Brinker International Advances Brand Strength Despite Inflation and Traffic Pressures

Q3 fiscal 2026 results reveal resilience in Chili’s and Maggiano’s brands amid wage inflation and supply challenges.

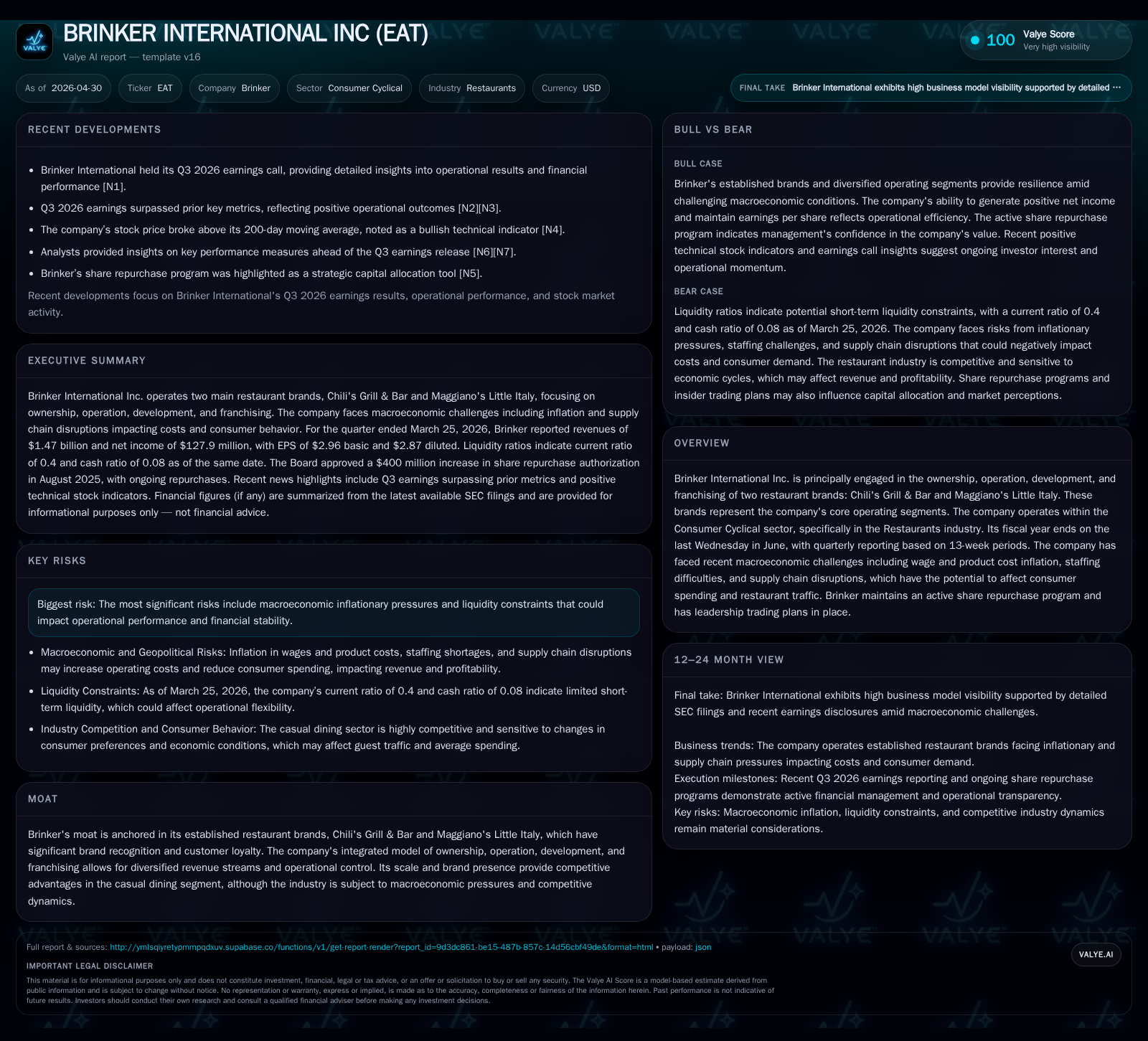

Brinker International’s latest quarterly filing for Q3 fiscal 2026 highlights stable operational performance supported by its flagship brands Chili’s Grill & Bar and Maggiano’s Little Italy. While macroeconomic headwinds such as product cost inflation, labor constraints, and supply chain disruptions persist, the company has maintained pricing power and customer loyalty. Brinker leverages a mixed model of direct operation and franchising to diversify revenue streams, focusing on digital sales and menu innovation to offset traffic pressures. The competitive casual dining space remains challenged but Brinker's scale, brand recognition, and disciplined capital strategy underpin its market position. Key growth avenues include digital expansion, franchise growth, and menu enhancements.

Recent Operating Update: Q3 Fiscal 2026 Highlights

Brinker International's Q3 fiscal 2026 report dated April 29, 2026 ([S2],[S3]) underscores operational resilience amid persistent macroeconomic challenges. Management cited continued wage inflation and product cost pressures that impacted margins but emphasized proactive price management across both Chili's Grill & Bar and Maggiano's Little Italy concepts. Supply chain disruptions remain a factor but have begun stabilizing.

Digital sales channels remain an accelerating component of revenue mix as Brinker deepens online ordering capabilities bolstering convenience amid fluctuating dine-in traffic patterns. The company's disciplined deployment of share repurchases continues with a roughly $400 million increase approved in August 2025; during Q3 they repurchased approximately 0.7 million shares at an average price near $157 per share ([S2],[F1]).

Business Model: Diversified Revenue via Integrated Owned & Franchised Concepts

Brinker owns, operates, develops, and franchises two core restaurant brands: Chili’s Grill & Bar (leading midscale casual dining) and Maggiano’s Little Italy (upscale casual dining with Italian-American cuisine) ([S1]). This hybrid model spreads risk between corporate-operated units generating direct revenue from food/beverage sales and franchised units producing royalty income based on sales volumes.

Revenue mechanics stem primarily from guest visits driving food and beverage sales—modulated by average guest check influenced via menu pricing adjustments, promotional activity, and product mix innovation. Digital ordering has added a new channel increasing transaction throughput while reducing friction for customers.

Margins are affected by labor pay scales which remain elevated due to ongoing scarcity of skilled restaurant workers nationwide. Food cost volatility also pressures input expenses despite tighter supply chain efforts. Brinker aims to offset these through targeted price actions without undermining customer retention or brand value.

Industry Structure & Competitive Positioning

The casual dining segment is crowded with legacy chains grappling with competition from fast casual formats emphasizing speed/value and technology-driven delivery platforms targeting convenience. Brinker leverages strong brand equity—particularly Chili’s widespread recognition—and scale advantages such as centralized supply agreements which yield some purchasing leverage.

Integrated ownership plus franchising diversifies exposure to unit economics fluctuations; owned stores afford control over operational standards while franchises provide fee revenue with lower capital intensity.

Marketing leadership upgrades (George Felix promoted to EVP Chief Marketing Officer in February 2026 [S15]) signal emphasis on sharpening brand strategies amid competitive noise.

Growth Drivers

- Digital Expansion: Increasing penetration of to-go/delivery orders via proprietary apps or third-party platforms drives incremental volume and improves customer experience.

- Menu Innovation: Iterative updates combined with value-based offers seek to sustain relevance especially among younger demographics more sensitive to trend cycles.

- Franchise Development: Expansion of franchised units builds recurring royalty streams and limits CapEx demands on company balance sheet.

- Operational Productivity: Ongoing efforts aim to optimize labor scheduling tech alongside simplification of kitchens reduce cost pressures.

- Share Repurchase Program: Aggressive authorized buyback capacity (~$207 million remaining as of March quarter end) supports shareholder returns while indicating confidence in intrinsic value [S2][F1].

Risks / Watchpoints / Growth Constraints

- Inflation Risk: Continued upward pressure on wages and food costs threaten margin sustainability; consumer sensitivity could limit frequency or average ticket expansion.

- Liquidity Constraints: Current ratio at approximately 0.4 ([F1]) signals need for careful working capital management; tight liquidity may hamper flexibility during downturns.

- Competitive Intensity: Fast casual operators emphasizing delivery/tech integration may erode traditional dine-in market share.

- Traffic Patterns: Potential shifts in consumer discretionary spending linked to macroeconomic trends impact same-store sales trajectory.

- Franchise Dependence Risks: Overreliance on franchise fees exposes revenue streams to underlying operator performance variability.

What to Watch Next

Investors should focus on several key metrics from upcoming quarters:

- Same-store sales growth or decline across both concepts indicating demand health.

- Pricing elasticity effects — whether further price hikes dilute traffic or support margin preservation.

- Franchise unit openings vs closures reflecting network vitality.

- Labor cost trends juxtaposed with productivity measures signaling margin turnaround potential.

- Ratio of digital-to-total sales showing progress in omnichannel penetration.

- Any additional share repurchase activity under the expanded program timing/volume details.

Financial Profile

Latest financial snapshot

At Q3 end March 25, 2026 ([F1]), Brinker reported cash & equivalents of approximately $57 million against current liabilities near $681 million resulting in a current ratio around 0.4 reflective of tight near-term liquidity. Total debt stood around $350 million last measured at June 25, 2025 with net debt approximating $293 million after cash offsets.

This analysis is based on publicly available SEC filings up to April 29, 2026 ([S1],[S2],[S3],[F1]) and industry context observations. It does not constitute investment advice or recommendations. Readers should conduct further due diligence before any decision-making related to Brinker International Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments