Kforce Inc. Faces Modest Revenue Pressure But Advances Technology Staffing Focus in Q1 2026

Q1 2026 results reveal ongoing demand constraints balanced by strategic investment in technology segment and robust liquidity.

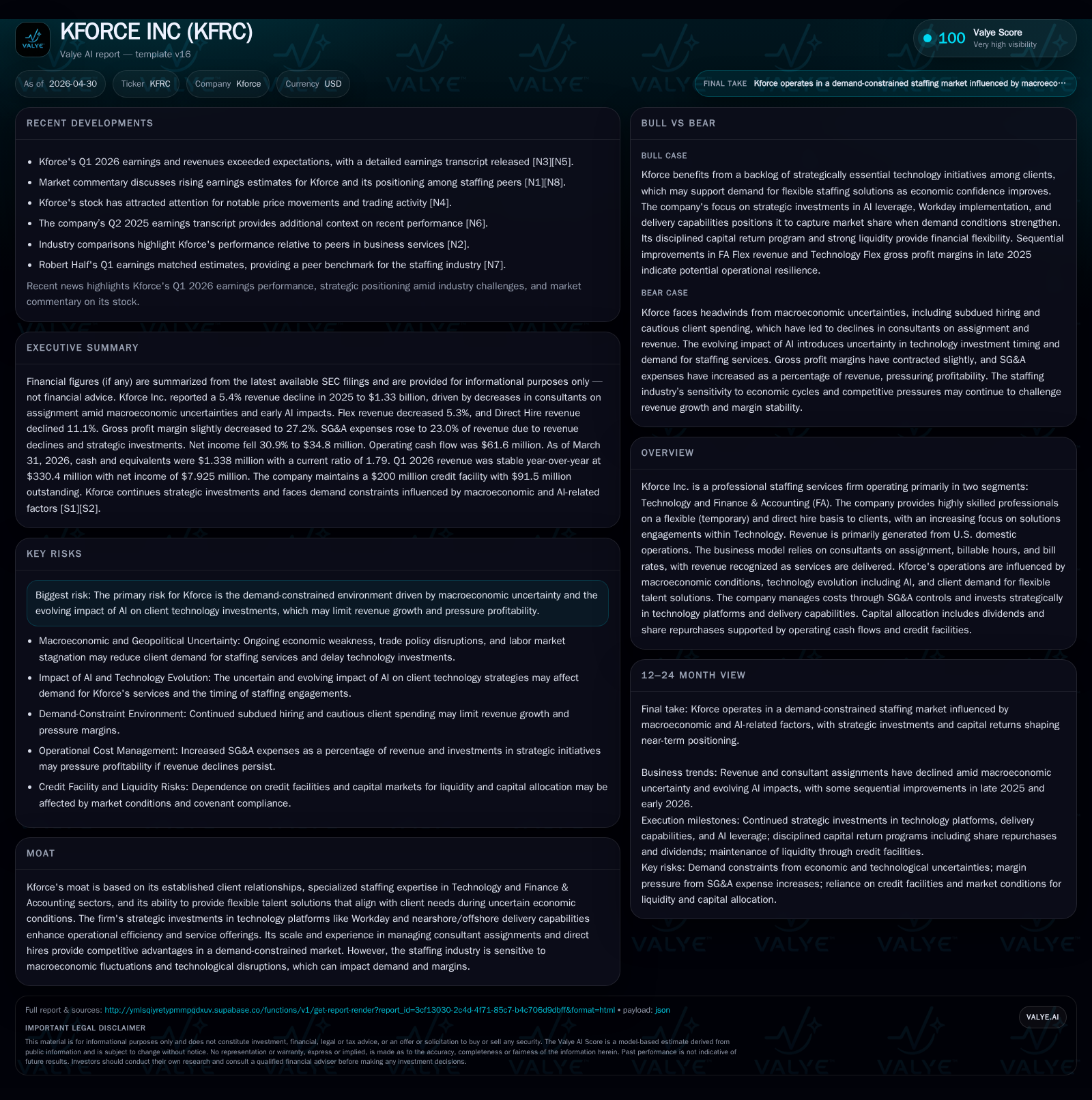

Kforce Inc.'s latest quarterly filing highlights a continuation of the revenue headwinds faced in 2025, largely due to macroeconomic uncertainty and evolving technology adoption cycles. Despite modest declines, the firm is sharpening its focus on Technology staffing and solutions engagements, which show signs of stabilization. The company's flexible talent model paired with strategic investments in platforms supports operational efficiency amid industry challenges. Liquidity remains strong with a solid current ratio and manageable debt levels. Demand constraints tied to AI impact and economic caution remain key risks to watch.

Recent Operating Update

Kforce Inc.'s first quarter 2026 results, as detailed in the April 29, 2026 Form 10-Q filing [S2] supplemented by an earnings release on April 27 [S3], continue to reflect a challenging market environment characterized by cautious client hiring behavior amid macroeconomic uncertainty. Although the company does not disclose detailed Q1 revenue numbers in these excerpts, it signals ongoing moderation of revenue contraction compared to the full year 2025 declines highlighted in the February 2026 annual filing [S1]. Signs of stabilization are most evident in the Technology segment's flexible staffing (Flex) business, which experienced a sequential slow-down of prior declines and even slight improvement on a billing-day adjusted basis late last year.

The April earnings announcement underscores client trends toward leveraging flexible talent solutions as organizations accelerate digital transformation efforts but remain guarded due to economic uncertainties and emerging AI impacts on technology investment lifecycles. Kforce's strategy to deepen engagement in solutions-based offerings within its Technology segment aims to capitalize on this shift by moving beyond traditional staffing towards value-added consulting support.

Business Model Overview

Kforce operates primarily through two reportable segments: Technology and Finance & Accounting (FA). Revenue generation hinges on providing highly skilled professionals either on a flexible (temporary) assignment basis or through direct hire placements to corporate clients predominantly within the U.S. These placements produce revenues based on billable hours at negotiated bill rates for flex engagements or fixed fees for direct hires. Volume drivers include the number of active consultants assigned and their utilization rates.

The firm recognizes that revenue is sensitive to macro factors influencing client hiring appetite and project ramp-up timing. Margins tend to be higher for direct hire services though this mix generally represents a smaller portion of total revenue. In recent periods, Kforce has noted declines in direct hire volumes alongside softer flex demand especially in FA sectors experiencing broader budget constraints.

Strategically, Kforce invests in technology platforms such as Workday implementation capabilities and software tools that enhance operational efficiency for deployment management, billing accuracy, and client servicing. The company also leverages nearshore/offshore delivery resources to balance cost structures while maintaining quality standards.

Industry Structure & Competitive Position

Within the professional staffing landscape, Kforce distinguishes itself through specialized focus verticals—primarily Technology staffing—and its flexible workforce delivery model. The industry is fragmented but marked by competition from large diversified firms like Robert Half alongside niche specialist providers.

Kforce's moat derives chiefly from longstanding client relationships anchored in trust around quality of deployed consultants coupled with agility in scaling talent quickly per fluctuating demand cycles. The firm's structural advantage also lies in its blended offshore/onshore approach that controls cost while supporting complex client requirements.

Technology sector expertise remains critical as businesses increasingly rely on digital platforms yet exhibit prudence amid rapid AI-driven changes that could disrupt traditional IT budgets. Kforce’s move toward solutions engagements positions it well versus pure staffing vendors by embedding itself into client core projectswhich may offer stickiness despite cyclical headwinds.

Growth Drivers

Key growth drivers include:

- Increasing Client Shift to Flexible Staffing: As companies prioritize workforce agility to navigate uncertain economies, demand for flex consultants sustained by Kforce’s scale offers sustained revenue potential.

- Expansion of Solutions Engagements: Moving beyond warm body staffing into consulting-like services adds incremental value-per-client and can improve margins over time.

- Technology Segment Stabilization: Early signs that technology-related flex revenue erosion is abating could signal inflection if market confidence grows.

- Operational Efficiency Enhancements: Investments in proprietary tech platforms improve delivery speed and reduce overhead costs supporting better cost management.

- Capital Allocation Supporting Shareholder Returns: Maintaining dividends and share repurchase programs aligned with cash flow generation bolsters investor confidence.

Risks & Watchpoints

Risks prominently identified include:

- Demand-Constrained Market: Macro-economic uncertainty continues to temper corporate hiring especially for finance roles resulting in sustained headwinds for FA revenues.

- AI Impact on Client Spend: The evolution of AI technologies introduces ambiguity regarding client technology budgets and may delay or alter traditional staffing needs.

- Margin Pressure from Mix Shift: A decline in higher-margin direct hire mix combined with competitive pricing pressure could compress gross margins further.

- Cost Management Challenges: Rising SG&A expenses relative to declining revenues seen in prior periods highlight execution risk in expense control without hurting growth initiatives.

- Leverage & Liquidity Dependence: Although the company’s current liquidity position appears adequate, adverse market shocks impacting cash flows could stress credit facility covenants or dividend/share buyback capacity.

What To Watch Next

Investors should monitor several critical milestones for early indicators of business momentum:

- Q2 reported revenues segmented between Technology and FA alongside any explicit commentary on consultant assignment levels or new bookings

- Gross margin trajectory particularly whether Technology Flex margins continue their modest recovery as observed late 2025

- SG&A expense control effectiveness as Kforce balances reinvestment against operational cost discipline efforts

- Updates on strategic initiatives execution such as expanded solution offerings or platform rollouts enhancing competitive positioning

- Guidance revisions that could signal changing management outlook given persistent market dynamics

Financial Profile Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1.34 billion | |

| 2026-03-31 | ||

| Current assets | $217 million | |

| 2026-03-31 | ||

| Current liabilities | $122 million | |

| 2026-03-31 | ||

| Current ratio | 1.79x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

The company’s current ratio of 1.79x as of March 31, 2026, indicates that current assets exceed short-term liabilities by a comfortable margin, supporting near-term liquidity. More detailed current debt or leverage figures are not explicitly disclosed in recent filings [S2][S3][F1].

Conclusion

Kforce stands at a crossroads where prudent stewardship through ongoing macroeconomic pressures intersects with sizable opportunities inherent in evolving technology-driven labor demand models. Its dual-segment exposure tempers risk but also presents uneven recovery trajectories—Technology showing steadier footing than Finance & Accounting amid cautious corporate spend patterns influenced by broader geopolitical uncertainties and emergent AI innovation waves.

Investments made over past cycles into enhanced platform capabilities and blended delivery models underpin competitive advantages that may support gradual growth resumption provided market confidence strengthens. However, vigilant monitoring of client behavior shifts, margin dynamics, and cost discipline execution will be pivotal as the company navigates an industry landscape both disrupted by technological evolution yet reliant on human capital agility more than ever.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments