YD Bio Establishes Taiwan-U.S. Regulatory Alliance and Advances Ophthalmology Pipeline

Strategic partnership with YC Biotech and acquisition plans mark pivotal steps for YD Bio’s clinical and commercial expansion.

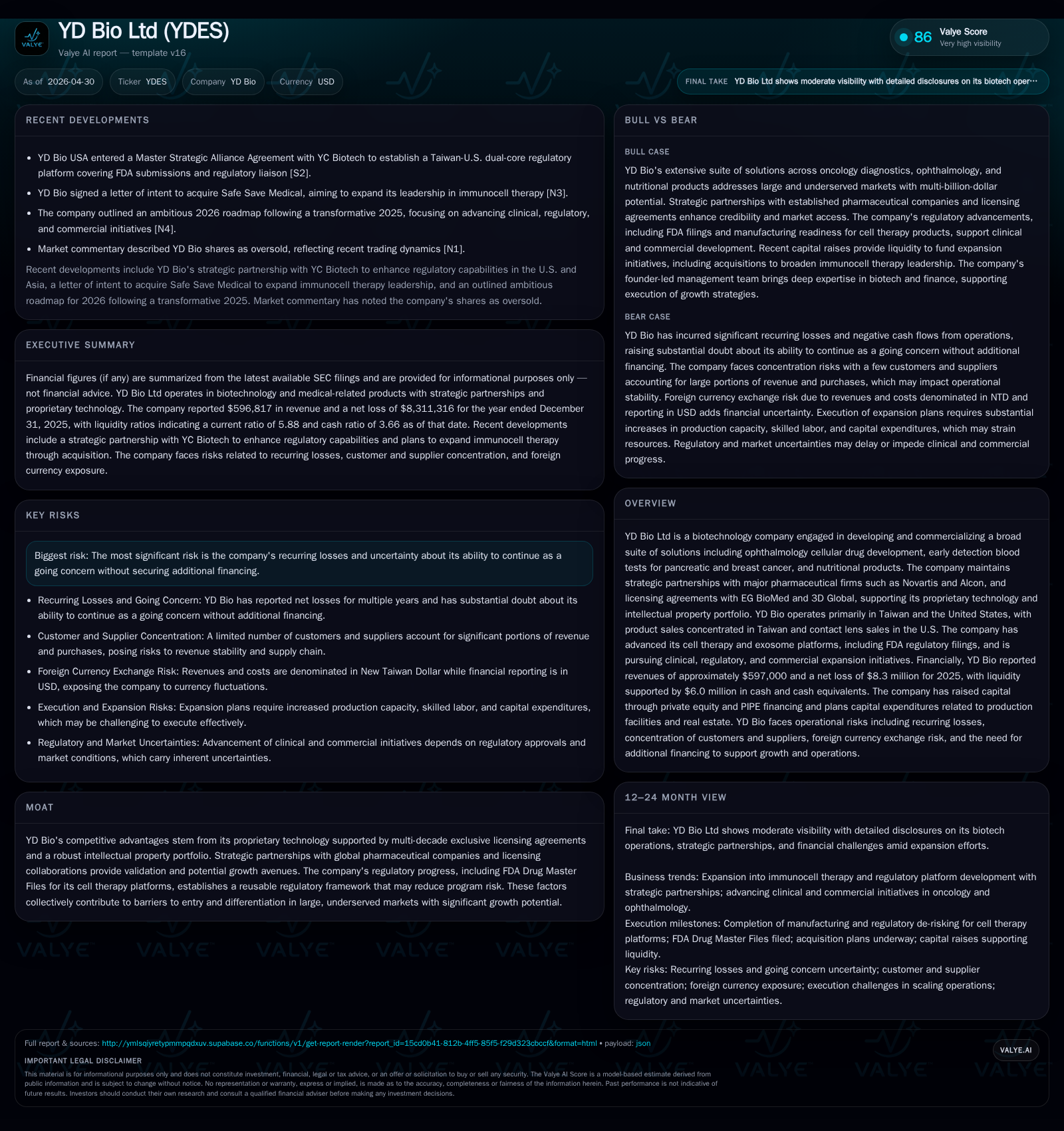

In its latest quarterly update, YD Bio USA formed a Master Strategic Alliance with YC Biotech to build a dual-core regulatory platform facilitating FDA submissions. Concurrently, YD Bio is advancing clinical development of its Limbal Stem Cell (LSC) exosome therapies targeting ophthalmic conditions, backed by a reusable FDA regulatory framework. The company is also progressing a pending acquisition of Safe Save Medical Cell Sciences & Technology, broadening its immunotherapy portfolio. These initiatives underpin YD Bio's strategy to scale through multi-segment healthcare regulated markets, although recurring operating losses and financing needs remain material risks.

Recent Operating Update

In February 2026, YD Bio USA, Inc., a subsidiary of YD Bio Ltd., entered into a Master Strategic Alliance Agreement with YC Biotech Co., Ltd., establishing a "Taiwan-U.S. Dual-Core" regulatory platform focused on navigating U.S. Food and Drug Administration (FDA) processes including Investigational New Drug (IND), New Drug Application (NDA), and Biologics License Application (BLA) submissions [S2]. Under this alliance, YD Bio USA will be the exclusive U.S. agent and FDA liaison for YC Biotech’s Asian contract research organization (CRO) clients, handling regulatory strategy, meeting representation, pre-IND facilitation, inspection readiness, and document preparation. This strategic partnership enhances YD Bio's transpacific reach in managing complex regulatory pathways and positions it as an integrated hub connecting Asian drug development to U.S. markets [S20].

Simultaneously, on March 31, 2026, the company launched the EG Telehealth Platform in collaboration with EG BioMed to support regulated diagnostic test delivery through an independent physician network in the U.S.—an approach aligned with clinical complexity and current expectations around cancer biomarker testing that preclude direct-to-consumer models without physician oversight [S1].

A notable growth initiative underway is the pending acquisition of Safe Save Medical Cell Sciences & Technology Co., Ltd. (SSMC), which specializes in autologous dendritic cell/tumor antigen immunotherapies including late-stage assets for glioblastoma and other solid tumors [S4], [S9]. This $27 million transaction—subject to due diligence and regulatory approvals—is expected to deepen YD Bio’s pipeline breadth in immuno-oncology.

Business Model

YD Bio operates across three synergistic segments: regulated diagnostics primarily in oncology using DNA methylation-based assays under laboratory-developed test (LDT) frameworks; life science clinical services including procurement, logistics coordination, and compliance support tailored to pharmaceutical clinical trials; and healthcare product commercialization encompassing ocular health products in the U.S. and consumer health distribution in Asia [S1], [S16].

Revenue generation is based on sales of diagnostic tests overseen by licensed healthcare providers, service contracts with pharma/biotech companies for clinical trial support, and distribution of medical devices such as contact lenses and associated ocular products. The model emphasizes physician-directed testing paradigms within tightly regulated environments to ensure compliance—a critical factor given variable regulatory landscapes between Taiwan, the U.S., and Asia.

Margins fluctuate depending on product mix: higher-margin proprietary diagnostics contrast with lower-margin resales of medical peripherals or nutritional products [S7], influenced also by procurement efficiencies.

Key proprietary assets include licensed patents from EG BioMed and ThreeD Global supporting DNA methylation cancer tests alongside exosome- and cell-based therapy platforms co-developed with partners such as 3D Global Biotech [S1]. Regulatory filings such as FDA Drug Master Files (DMFs) applied for limbal stem cells (LSC) and derived exosomes establish reusable frameworks reducing duplicative program risk across multiple IND filings.

Industry Structure and Competitive Position

YD Bio operates at the intersection of several high-complexity biotech segments: early cancer detection diagnostics leveraging epigenetics; cell therapy/exosome-based ophthalmology treatments; contract research organizational support for Asian pharma clients seeking U.S. market access; and consumer healthcare product commercialization. The industry features intense R&D-driven competition from specialized biotech firms developing novel diagnostics and cellular therapies.

The company's competitive moat is anchored by longstanding exclusive licensing agreements conferring unique proprietary nucleic acid methylation biomarkers validated under CLIA-certified labs in the U.S., plus internally developed scalable CMC processes for LSC-derived exosomes [S1]. Partnering with multinational pharma firms like Novartis adds credibility while enabling co-development synergies.

Regulatory complexities demand sophisticated capabilities that few competitors can match—especially bridging Taiwan’s TFDA regulatory environment with the FDA in the U.S.—underscoring strategic advantage in offering "dual-core" regulatory navigation via the YC Biotech alliance.

However, as relatively early-stage entities dominate these emerging technology domains, execution speed on clinical milestones such as IND approvals for ophthalmology indications will heavily influence competitive positioning [S1].

Growth Drivers

YD Bio’s near-term growth hinges on several interrelated vectors:

- Clinical advancement of LSC exosome therapies targeting Dry Eye Disease (DED) and Age-Related Macular Degeneration (AMD), expecting IND submissions in 2026 followed by Phase I trials starting in 2027 [S1].

- Expansion of regulated oncology diagnostics via the EG Telehealth Platform designed for physician-led ordering workflows to capture growing demand for early cancer detection modalities leveraging DNA methylation signatures.

- Regulatory pathway acceleration enabled by reusable DMFs submitted to FDA for limbic stem cell products reducing developmental friction for future applications.

- Strategic M&A activity exemplified by the Safe Save Medical Cell Sciences & Technology deal to integrate late-stage immunotherapy candidates aimed at high unmet needs like glioblastoma [S9].

- Regulatory consulting service revenue potential through YC Biotech collaboration acting as a gateway for Asian CRO clients targeting U.S.-based trials.

- Geographic diversification spanning Taiwanese markets—where consumer ophthalmology product sales are concentrated—and U.S.-based contact lens distribution channels [S1], [S16].

Collectively these drivers promise multiple inflection points tied to milestone achievements like IND acceptances, clinical trial initiations, telehealth platform scaling metrics including test order volumes, patient enrollment rates at Taiwan clinical sites like Shuang Ho Hospital, plus successful integration of acquisitions.

Risks / Watchpoints / Growth Constraints

Key risks tempering upside include:

- Financial sustainability concerns given recurring operating losses ($8.3 million net loss reported for 2025) necessitate periodic equity or debt raises which dilute ownership or add debt service burdens [F1], [S10].

- Execution risk surrounding timely completion of preclinical validation required before initiating costly human trials; subject to regulatory feedback cycles that can be protracted or unpredictable [S1].

- Integration challenges associated with acquiring SSMC’s complex autologous dendritic cell therapy assets potentially divert management focus.

- Market adoption uncertainties—in oncology diagnostics especially where reimbursement policies evolve slowly—and ophthalmic therapeutics which face entrenched incumbents.

- Foreign exchange exposure owing to revenues denominated largely in New Taiwan Dollar vs reporting currency USD while NTD is controlled currency impacting translation volatility [S16].

- Regulatory hurdles outside primary markets: extension beyond Taiwan-U.S. dual core platform requires additional certifications potentially delaying international rollout.

- Operational scalability constrained by ongoing investments needed in manufacturing infrastructure highlighted by $9–$10 million capital expenditures earmarked primarily for real estate and production capacity expansion [S10], potentially stretching balance sheet given current cash runway.

What to Watch Next

Operationally critical events anticipated through 2026 include:

- IND submission timelines adherence for LSC-derived exosome therapies targeting DED and AMD scheduled this year along with establishment of clinical-grade master cell banks [S1].

- Initiation of Phase I clinical trials projected in 2027 but early preparatory steps measurable through site activations or protocol filings provide leading visibility.

- Closing of Safe Save Medical Cell Sciences & Technology acquisition contingent upon satisfactory due diligence by mid-2026 representing key strategic milestone toward pipeline diversification [S9], [S12].

- Uptake metrics from EG Telehealth Platform deployments including volume growth of physician-authorized cancer diagnostic tests will signal commercial traction.

- Progression in building out the "Taiwan-U.S. dual-core" regulatory alliance evidenced by new client wins from Asian CROs engaged via YC Biotech partnership expanding fee-for-service revenues beyond core product streams.

- Quarterly updates disclosing R&D spend intensity changes reflecting prioritization among competing initiatives alongside updates on regulatory feedback timelines.

- Cash burn rate trajectory relative to current $6 million cash buffer determining timing for potential refinancings or capital raises given target operating expenses estimated between $2.4 million to $2.7 million annually plus capex commitments approximating $9 million–$10 million [$F1], [S10].

Financial Profile Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $6mm | |

| 2025-12-31 | ||

| Total debt | $6764 | |

| 2025-12-31 | ||

| Net debt | $-6mm | |

| 2025-12-31 | ||

| Current assets | $10mm | |

| 2025-12-31 | ||

| Current liabilities | $1643578 | |

| 2025-12-31 | ||

| Current ratio | 5.88x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Revenue | $596,817 | |

| 2025-12-31 | ||

| Operating Income | -$5,271,721 | |

| 2025-12-31 | ||

| Net Income | -$8,311,316 | |

| 2025-12-31 | ||

| Cash & Equivalents | $6,007,615 | |

| 2025-12-31 | ||

| Total Debt | $6,764 | |

| 2025-12-31 | ||

| Current Ratio | 5.88 | |

| 2025-12-31 |

YD Bio's financials highlight modest revenues reflecting early commercial penetration coupled with substantial investment spending driving operating losses. Its strong liquidity position relative to minimal debt supports near-term operational funding needs but underscores dependency on successful fundraisings going forward [F1], [S10]. Continuous scaling depends on converting clinical pipelines into revenue-generating products while managing cash burn prudently.

This analysis synthesizes recent SEC filings as of April 2026 with an emphasis on operational developments affirming YD Bio’s evolving biotechnology specialty within highly regulated diagnostics and therapeutic markets. Although promising advances characterize its technological positioning especially through dual-core regulation-oriented partnerships and multi-indication pipelines leveraging cellular platforms—the company remains fundamentally reliant on near-term execution success amid financial constraints inherent at this developmental stage.

This report does not constitute investment advice but aims to provide an informed perspective grounded strictly on publicly filed disclosures respecting Valye News' analytical standards.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments