AMERICA MOVIL SAB DE CV Strengthens Operating Leverage and Capital Allocation Amid Robust Subscriber Growth

Q1 2026 results reveal sustained revenue growth and enhanced profitability driven by postpaid subscriber expansion and operational efficiencies.

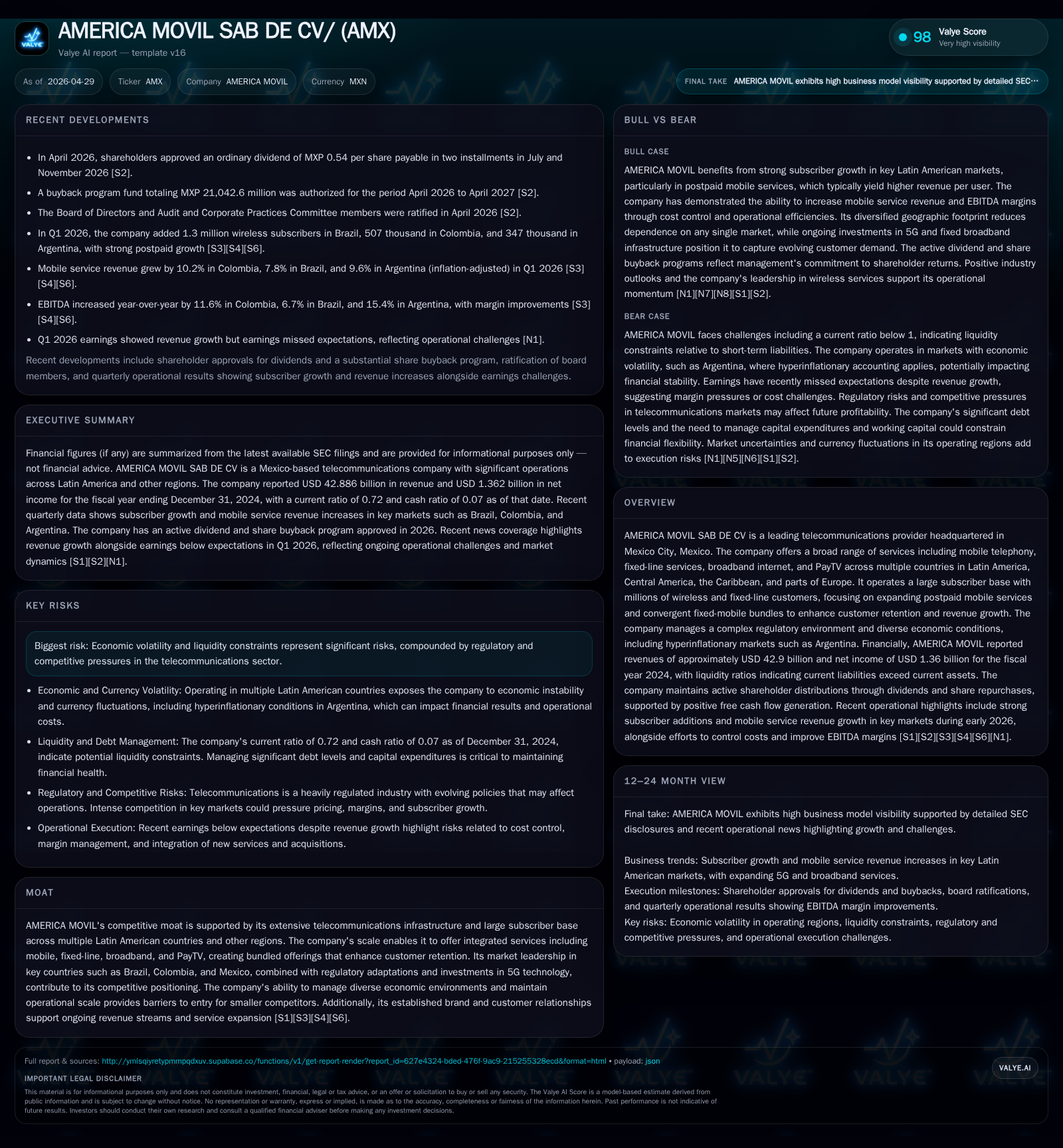

America Movil reported a solid first quarter in 2026, with revenues rising 6.1% at constant exchange rates fueled by a 4.6% increase in service revenue and double-digit equipment revenue growth. The company's EBITDA expanded 8%, outpacing service revenue growth and pushing margins to near-record levels. Subscriber additions were robust, notably in postpaid wireless segments across Brazil, Colombia, and Peru, while fixed-line broadband connections also grew meaningfully. Capital allocation remains disciplined with continued share buybacks and dividend payments amid modest net debt reduction. The company's scale, integrated product offerings, and regional diversification underpin its competitive moat despite economic and regulatory challenges.

Recent Operating Update

America Movil’s latest quarterly disclosures for Q1 2026 highlight a period of accelerated growth marked by resilient subscriber gains, improving margins, and strategic capital deployment [S2][S3]. Revenues grew 6.1% at constant exchange rates, driven by a 4.6% rise in service revenues alongside an impressive 11.3% increase in equipment sales. This balanced top-line expansion laid the foundation for an 8.0% EBITDA increase on a currency-adjusted basis, pushing the consolidated EBITDA margin close to 40%, a peak not commonly seen in recent quarters [S3].

Subscriber traction remains the engine for this performance, with net additions of three million wireless customers—all postpaid—reflecting steady shifts in consumer preference from prepaid to more lucrative postpaid plans. Brazil contributed most heavily with a gain of approximately 1.3 million subscribers; other notable contributors include Colombia adding over a quarter-million and Peru nearly two hundred thousand new clients during the quarter [S3]. On the fixed-line side, the company connected nearly 600 thousand new broadband accesses, emphasizing Mexico's and Brazil's continuing importance as growth engines.

Capital management followed measured steps: net debt stood at 437 billion pesos at the end of March, equivalent to 1.41 times Net Debt to LTM EBITDA, reflecting prudent balance sheet management despite a slight increase in total financial debt compared to December-end figures [S3]. Share repurchases continue under an expanded buyback authorization totaling over MXP21 billion for April 2026-April 2027, accompanied by planned ordinary dividends split into two installments within the current fiscal year [S2][S26].

Strategically, America Movil reinforced its market foothold with the pending acquisition of approximately 73% of Desktop S.A., bolstering its presence in the Brazilian market upon completion of required regulatory approvals [S15].

Business Model

America Movil operates a multifaceted telecommunications business spanning mobile telephony (prepaid/postpaid), fixed-line services including broadband internet and corporate networks, and PayTV distribution across Latin America, parts of Central America, the Caribbean, and Europe [S1][S5]. The company generates revenue primarily by charging end consumers—both individual users and enterprises—for subscription-based services as well as equipment sales (handsets, modems) tied closely to contract volumes.

Volume drivers encompass subscriber base growth particularly in higher-value postpaid segments that offer greater retention rates and ARPU uplift through bundled product packages combining mobile connectivity with broadband access and pay-TV options. Pricing power benefits from scale economies due to Amx’s extensive regional infrastructure footprint which enables efficient delivery of converged solutions harder for smaller competitors lacking broad network assets to replicate.

Revenue mix trends favor growing equipment sales buoyed by device cycles alongside steadily improving service revenues accelerated by migration from prepaid toward more durable postpaid relationships. Operational leverage benefits emerge as fixed costs dilute over larger subscriber volumes enhancing EBITDA margins—a dynamic observed increasingly in recent quarters where EBITDA growth outpaces service revenue gains [S3].

Customer behavior reflects preferences shifting toward integrated telecom offerings facilitating stickier relationships through contractual bundling; this trend supports stable churn metrics while allowing premium pricing on value-added services such as higher-speed data plans or content packages.

Industry Structure and Competitive Position

The Latin American telecom sector is characterized by oligopolistic structures dominated by a few large incumbents including America Movil (Telcel/Claro brands), Telefónica (Movistar), AT&T Mexico, Vivo (Telefonica Brasil) among others. Competitive pressures vary considerably across countries with different regulatory frameworks influencing pricing mandates, spectrum allocation, interconnection fees, and quality-of-service obligations.

America Movil’s scale affords it several competitive advantages: substantial network infrastructure investments enabling superior coverage especially in less penetrated areas; a vast customer base exceeding tens of millions powering cross-subsidy possibilities between urban/suburban markets; well-established brand recognition reinforcing consumer trust; diversified geographic exposure mitigating country-specific political or economic shocks; plus early adoption of advanced technologies like LTE Advanced Pro and initial rollout steps towards broader 5G adoption enhancing service capabilities [S1][S3][S4].

The company’s ability to offer convergent fixed-mobile bundles uniquely positions it against peers who may focus predominantly on one segment thus raising switching costs for consumers through ecosystem lock-in effects via bundled billing and customer care platforms.

Growth Drivers

- Postpaid Wireless Expansion: Continued shift from prepaid plans driving higher ARPU per user through longer contract terms and value-added services.

- Broadband Penetration: Rising demand for fixed broadband due to increasing data consumption trends supports steady fixed-line subscriber additions.

- Equipment Sales Momentum: Device upgrade cycles increasing equipment revenue streams beyond subscription fees.

- Geographic Diversification: Expansion beyond Mexico into high-growth markets like Brazil, Colombia, Peru aids risk diversification amid macroeconomic volatility.

- Convergent Offers: Bundling mobile, broadband, and PayTV encourages higher customer retention rates.

- Regulatory Evolution: Adaptation to evolving telecom regulation regimes potentially unlocks new investment flexibility (e.g., long-distance switch from concession model to authorization in Brazil).

- Strategic M&A: Acquisition of Desktop S.A. signals proactive consolidation efforts designed to deepen market penetration.

Risks and Watchpoints

- Economic Volatility: Currency fluctuations across operating regions affect consolidated financials with notable exposures in hyperinflationary environments such as Argentina [S1].

- Regulatory Complexity: Navigating varied local regulations requires careful compliance strategies; sudden changes or adverse rulings might impair capital investment or operational freedom.

- Competitive Intensity: Increasing competition from smaller regional players or global entrants may press service pricing or force higher marketing expenditures.

- Technological Transition Risks: Failure to timely deploy next-generation networks like full-fledged 5G could erode competitive positioning.

- Concentration Risks: Heavy dependence on few large markets (Mexico/Brazil) exposes the group to geopolitical risks or saturation limits.

- Leverage Management: Net debt levels stood at 437 billion pesos, equivalent to 1.41x EBITDA, indicating manageable leverage; however, any material negative cash flow shocks could affect debt servicing capacity given sizeable absolute financial obligations [S3].

What To Watch Next

Key milestones include regulatory approval progress for the Desktop acquisition in Brazil alongside integration synergies realized post-close [N1][S15]. Monitoring quarterly subscriber trends will provide clues regarding ongoing migration momentum toward postpaid categories especially under evolving economic conditions [S3][S23]. Additionally, updates on capital expenditures targeting network upgrades or expansions may signal readiness for intensified competition around fiber broadband or advanced mobile technologies.

Dividend payment schedules following shareholder approval imply cash flow confidence but warrant watching for any shifts based on market or operational changes [S2]. Also important is how America Movil manages competitive dynamics tied to ongoing price wars or promotional offers across core markets which can impact margins over time.

Financial Profile Context

Net debt stood near MXN437 billion translating into LTM leverage around 1.41x EBITDA — slightly improved from prior periods — suggesting prudent balance sheet management while funding both capital expenditures (~MXN21 billion covered in Q1) plus shareholder returns through dividends and repurchases [S3]. The current ratio below unity (0.72) marks working capital constraints relative to short-term liabilities but is typical for telecom operators engaged in heavy capex cycles coupled with receivables collection patterns [F1].

Overall liquidity appears sufficient given cash flow generation covers capital needs along with disciplined capital allocation frameworks that prioritize deleveraging when possible amidst favorable free cash flow trajectories recorded recently [S3][F1].

This analysis relies exclusively on publicly disclosed information as of April 2026 without speculative forecasting or investment recommendations. It aims to provide an informed industry perspective centered on America Movil's latest operational disclosures plus structural business context within Latin American telecommunications markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments