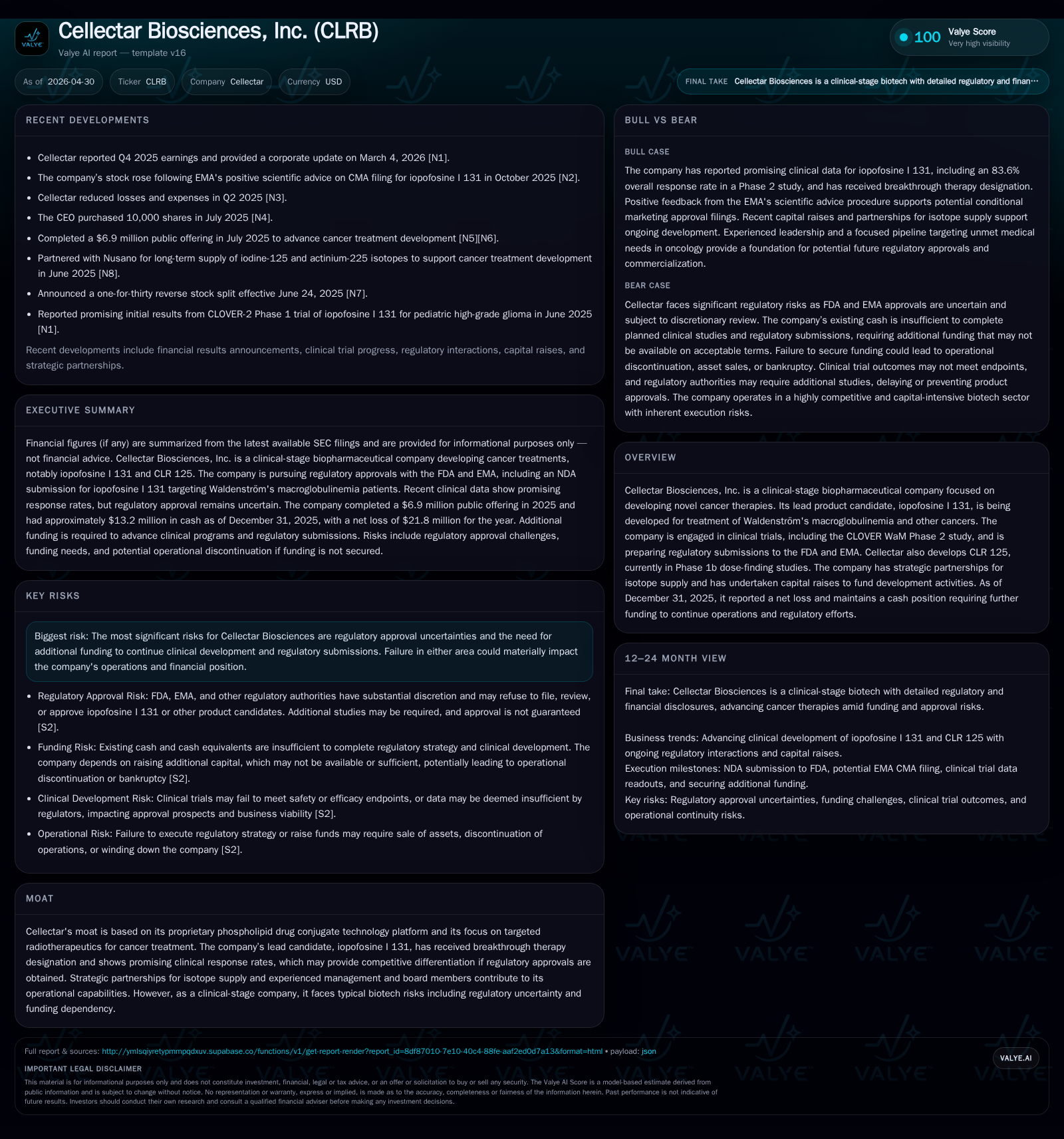

Cellectar Biosciences Advances Regulatory Push Amid Funding Challenges

Recent filings highlight Cellectar's approach toward NDA submission for its lead cancer therapy amid critical capital constraints.

Cellectar Biosciences is progressing toward regulatory submissions for its lead radiotherapeutic drug candidate, iopofosine I 131, focusing on treatment of Waldenström's macroglobulinemia after prior therapies. The company recently received favorable yet non-binding scientific advice from the EMA regarding conditional marketing authorization in Europe and plans an FDA NDA submission targeting accelerated approval. However, liquidity remains tight with cash sufficient only to early-mid 2026, forcing a reliance on additional financing to sustain clinical development and regulatory efforts. Success depends highly on navigating regulatory discretion and securing further capital.

Latest Quarterly Update Highlights Clinical and Regulatory Progress

The most recent operating disclosure in Cellectar Biosciences’ November 13, 2025 10-Q [S2] and subsequent March 4, 2026 8-K [S3] provide critical updates framing the company’s near-term strategic priorities. Chief among them is the company's plan to file a New Drug Application (NDA) with the U.S. Food and Drug Administration (FDA) seeking accelerated approval of its lead candidate iopofosine I 131 for Waldenström's macroglobulinemia (WM) patients who have failed at least two prior therapies including a Bruton tyrosine kinase inhibitor (BTKi). The CLOVER WaM Phase 2 clinical study underpins this application.

Concurrently, Cellectar has made significant regulatory strides in Europe via the Scientific Advice Working Party (SAWP) of the European Medicines Agency (EMA). SAWP has advised that submitting a conditional marketing authorization (CMA) application could be acceptable for the post-BTKi refractory WM patient population—a rare subset with significant unmet need [S18]. However, this endorsement is guidance-only; final EMA approval will depend on comprehensive review including safety, efficacy metrics, trial conduct scrutiny, and potential necessity for additional studies [S16]: such regulatory discretion introduces substantial uncertainty.

Meanwhile, Cellectar continues the Phase 1b dose-finding study for CLR 125—another candidate designed to broaden their oncology pipeline—though they acknowledge that their existing cash reserves are insufficient to complete this trial without raising additional funding [S2]. This fiscal tightrope underscores the dual challenge: advancing critical clinical milestones while managing constrained capital.

Cellectar’s Business Model Centered on Targeted Radiotherapeutics

At its core, Cellectar is a clinical-stage biopharmaceutical firm focused on developing novel targeted radiotherapeutics aimed at difficult-to-treat cancers. The company’s proprietary drug conjugate platform leverages phospholipids as delivery vehicles binding radioactive isotopes to enable precise tumor targeting with limited systemic toxicity [S1].

Their flagship asset, iopofosine I 131, couples radioactive iodine-131 (I-131) with phospholipid conjugates designed primarily for patients with Waldenström's macroglobulinemia refractory to BTKi therapies—a niche within hematologic malignancies characterized by poor outcomes post-standard treatments [S1]. The platform intends to enhance efficacy by delivering radiation selectively into cancer cells while sparing healthy tissues.

This modality differentiates Cellectar relative to conventional chemotherapies or small molecules through precision targeting leveraging radiopharmaceutical characteristics—a space increasingly competitive yet fragmented. Isotope supply partnerships support production but also represent complex logistical factors given the half-life constraints and specialized manufacturing needed [S1].

Consequently, revenue mechanics depend ultimately on successful product approvals followed by market adoption within rare cancer segments characterized by specialized centers familiar with radiotherapy protocols. Early-stage clinical positioning means margins or profitability remain structurally distant; value accrual pivots entirely on regulatory milestones and eventual commercialization agreements.

Competitive Context: Focused Pipeline in Niche Oncology Segment

Within an oncology ecosystem crowded by immunotherapies, kinase inhibitors, and antibody-drug conjugates, Cellectar occupies a narrow specialist realm focusing on radionuclide therapies targeting rare blood cancers such as WM. The smaller patient base constrains absolute market size but enhances pricing power when addressing refractory populations with substantial unmet need.

Breakthrough Therapy Designation granted by FDA signals potential expedited pathway benefits if the data sustains efficacy claims [S1]. Nevertheless, approvals here face steep hurdles due to stringent requirements around demonstrating safety/efficacy endpoints in relatively small populations.

Barriers extend beyond regulation into manufacturing scale-up challenges intrinsic to radiopharmaceuticals—these require specialized isotope sourcing that can create bottlenecks or favorable leverage depending on partnerships. Strategic alliances supplying isotopes help mitigate supply-chain risks but also tether operational dependence.

Additionally, market adoption curves remain speculative at this juncture; clinicians' willingness to integrate novel radionuclide therapies alongside existing standards will be influenced by reimbursement frameworks and real-world effectiveness post-launch.

Growth Drivers: Regulatory Approvals and Clinical Data Catalysts

Cellectar’s path to growth is tightly linked to concrete near-term milestones anchored in regulatory submissions and clinical trial progress:

- NDA Submission Timing: The FDA filing for iopofosine I 131 represents a pivotal event poised to unlock commercial pathways pending review outcomes [S2].

- Confirmatory Trial Design Agreement: The company's ability to align with FDA/EMA on post-approval confirmatory study design affects both labeling scope and accelerated approval viability.

- EMA Conditional Marketing Authorization: Positive opinion from EMA’s SAWP opens an early European access route potentially as soon as 2027 if approvals materialize [S18].

- CLR 125 Phase 1b Dose-Finding Readouts: Preliminary data from this study will inform pipeline breadth expansion beyond WM indications.

- Capital Raises Tied to Execution: Successful fundraising efforts directly enable regulatory strategy execution and ongoing trials.

These catalysts are quantifiable proxies for validation of both science and commercial feasibility. Absence or delay could stall momentum considerably.

Risks and Constraints: Funding Dependencies and Approval Uncertainties

Foremost risks center around financing adequacy given reported cash not sufficient to cover full planned development through critical upcoming events including NDA submission and Phase 1b completion [S2], [S16]. The company acknowledges explicit dependency on raising capital through equity or debt transactions which introduces dilution risk or shifts in control dynamics.

Regulatory authority discretion remains another acute constraint. Both FDA and EMA retain broad latitude to reject filings based on disagreements over statistical power, trial design nuances, safety assessments or data interpretation despite positive internal conclusions [S20]. The non-binding nature of EMA scientific advice underscores this unpredictability where even precedent-setting RAD/radiotherapeutic drugs have failed final approval.

Operationally, complex isotope sourcing chains pose potential bottlenecks threatening consistent clinical supply should scale-up demands escalate rapidly upon market entry.

Failure either on funding fronts or regulatory clearance substantially imperils continued operations possibly leading to asset sale or restructuring as per disclosed contingencies [S20],.

Key Upcoming Milestones to Monitor

Stakeholders should track several principal events that will serve as barometers for future prospects:

- Anticipated NDA filing date official announcement covering target patient indication post-BTKi refractory WM [S2], [S3].

- Regulatory agency feedback sessions outlining confirmatory trial expectations especially aligning FDA/EMA requirements.

- Initial readouts from CLR 125 Phase 1b dose-finding study providing insight into pipeline diversification potential.

- Progress updates on EMA CMA application status potentially accelerating European market access timelines.

- Announcements regarding additional financings validating ability to fund key milestones without disruptive dilution effects.

These checkpoints provide measurable signals for assessing success trajectory versus execution risks.

Current Financial Position and Liquidity Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $13mm | |

| 2025-12-31 | ||

| Current assets | $14mm | |

| 2025-12-31 | ||

| Current liabilities | $5mm | |

| 2025-12-31 | ||

| Current ratio | 2.96x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

As of December 31, 2025, Cellectar held roughly $13.2 million in cash and equivalents against current liabilities near $4.75 million yielding a current ratio close to 2.96 indicating reasonable near-term liquidity coverage absent unforeseen expenditures [F1].

However, net losses totaled over $21.7 million for the year ended December 31 reflecting high R&D spend typical of clinical-stage biotechs engaged in multiple phases of trials without product revenues yet generated [F1].

Total debt appears minimal based on available data indicating low leverage risk but emphasizing dependence on equity capital markets or partnership deals for sustaining operations beyond Q3-Q4 of fiscal 2026 given projected burn rates disclosed in filings [F1], [S2], [S3].

| Metric | Value |

|---|---|

| Cash & Equivalents | $13,196,033 |

| Current Liabilities | $4,749,737 |

| Current Ratio | 2.96 |

| Net Income (FY2025) | -$21,791,037 |

This financial snapshot frames a biotech firm balancing significant operational ambitions facing imminent funding imperatives.

This analysis is based solely on publicly available SEC filings as referenced above. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments