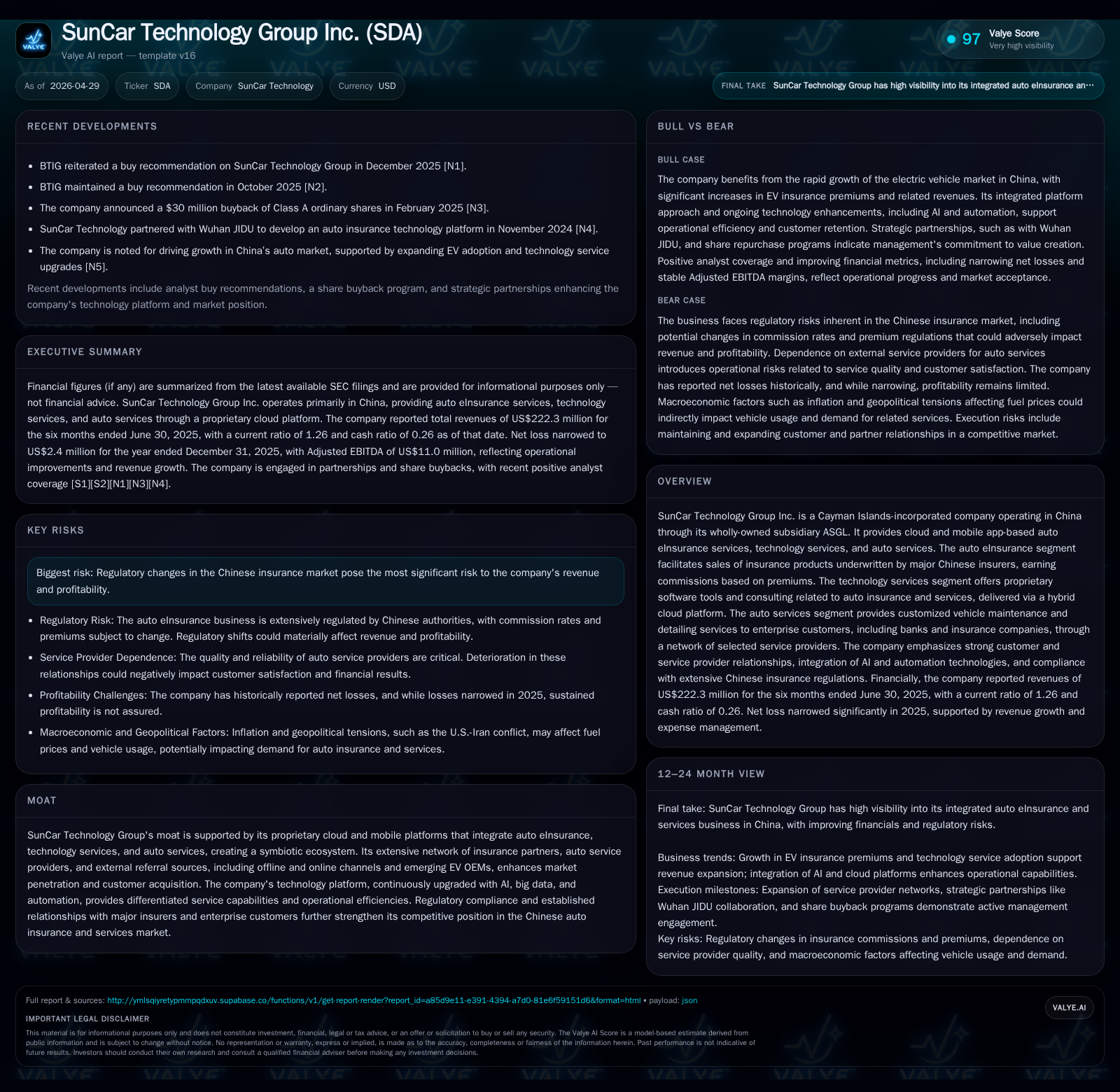

SunCar Technology Group Inc. reported a significant increase in electric vehicle (EV) insurance premium volume and corresponding commission revenues in its latest quarter, reflecting accelerating demand for its cloud-based auto eInsurance services. Concurrently, the company is progressing on transitioning its technology service offerings toward a SaaS model enriched by AI integration, which bolsters both partner efficiency and customer retention. The company’s integrated business model synergizes auto eInsurance commissions, technology services, and enterprise auto service contracts, creating a moat through proprietary platforms and a vast partner/referral network. Regulatory changes within China’s insurance space and reliance on service providers remain critical watchpoints.

Recent Quarterly Operating Highlights and Implications

In its latest quarterly filing dated February 3, 2026 [S2], SunCar Technology Group highlighted continued momentum in its core auto eInsurance business fueled primarily by a soaring electric vehicle (EV) insurance market. For the year ended December 31, 2025, EV auto insurance premiums climbed by nearly 50% compared to the prior year ($1.524 billion vs. $1.020 billion) [S1]. This translated to a substantial $66.2 million revenue from EV insurance commissions—up over 50% from the previous year. Such robust premium growth reflects the structural acceleration of EV adoption in China, where insurance penetration tied to new energy vehicles is expanding rapidly.

On the technology services front, revenue increased by 19% from $44.9 million in 2024 to $53.6 million in 2025, evidencing strong uptick in enterprise uptake of SunCar’s proprietary software tools deployed via its hybrid cloud platform [S1]. These offerings include CRM systems, order/finance management modules, and analytics—all pivotal for streamlining workflow automation among sales partners and service providers.

Operationally, the company has started shifting from traditional licensing toward a SaaS product offering that promises higher recurring revenues and client stickiness through continuous feature upgrades powered by AI integrations. The quarterly report detailed ongoing iterative platform upgrades further embedding AI intelligence into internal workflows and partner processes [S1], which aligns with industry trends favoring scalable cloud-native SaaS architectures.

Meanwhile, SunCar’s auto service segment posted relatively stable revenues but experienced slight volatility due to modest shifts in service orders during the period [S21]. The cross-segment synergy remains key: many auto services providers also serve as sales partners for the eInsurance business, enabling mutual growth.

Business Model Overview: Multi-Segment Integration in Auto eInsurance

SunCar operates through three interrelated segments—auto eInsurance services, technology services, and auto services—all anchored by its proprietary cloud/mobile applications connecting insurers, customers, enterprise clients, and service providers [S1].

The core revenue driver stems from commissions earned on facilitating auto insurance policy sales underwritten by established Chinese insurers. Typically structured as a percentage fee on gross premiums collected from customers digitally accessing a wide product portfolio via SunCar’s platforms.

Simultaneously, SunCar monetizes a modular suite of technology tools offered to insurance sales force members and vehicle service providers—for managing CRM tasks, order processing, finance tracking, and visual data analysis—transitioning these offerings toward a subscription-style SaaS model that encourages long-term client retention.

In tandem is the B2B-focused auto services business delivering maintenance and detailing packages customized for large enterprises such as banks or insurance firms managing fleets or client incentives programs. End-user delivery is outsourced to select regional providers vetted within SunCar’s expanding national network.

This tightly integrated operating model fosters multiple customer lock-in points—from policyholder acquisition on one end to consistent usage of software tools supporting partner workflows on the other—generating considerable switching costs while enhancing overall ecosystem value [S1].

Proprietary Technology Platform and Service Quality Differentiation

SunCar's hybrid cloud platform combines several backend operational modules: CRM for customer engagement tracking; order management tailored for seamless transaction processing; financial controls ensuring accuracy of commissions/fees; plus visual analytic dashboards providing actionable insights. Critically, this platform is augmented with AI-powered automation designed both to optimize internal resource deployment and empower external partners with enhanced service capabilities [S1].

The company reports ongoing efforts at embedding AI within workflow processes such as underwriting support tools for insurance products, fraud detection mechanisms potentially reducing loss ratios indirectly benefiting insurers' willingness to collaborate under favorable terms, and digital assists simplifying complex administrative tasks across sales networks.

This technological edge differentiates SunCar in an otherwise fragmented market characterized by diverse service quality levels especially across local auto maintenance vendors who rely heavily on third-party platforms for lead generation and customer interface management.

Furthermore, platform scalability enables rapid onboarding of new external referral channels including emerging electric vehicle OEMs who increasingly require efficient digital ecosystems linking customers to tailored insurance policies alongside ancillary car maintenance solutions—a trend signifying deeper integration opportunities across automotive lifecycle services beyond mere insurance brokerage [S1].

Competitive Positioning Within China’s Growing Auto Insurance Industry

SunCar operates amid a highly competitive landscape shaped by major state-backed insurers underwriting policies distributed through multiple channels including direct salesforces and online aggregators. The company carves out distinction by leveraging exclusive partnerships with principal underwriters alongside an extensive network of offline after-sales distributors frequently interfacing with car owners using digital platforms supplemented with mobile apps facilitating faster policy shopping experiences.

Moreover, collaboration with emerging EV manufacturers establishes direct upstream referral relationships at vehicle sale points—critical since EV buyers often require bundled financing plus tailor-made insurance solutions that integrate seamlessly at purchase time rather than post-sale reactive policies common among traditional insurtech players.

Its ecosystem approach combining tri-segment synergies creates practical entry barriers for competitors: the accumulated data assets linking user behavior across policy purchases, usage patterns via software tools usage metrics, plus feedback loops capturing service provider quality reviews enable ongoing improvement cycles difficult to replicate swiftly by newer entrants without deep investment.

However, regulatory strictures governing licensing requirements for online insurance distribution agents impose compliance burdens that act both as barriers protecting incumbents yet simultaneously constrain nimble innovation cycles if regulatory changes introduce new commission capping or licensing hurdles reflective of shifting government priorities within China's broader financial reform agenda [S1], [N/A analysis context].

Growth Drivers: EV Market Expansion, SaaS Transition, and AI Enhancements

The foremost structural growth enabler is China’s accelerating EV adoption pushing exponential demand for specialized coverage products—SunCar’s surge in EV-related premiums (+49%) directly validates this secular tailwind [S1]. This dynamic creates volume-driven expansion opportunities not only through commission income but also upsell potentials into value-added products such as usage-based policies facilitated through digital platforms embedded with telematics data.

The parallel momentum lies within the company’s gradual pivot to SaaS-based monetization models where increasingly sophisticated software tools create predictable recurring revenue streams while deepening enterprise client engagement reducing churn risks associated with transactional license deals.

AI incorporation stands out as a multiplier effect enhancing operational leverage—automation lowers incremental servicing costs for growing contract volumes while improving real-time responsiveness crucial for retaining tech-savvy institutional customers demanding seamless digital experiences [S1].

Additionally noteworthy is the broadening partnership base blending offline industry trusted referral sources plus high-traffic digital platforms—this multichannel sales approach boosts lead funnel robustness mitigating channel concentration risks typical of pure-play online distributors.

Risks and Constraints: Regulatory Exposure and Service Provider Relations

The dominant risk vector remains regulatory shifts impacting commission structures or online distribution licensing conditions potentially compressing margins or limiting market access [S1]. Regulatory tightening may also enforce heightened consumer protection mandates increasing compliance costs adversely affecting profitability profiles.

Operational constraints arise from reliance on quality-controlled service provider networks fulfilling the auto services segment contracts. Deterioration in provider performance or disputes could tarnish brand reputation thus dampening customer loyalty critical given feedback-driven purchase repeat rates foundational to sustaining long-term growth trajectories.

Market competition intensifies as other insurtech firms continuously enhance their own tech stacks or forge exclusive insurer relationships necessitating sustained R&D investment coupled with prudent partner ecosystem management balancing scale against service quality control challenges.

Finally currency risks exist given RMB-denominated predominant cashflows alongside foreign listings necessitating diligent FX risk oversight amidst evolving PRC capital control policies potentially restricting offshore repatriations or dividend flows without bureaucratic delays [S3], [N/A analysis context].

Outlook & What to Watch: Milestones for Customer Acquisition and Platform Development

Monitoring execution milestones around enterprise contract win rates for SaaS products will be key indicators signaling traction beyond initial license sales toward sustained subscription expansions [S2], [S1].

Further announcements detailing AI functional enhancements or integration deployments across partner workflows can offer insights into technological moat depth evolution impacting future cost structures positively.

Growth validation may emerge from broadened collaboration announcements linking SunCar’s platform directly with more EV OEMs or new insurance underwriters diversifying risk pools thereby enriching product mix offering options.

Regulatory updates concerning online insurance agent frameworks or commission regulations bear close attention due to their direct impact on revenue mechanics potentially triggering structural margin resets.

Lastly, developments around the stability or expansion of the auto service provider network—including qualitative metrics related to customer satisfaction ratings—would serve as bellwethers reflecting sustained brand strength critical for end-customer trust aggregation within this integrated ecosystem model.

Financial Condition Snapshot: Liquidity, Leverage, and Investment Funding

As of mid-2025 data extracted from companyfacts herein provides relevant liquidity context: cash and equivalents stand at approximately $24.3 million against total debt near $83.1 million generating net debt around $58.8 million; current assets exceed current liabilities producing a current ratio of roughly 1.26 indicative of adequate short-term asset coverage relative to obligations [F1].

Capital expenditures focused primarily on cloud infrastructure development reached about $8.9 million in 2025 funded by bank borrowings supplemented intermittently by equity issuances confirming deliberate reinvestment posture geared towards digital platform enhancement supporting near-term growth aims [S4], [S3].

Management states confidence that existing liquidity combined with projected cash flow generation should fund anticipated capital requirements for at least twelve months barring unexpected market disruptions requiring significant capital raises risking shareholder dilution or covenant restrictions on debt instruments [S3], [N/A external context analysis].

Disclaimer: This report is prepared solely for informational purposes based on publicly available filings as of April 2026. It does not constitute investment advice or a recommendation regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments